How money laundering works

Money laundering operations by criminal organisations can involve businesses the public administration and large banks working together to give a legal appearance to money obtained illegally. Juan Carlos Galindo, an expert in the prevention of money laundering and terrorist financing, explains the mechanisms money launderers use.

Almost three-quarters of criminal networks in the European Union use some form of money laundering to finance their operations and hide their assets. These transactions are estimated to have a total value of between 117 and 210 billion euros in the EU.

The main purpose of money laundering is to legalise the proceeds of criminal activity. It can be a relatively simple process carried out locally or nationally, or a very sophisticated process involving numerous intermediaries in several jurisdictions using the international financial system.

In an interview on the “ConPdePodcast” programme, Juan Carlos Galindo, an expert in the prevention of money laundering and terrorist financing, describes in detail how money is laundered. He begins by explaining the possible origins of this term: one that attributes the concept to Al Capone, who bought a chain of laundromats to use them as a legal front to recycle the money obtained from his criminal activities and another that mentions a Colombian method of counterfeiting American banknotes.

Galindo explains that there are three stages in money laundering – placement, transformation, and integration – and gives some practical examples:

1. Placement: This represents the first step in integrating the proceeds of crime into the legitimate financial system. This can be done through shell businesses, such as restaurants or cafés, which appear to have legitimate income.

2. Transformation: Layering or transformation involves converting the money into various financial or real estate assets to distance its illicit origin. This includes buying stocks, bonds, property and other assets through different companies.

3. Integration: The third and final stage of the laundering process aims to bring the money back into the market as apparently licit capital, allowing the criminal to make use of this money without arousing suspicion.

11Onze is the community fintech of Catalonia. Open an account by downloading the app El Canut for Android or iOS and join the revolution!

In contrast to inflation, deflation is an economic phenomenon characterised by a generalised and sustained fall in the prices of goods and services. While this may initially seem like good news for consumers because it increases their purchasing power, it can negatively affect the economy.

Inflation is an economic concept linked to the evolution of the Consumer Price Index (CPI) that almost everyone is familiar with, but what do we know about deflation? Contrary to inflation, deflation or negative inflation is a generalised and sustained decline – for at least two semesters – in the prices of goods and services.

Deflation is often associated with economic crises and recessions. It occurs when the supply of goods and services in an economy exceeds demand, forcing companies to cut prices to sell production and avoid accumulating large amounts of stocks.

In principle, lower prices may seem to be a good thing, since it will lead to a price adjustment that favours consumers. In other words, if wages are maintained, people’s purchasing power increases. But it can also generate a vicious circle of falling prices, leading to a reduction in spending and causing consumption and investment to stagnate, resulting in lower economic growth and higher unemployment.

Negative effects of deflation on the economy

Deflation can discourage consumption: if we believe that the price of a product will continue to fall, we will postpone our purchasing decision in the expectation of a better price. Therefore, if this sentiment is maintained over time and all consumers postpone their purchasing decisions, businesses will be forced to continue lowering the prices of their products due to the lack of sales. This effect is known as a deflationary spiral.

This will lead to lower profits for businesses, which will have to cut costs, so they will tend to also cut wages or lay off workers, causing unemployment to rise. Thus, deflation can create or worsen a recession, triggering long-lasting economic crises.

On the other hand, asset prices, such as stocks and real estate, may also fall during periods of deflation, negatively affecting the net worth of individuals and firms. This effect can make it more difficult to service debts by increasing the real burden of debt, which could lead to households and firms being unable to meet their obligations.

That is why central banks aim for price stability in their monetary policy and control of the money supply, aiming for inflation of around 2%. These measures are implemented to mitigate the possibility of deflation and thus avoid having to inject money into the economy to increase the money supply, reducing the value of money to raise prices.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

For years, the dominant economic narrative in Spain has associated growth with success: more population, more consumption, more tourism, more real estate activity and more GDP. But this model hides an uncomfortable reality: growth does not always mean prosperity. The big question is why some European regions generate more wealth with fewer people.

The Fènix Report puts data to this contradiction. Catalonia has increased its GDP over the last twenty-five years above the European average, but GDP per capita —the real wealth per inhabitant— has fallen in relative terms compared with Europe. In other words, the economy has become larger, but not necessarily richer for the people who live in it.

While other European economies have committed to productivity, innovation and added value, a large part of the Spanish economic model continues to be based on quantitative growth: more population, more consumption and more volume. The difference is profound, because it ends up determining wages, savings capacity, the quality of public services and, ultimately, the population’s standard of living.

The great mistake: confusing size with prosperity

An economy can grow in two ways. The first consists of increasing productivity: producing more value with more technology, more innovation and more efficiency. This is the model of the advanced industrial economies of northern Europe. The second consists of increasing volume: more population, more workers, more construction and more consumption.

This second model can make GDP grow quickly for a while, but it does not guarantee better wages or greater well-being. And this is where the great European divergence appears. According to the Report, Catalonia has gone from having GDP per capita six points above the European average to standing six points below it. This is a very significant deterioration for one of the main industrial economies of southern Europe.

The paradox is clear: economic activity increases, but many families have the objective feeling that they are living worse. The cost of living rises faster than wages, savings capacity decreases and access to housing has become one of the main concerns of the middle classes.

Bavaria: industry, innovation and high wages

If there is a region that symbolises the European model based on productivity, it is Bavaria. The German industrial engine concentrates technology companies, advanced industry, engineering, automation and applied research. It is no coincidence that it has some of the highest wages in Europe and one of the highest productivity rates on the continent.

The Fènix Report shows that Upper Bavaria is far ahead of Catalonia in productivity per hour worked. The key is not working more hours. The key is generating more value in each hour worked. Germany has built much of its economic model on export industry, technical training, business innovation and institutional stability. This ecosystem allows high wages to be paid without destroying competitiveness. It is exactly the opposite of a model based exclusively on low labour costs.

The Netherlands: a small country with giant productivity

The Netherlands shows that prosperity does not depend so much on the size of an economy as on the quality of its productive model. With a relatively small population and a small territory, it has managed to become one of the most efficient economies in the world. The port of Rotterdam, advanced logistics, technologised agribusiness and a commitment to technology have created a highly competitive model. According to the Fènix Report, the Netherlands stands well above Catalonia in productivity.

And this is not an abstract matter. It translates directly into higher wages, greater savings capacity, higher disposable income and a better financial situation for families. When an economy generates more value, wealth usually tends to be distributed better and offers greater social stability.

The Basque Country: the great anomaly of Spain

The case of the Basque Country is especially revealing because it shares an institutional framework with Catalonia and the rest of Spain. Even so, its economic performance has been very different.

According to the Report, the Basque Country has managed to improve its GDP per capita with demographic growth far lower than Catalonia’s. It has done so by maintaining a strong industrial fabric, a sustained commitment to industrial vocational training, medium-sized exporting companies and an economic structure less dependent on low-productivity sectors. It is not a perfect economy. But it shows that, even within Spain, it is possible to prioritise productivity, industry and added value over simple quantitative growth.

Catalonia: more activity, less relative income

Catalonia remains a powerful, diversified and entrepreneurial economy. But the data indicate a worrying trend: the growth model of recent years has been unable to translate economic expansion into greater individual prosperity.

The Fènix Report identifies two structural problems: productivity below the European average and a growing dependence on low-productivity sectors. This model creates employment, yes, but it is often employment with low wages, high temporary employment, little added value and limited savings capacity.

Meanwhile, housing, taxes and the cost of living continue to rise. The result is a growing feeling of impoverishment among the middle classes: working more no longer guarantees living better.

The future is not growing more, but growing better

Europe has already accepted that competing with low wages is a lost battle. The continent cannot compete with Asia on labour costs, but it can compete on technology, automation, advanced industry, research and human capital.

That is why many of Europe’s strongest economies are committing to reindustrialisation, attracting qualified talent and increasing productivity. Meanwhile, in much of southern Europe, a model based on volume still predominates: more tourism, more construction, more population and more consumption.

It is a model that can generate rapid growth for a while, but that also tends to cause pressure on infrastructure, higher housing costs, stagnant wages and lower social cohesion. The big question is what economic model Catalonia wants for the coming decades. Because the debate is no longer only how much an economy grows, but how it does so and who benefits from that growth. The most prosperous European economies are not necessarily those that accumulate the most population, but those that generate more value per worker.

And this is probably the great lesson of the Fènix Report: without productivity, there is no sustainable prosperity. At the 11Onze Community, we will continue to analyse these economic transformations to understand how they affect savings, wages and the future of families.

Protecting savings with physical gold has been one of 11Onze’s main contributions to its community and, now, the range of products is being expanded. That is why, in the face of volatility, still-high inflation and the growing crisis of confidence in the banking system, gold is once again strengthening as a safe-haven asset. Discover Gold Seed at Preciosos 11Onze.

If you would like to learn more about this topic, we recommend:

Economy

EconomyEurope wants to be independent… but from what?

6 min readEurope is talking more and more about “strategic autonomy”...

For years, we have been told an apparently indisputable idea: if the economy grows, society prospers. But what happens when GDP increases and, despite that, wages remain stagnant, housing becomes increasingly inaccessible and saving has become a luxury?

This is the great contradiction brought to the table by the Fènix Report: Catalonia generates more wealth than it did twenty-five years ago, but Catalans are relatively poorer than before. The figure is as forceful as it is uncomfortable.

At the beginning of the 2000s, Catalan GDP per capita was six points above the European average. Today, it is six points below. In just a quarter of a century, Catalonia has lost twelve points of relative prosperity compared with its European partners. This forces us to reconsider a fundamental question: what does economic growth really mean if this growth does not translate into better wages, greater savings capacity and a more affordable life for the majority?

Demographic growth does not guarantee prosperity

When governments announce that the economy is growing, they usually refer to Gross Domestic Product, GDP: the total value of goods and services produced by an economy. It is a useful but incomplete measure, because it does not explain how that wealth is distributed or how much prosperity actually corresponds to each citizen. That is why GDP per capita is much more revealing: it divides total wealth by the population and allows us to see whether growth reaches people’s pockets.

And this is where the great Catalan anomaly appears. According to the Fènix Report, Catalan GDP has grown above the European average over the last twenty-five years, but GDP per capita has moved in the opposite direction. The economy is larger, but individual prosperity is lower. The metaphor is simple: if a cake gets bigger, but there are more and more people sitting at the table, the slices may end up being smaller.

One of the key factors is Catalonia’s strong demographic growth, much higher than that of many comparable European regions. But more population does not automatically mean more prosperity. The report shows that territories such as the Basque Country or Aragon have improved their GDP per capita with much more moderate demographic increases. When growth is concentrated in low-productivity and low-wage sectors, population growth can put pressure on public services, make housing more expensive and reduce families’ disposable income.

The decisive variable is productivity: how much wealth an economy generates for each hour worked. Without productivity, there are no high wages, no savings, no solid public services and no sustainable prosperity. And here Catalonia also shows worrying symptoms: the Report points out that Catalan productivity has fallen from 92% to 87% of the European average in twenty-five years, placing it below industrial regions such as Bavaria, Stuttgart, Lombardy or the Netherlands. In other words: growth is not enough; we need to grow better.

The weight of low value-added sectors

The report also points to a structural problem that has accompanied the Catalan and Spanish economy for decades: a large share of the employment created comes from low-productivity sectors. Tourism, hospitality, restaurants and certain services have enormous weight in the current economic model. These are activities capable of generating a large economic volume and a great deal of apparent employment, but often with low wages, limited technological investment and little capacity for innovation. The problem is not the existence of these sectors, but the excessive dependence on a low value-added model while industrial, scientific and technological weight is being lost.

The consequences end up directly affecting paychecks and everyday life. Labour precariousness, the difficulty of retaining qualified talent and wage stagnation explain much of the feeling of impoverishment among the middle classes. And this perception is not only emotional: the data show how inflation, housing, food and energy have grown much faster than real wages. When the cost of living rises more than income, the capacity to save disappears. And when savings disappear, families’ financial security is also weakened.

Growth is no longer enough

For decades, the economic debate has focused almost exclusively on growth. But the Report forces us to ask a much deeper question: what kind of growth are we building? Not all economies grow in the same way. Some do so through innovation, advanced industry, technology and increased productivity. Others grow by expanding population and low-wage sectors. Both can increase GDP, but only one manages to generate sustainable prosperity. Catalonia remains a dynamic and entrepreneurial economy, but the indicators show clear signs that the current model is wearing out.

This is probably the great economic debate of the coming years: how to turn growth back into real prosperity. Because a country’s wealth is not measured only by what it produces, but also by its citizens’ ability to live better, save and build a stable future. At the 11Onze Community, we continue to analyse the major economic transformations that affect our daily lives, with a critical and educational perspective that helps us understand what is really happening behind the figures. Because growth does not always mean prosperity.

Protecting savings with physical gold has been one of 11Onze’s main contributions to its community and, now, the range of products is being expanded. That is why, in the face of volatility, still-high inflation and the growing crisis of confidence in the banking system, gold is once again strengthening as a safe-haven asset. Discover Gold Seed at Preciosos 11Onze.

The low yields still offered by bank deposits and the low interest paid in the latest auction of Treasury Bills are not enough to offset inflation, which in Catalonia remained at 3.6% in June. What other options are there to offset the price rises and protect our savings?

After experiencing a third consecutive rise in prices, inflation in Catalonia stagnated in June and remained at 3.6%, according to data published last Friday by the National Statistics Institute (INE). This is the same year-on-year variation recorded in May and two-tenths of a percentage point above the national average.

In this context, the enthusiasm for buying Treasury Bills experienced since December 2023 by retail investors seeking to offset inflation and make their savings more profitable than the low remuneration offered by large banks for deposits, is not being compensated as expected.

In the latest auction of Treasury bills, which took place at the beginning of the month, the Treasury paid an average interest rate of 3.4% for one-year bills and 3.3% for the six-month benchmark. Moreover, the consensus among experts is that the yield on Treasury Bills will fall even further in the coming months, as the official price of money falls.

On the other hand, Spanish banks still do not offer deposits with interest rates that compensate for rising prices. To find the few European banks with deposit accounts that match or exceed inflation, we have to look beyond Spain. This is the case of the Lithuanian bank, Mando Bank (3.66%), or Latvia’s BluOr Bank (3.65%).

11Onze offers its community a tool to combat inflation.

High returns with low-risk

As a general rule, investments that offer high returns come with high risk, while low-risk investments offer more stable, but potentially lower, returns. However, at 11Onze we have shown that this does not always have to be the case.

Saving with 11Onze is always based on one maxim: they have to be safe propositions. That is why we have made a firm commitment to gold, because of its historic role as a store of value. This precious metal not only represents a useful and effective way to diversify our savings and investments, but it can also help us to obtain liquidity in case of need.

At Preciosos 11Onze we offer gold bars in two formats: Gold Patrimony and Gold Seed. Bearing in mind that gold has doubled in value in the last five years and that its price rose by 15% in 2023, it has consolidated itself as an excellent option for dealing with inflation.

Litigation Funding offers liquidity to pursue socially just claims.

Earning money at the banks’ expense

Social justice does not have to be at odds with making a profit on your savings. Thanks to Litigation Funding, you can help others who have been abused by banks or the government while earning returns of between 9% and 11% on your money.

It is a product that has been structured exclusively for members of the 11Onze community, offering two ways to participate: an option that returns your capital and possible profits after one year, or another option in which your capital works for a few years and provides you with a monthly return in six months.

Almost 100% of Litigation Funding’s clients have reinvested their money in the same product. Considering that the capital is 100% insured and that it has had a 100% success rate in litigation since its launch just over a year ago, you have no excuse for having your savings standing still!

Preciosos 11Onze makes it easy to buy gold, at the best price and with total security. Give us a call and speak to one of our agents without compromise to clarify any doubts you may have and protect yourself from economic crises with the ultimate safe-haven asset: physical gold!

Newton’s first law states that an object always tends to be either at rest or in motion, rectilinear motion, unless an external force alters its state. Therefore, if a centripetal force acts on this object, it will be trapped by an invisible force called the central force. In this way, the object will see its movement altered, its inertia modified, and it will be difficult for it to return to its original physical state.

The Aragonese economist and historian José Larraz López, a distinguished member of the Royal Academy of Moral and Political Sciences, wrote an interesting book on economics in 1943 entitled ‘La época del mercantilismo en Castilla (1500-1700)’. He was a procurator in Franco’s Cortes and Franco’s minister in 1939, just after the end of the civil war – and therefore a man committed to Franco’s dictatorship to the bone – and when referring to the unity of Spain, he argued that the political reality of that time – between the 15th and 18th centuries – had been very different from that of his own time. Consequently, we could not speak of the existence of a single unitary state – Spain – for all those centuries, which would be the case after the arrival of the Bourbons.

The fact is that both Galicia, Asturias, Cantabria, León and Castile – the original core of the kingdom – and the three Basque provinces – Alava, Guipúzcoa and Vizcaya – plus Extremadura, Andalusia and Murcia will end up forming part of the same integrated body. In this way, the central part of the Iberian Peninsula – the area stretching from the Cantabrian coast to the Strait of Gibraltar – will end up sharing the same border, and the same Cortes will legislate the territories – the Castilian Cortes – which will use the same currency and all together will follow the same economic and fiscal policy. Pardon, except for the three Basque provinces which, from the 14th century onwards, would be exempt from all Castilian taxes. It is therefore clear that the other peninsular territories – Portugal and the Catalan-Aragonese Confederation – were never part of this Castilian matrix.

Indeed, in the mid-15th century, the Iberian Peninsula was divided into five political blocs of unequal importance: Portugal, the territories of the Crown of Castile, the Kingdom of Navarre, the Catalan-Aragonese Confederation and the Muslim Emirate of Granada. In fact, by the middle of the 15th century, each of these groups of territories would eventually acquire a very distinct personality and become original societies with their own customs, their own legal peculiarities, their own institutions and even their own language.

That a historian of the darkest period of the dictatorship – such as José Larraz López – should serve to combat the colossal misinformation or ignorance wanted by current Spanishism should shame a part of the political class, the media – including the ‘influencers’ hidden behind the networks – who time and again, from their supreme tribunes, have not tired and will never tire of proclaiming the existence of a unitary Spain for more than five hundred years.

The Castilian oligarchy -for too long and although speaking Catalan in private-repeats over and over again the same mistake when they speak of Spain as a political reality since the 15th century, referring to it as ‘the oldest nation in Europe’. If they understood once and for all that from the 15th century to the early 18th century, Castile pursued a policy of zero integration of the Mediterranean – and Portuguese – world, and that this was only possible through the use of force, combined with persistent repression and a constant plundering of economic resources in order to modulate their legitimate aspirations, it would surely help them to understand many issues that happen to us today as a state. More specifically, it would help them to understand that the Spanish project – as it has been set out since the arrival of the Bourbons – is totally unsustainable.

“In the mid-15th century, the Iberian Peninsula was divided into five political blocs of unequal importance: Portugal, the territories of the Crown of Castile, the Kingdom of Navarre, the Catalan-Aragonese Confederation and the Muslim Emirate of Granada.”

The beginning of the Hispanic divergences

After the Navas de Tolosa, Castile definitively entered the interior of the lower Meseta, which provoked a period of extreme euphoria in view of the possibilities offered by the new territory. But it soon realised that, despite its determination, it was encountering the same problem that León had encountered at the end of the 12th century. It was after the Concordia de Benavent – the agreement on the purchase of the kingdom of León by Castile – that Castile – except the Nazarí Kingdom – acquired practically the current perimeter.

The lower plateau, with its mountainous and rugged terrain -especially in the areas closest to the Central system-had land that was unsuitable for agriculture -except for the Guadalquivir valley-, with scarce and poor quality pastures, which, added to the strong climatic variability between summer and winter, were too adverse factors to be able to take control quickly. In addition, there were three even more determining factors: the low birth rate of the population in the north, the lack of mobility of inhabitants from the north to the south – despite the promotion of the ‘presuras’ or territorial divisions – and the consequences of applying an excessively repressive policy against the native population – by arguing nonsense – which culminated in the expulsion of the Andalusian Moriscos.

All these factors would have a very negative impact on the Castilian economy because any manufacturing and commercial activity, such as trade with the East or Africa across the Straits of Gibraltar, would be nipped in the bud. In any case, the Monarchy – in order to prolong its expansionary policy – continued to need to increase its regular income, which contributed to a situation of extreme inflation, resulting in a monetary alteration and generating a permanent deficit in its balance of trade.

As a solution, the Monarchy exerted strong fiscal pressure on some sectors of the population – such as the Jews, for example – but above all on the great transhumant herds of the upper plateau, just at the time when both Flanders and northern Italy were becoming the great buyers of Castilian wool. This plains traffic had catapulted Burgos to the forefront of European cities and turned the Cantabrian Sea into an important maritime axis towards Europe, which stimulated the birth of a textile industry. But all this faded away as soon as the interests of the nobility – the owners of the land, based on ancient rights of conquest – prevailed over any private initiative of the plainsmen, which made it impossible for the economy to flourish in the following centuries.

Faced with economic suffocation, the Monarchy – in order to boost the economy – resorted to the credit offered by the Jewish communities settled in the main Hispanic cities. So it was, sooner rather than later, that kings, nobles, military orders, ecclesiastical communities and ‘councils’ – and even individuals or ‘situados’, as they were known at the time – ended up abusing credit, which in the long run became a real internal problem. Faced with the heavy indebtedness of the Castilian public treasury, the Monarchy – as a result of the generalisation of non-payments – began to reform its financial system, although the real trigger was the promulgation of the Edict of Granada – also known as the Decree of the Alhambra – by which the Catholic Monarchs decreed the expulsion of all Jews from the Hispanic territories, which meant obtaining large assets for the Monarchy in the short term.

As for the rest of the peninsular territories – above all the Mediterranean and the Portuguese Atlantic world – they were able to find in the sea a lever for growth that allowed them to continue with their expansionist policies. For example, the Catalan commercial bourgeoisie was able to take advantage of the consequences of the war with France – the famous crusade of Philip Ardid – to boost its manufacturing industry. The creation of the Consulates of the Sea and the extension of old maritime routes – begun in the 10th century – were the mechanisms of penetration that the Catalan-Aragonese Confederation used to satisfy the demand for its products – rags, iron tools, coral, leather, spices and slaves – both in the mainland markets – Lisbon, Donostia, Bilbao and Seville – and in the foreign markets of Sardinia, Sicily, Bruges, Constantinople, Tunisia and Alexandria.

A territory made up of free people

From the beginning of feudal expansion – at the beginning of the 9th century – the territories of the northwest peninsular were configured under the juridical-administrative formula of ‘dominium’, based on Roman law, which meant that the holder of the land property was a ‘dominus’ or lord. Therefore, the king or the count – the highest figure in the social pyramid – from the beginning became the final owner – directly or indirectly – of all those lands that were expropriated.

It should be borne in mind that no lord would have the slightest interest in owning land, water, herds or mills if there were no peasants capable of organising stable work processes that would lead to the conversion of effort into income. Therefore, with the creation of Extremadura from the 9th century onwards, the Castilian-Leonese expansionist policy was implemented by means of the ‘villa and land’ communities, which would become the key element of political-legal organisation within the ‘new expropriated territories’. In this way, the landscape of the Meseta was articulated on the basis of the foundation of a series of major towns – walled and with representation in the Castilian Cortes – on which depended six or eight unwalled hamlets located around the main town.

For the lords, the real danger lay in the existence – within that vast territory – of free peasant communities that could escape the new jurisdiction. For this reason, they created mechanisms that involved a brutal indebtedness of those communities of ‘villa and land’ through the famous settlement charters or ‘asentamientos’ and the ‘presura’ contracts, so that they would lose all possible mobility, remain attached to the land and, in this way, ensure the return of the debts contracted.

And since the king’s life was so ‘sacrificial’ – it still is today when they indulge in the luxury of elephant hunting – they ended up ceding the land for services rendered to other lords, ecclesiastical bodies or monasteries. Therefore, it depended on who was the final rentier – that is, the owner – whether the land was known as ‘realengas’, if it belonged to the king; if it belonged to an abbot or a bishop; ‘de solariego’, if it belonged to a nobleman or a military order; or de ‘behetría’, if it was the villagers themselves who chose the lord. In the long run, all these types of property would contribute to the formation of the large estates of the region – known as the process of ‘seigniorialisation’ – which, from the 14th century onwards, would lead to the concentration of much power, both economic and territorial, in a very small part of the Castilian population.

“From the 9th century onwards, the Castilian-Leonese expansionist policy was implemented by means of the ‘villa and land’ communities, which would become the key element of political-legal organisation within the new expropriated territories.”

Towards a new conception of the state

At the end of the 15th century, the Castilian-Leonese world would end up ‘expropriating’ some 385,000 km² of land – between the upper and lower plateau – on which nearly four and a half million people would live, including the Nassari population. In the rest of the peninsula, the population would be distributed as follows: in the territories of the Catalan-Aragonese Confederation, about nine hundred thousand people would live on about 110,000 km²; about one hundred and twenty thousand people would live on 11,000 km² in Navarre; and in Portugal, one million people would live on 88,000 km².

Castile, although it was the largest territory in the Iberian Peninsula, continued to experience continuous economic and demographic problems, mainly driven by the process of consolidation of ‘seigniorialisation’, to the detriment of the exhausted expansive economy, which had been based on the indiscriminate expropriation of land and the reallocation of property through physical coercion.

Then, during the second half of the 15th century, the Castilian Monarchy began a process of economic transformation through monetary and fiscal reform, which led to a major social imbalance, to the point that it ended up having a direct impact on noble interests. As a result, major disturbances broke out throughout the kingdom and, unable to calm things down, the Monarchy applied a policy of manorial satisfaction by offering more land, more rights and more pensions for life at the expense of the public treasury and financed by a special tax on the population of the towns of the ‘Comuneros0. To top it all off, in the early 16th century, the main Communities of Castile were forced to assume a considerable tax to cover the purchase of the Imperial title – by the Habsburg family – which led to the famous Revolt of the ‘Comuneros’.

Even so, this policy had an insufficient impact in placating the ambitions of the nobility, which brought to light the existence of a much deeper division within the Castilian aristocracy. The existence of two politically antagonistic factions soon became apparent: on the one hand, there were the Pacheco, Villena and Girón families, who were in favour of taking a more active part in the kingdom’s major political decisions and therefore saw the need to weaken the Monarchy in order to control it. On the other hand, there were the Santillanas and Mendozas who understood that the time had come to abstain from power because the Monarchy was the one that had to guarantee the stability of the kingdom to ensure its ‘seigniorial’ privileges… ‘in saecula saeculorum’.

After the Castilian Civil War (1475-1479), the two largest territories of the Iberian Peninsula – the Kingdom of Castile and the Catalan-Aragonese Confederation – created a new political entity known as the Hispanic Monarchy, which was soon joined by Granada (1492), Portugal (1497) and Navarre (1512). That new dynastic state was shaped by the union of only two key elements: the army and foreign policy. For the rest of the elements that would make up the modern state, such as borders, currencies, laws and institutions, they remained completely separate.

Thus, the configuration and distribution of power – agreed by both sides at the Concordia de Segovia – was structured as follows: while Castile was structured according to the sacralised authority of the queen and always above the nobility and the church – thanks to an effective policy of numbing the Cortes – the Catalan-Aragonese Confederation was organised around the Constitution of Observance, which would always oblige the king to govern and make agreements in accordance with the laws of the Principality.

In the long run, Castile would offer less resistance to the Hispanic monarchs, something that would not happen within the Catalan-Aragonese Confederation, which, while respecting all its legal-political realities, would end up limiting the non-agreed initiatives between the different arms – count-king, nobility, clergy and honest citizens – that would represent part of the confederate society. The historian John Elliott in his famous book ‘Imperial Spain (1469-1716)’ very aptly defined it as follows: the Spanish sovereigns (Castilians) were absolute kings in Castile and constitutional monarchs in Aragon (Catalonia).

“The Spanish (Castilian) sovereigns were absolute kings in Castile and constitutional monarchs in Aragon (Catalonia).”

The unconscious empire

Only chance and the trade winds led the first navigators of the Catalan-Aragonese Confederation to the most populated area of the American continent. From the very beginning of the westward voyages, the first navigators were certain and aware that where they had arrived was not the East Indies, but a completely different territory. Realising this fact, the Castilian Monarchy deployed all its modern legal and administrative machinery to legitimately possess it. Without entrusting itself to anyone and by right of conquest, the Monarchy once again claimed ownership of those territories, ignoring the indigenous population.

The discovery of important deposits of precious metals – between Mexico and Peru – led to the founding or re-founding of important American cities, which acquired a new territorial role in order to ensure a regular flow of wealth to Castile. Thus, acting as nouveau riche, Castile would spend an indecent amount of economic resources to build its concept of civilisation, based on Catholicism. This obsession – sometimes uncontrolled – would lead them to embark on a myriad of conflicts of all kinds, such as theological disputes, family conflicts, commercial affairs or lavish megalomaniac constructions.

However, at the beginning of the 17th century, the American mines began to show signs of depletion, which became more pronounced as the century progressed. Faced with this slowdown, and in order to maintain the same rate of expenditure, the Monarchy resorted to loans from German banks – the Fuggers and the Welsers – and the Genoese banks of the Spinola, Centurione, Balbi, Strata and, above all, Gio Luca Pallavicino families. It would then be forced to raise taxes and exert fiscal pressure on the whole of Hispanic society. We remember the famous ‘Union of Arms’ of the Duke of Olivares. Faced with a generalised avalanche of non-payments, the State entered into a process of successive bankruptcies (1627, 1647, 1652 and 1662), which contributed to projecting a very unfavourable image of Spain in the eyes of the other European chancelleries.

Spain’s history is still stigmatised today by a ‘black legend’ conceived between the 16th and 17th centuries – both by the Lutherans of Wittenberg and the Dutch of Dillenburg – which sought to chip away at its hegemony in the world. Subsequently, in order to control the raw materials of the Castilian and Portuguese colonies, the English would amplify Protestant propaganda as a key element of discrediting the colonial elites, something that would help them to initiate and finance the independence processes of the Spanish colonies throughout the 19th century.

The Bourbon drift

Castile – and later Spain – has always found itself in a dangerous vicious circle, in which the State’s expenditure has been excessive, and it has needed to continually increase taxes to balance its income, which has led – over a prolonged period of time – to an excessive fiscal pressure on the population as a whole.

With the entry of the Bourbons – after a long campaign to discredit the Habsburgs – the economic problems worsened when, through the use of continuous loans, on-lending, negotiations and renegotiations, these only served to satisfy their personal ‘grandeur’, to the detriment of the modernisation of society by the Enlightenment spirit that prevailed throughout Europe.

The Bourbons were always aware that the only way to economically sustain the entire Hispanic kingdom was to annex all the peninsular territories and thus form a new geopolitical hexagon. However, this was not possible because from the end of the 17th century, Portugal was no longer part of the Hispanic Monarchy, although attempts were made to annex it on three occasions during the 19th and 20th centuries. Therefore, efforts could only focus on the territories of the Levant peninsular which, first with the War of Succession and then with the Nueva Planta Decrees, allowed the Bourbons to link productive sectors – master craftsmen and merchants – to the new centralist system. As a result, this loyalty to the Bourbons allowed those who supported the new regime to gain access to large public contracts, which led to their absolute dependence on the new centralist system, which ended up weaving a web of widespread corruption at all levels of public administration.

There is no shortage of examples, such as when at the beginning of the 19th century Queen Maria Cristina – widow of Ferdinand VII – handed over power to the Spanish liberals, who at the same time made a pact with the Catalan industrial bourgeoisie to forge a self-interested political and socio-biological alliance that would materialise with the institution of a protectionist system. In this way, the Catalan mercantile tradition was squandered and the spirit of 1705 was betrayed, because the Bourbon refusal to free trade the Principality with England and the Netherlands – its main trading partners – initiated the whole process that would converge on 11 September 1714.

Nor did the establishment of the ‘democratic regime of “78” improve matters for the interests of the Levant peninsular. In fact, we Catalans, Valencians and Balearic Islanders suffer the consequences on a daily basis when, year after year, we contribute a massive amount of our GDP to the State coffers for the sake of a ‘solidarity-based centrality’ and, let us remember, with the approval of politicians, industrialists and bankers. And the story continues to the present day, when after a politically and socially intense decade, the State has just proposed to Catalonia – soon it will also propose it to Valencia and the Islands – a singular financing, surely conditioned by a great solidarity.

History had already warned Philip II when he visited his father, Emperor Charles of Habsburg, for the last time in the monastery of Yuste, when he advised him that if he wanted to increase the empire, he should locate the capital in Lisbon, because this would mean linking it to the New World; if he wanted to preserve it, he should locate it in Barcelona, in other words, link it to the classical tradition; and if he wanted to lose it, he should locate the capital in Madrid. And indeed, Madrid was the most poorly communicated capital in Europe until the beginning of the 20th century, when, thanks to the development of airlines and the construction of reservoirs, it managed to revitalise that solitude in the middle of the Castilian plateau.

We return to Newton. And how can we move from a centripetal force to a centrifugal force? Well, this will only be possible if there is a tangential acceleration that allows the velocity modulus of the object to vary and, in this way, it will be able to return to its original physical state. So, will technological innovation bring about an acceleration of the economic movement that, by taking advantage of ‘Open Banking’ and ‘Embedded Finance’, will bring about the tangential force that will make it possible to return to our original stage? It is up to us to achieve this!

11Onze is the community fintech of Catalonia. Open an account by downloading the app El Canut for Android or iOS and join the revolution!

El monitoratge de la nostra conducció ja és ineludible, els cotxes connectats s’han convertit en telèfons intel·ligents amb rodes i són una oportunitat de negoci addicional per a totes les marques, des de poder oferir equipament opcional via subscripcions fins a la venda a tercers de les dades generades per milions de clients. Ens ha de preocupar aquesta nova pèrdua de privacitat?

Amb l’avanç de la tecnologia, els cotxes connectats a internet s’estan convertint en una realitat cada vegada més present en les nostres vides. Els fabricants de cotxes argumenten que aquests vehicles sense botons físics, amb pantalles gegants i farcits de càmeres i sensors que monitoritzen el nostre comportament ofereixen una experiència de conducció més “segura” i còmoda.

Aquesta capacitat per comunicar-se amb altres vehicles, dispositius i serveis a través d’internet també obre noves oportunitats de negoci per a les marques. Alguns fabricants de cotxes ja han posat a prova la paciència dels seus clients amb models de subscripció mensual per seients calefactables, mentre d’altres ofereixen més potencia a canvi d’una subscripció anual o es pantaixen cobrar una subscripció per les opcions més populars.

A més, gràcies a aquesta interconnexió els vehicles poden recopilar i transmetre dades en temps real sobre els hàbits de conducció, la ubicació i l’estat del vehicle, que ofereixen un potencial d’ingressos addicionals per a les marques disposades a vendre aquesta informació, la qual cosa pot suposar una amenaça per al dret a la privacitat dels usuaris.

De la teoria a la realitat

Un informe elaborat per la fundació Mozilla alertava que els cotxes connectats són “terribles en concepte de privacitat i seguretat” i destacava que 25 de les marques de cotxes més conegudes recopilen sense consentiment un gran nombre de dades dels seus usuaris, no sols relacionades estrictament amb la conducció, com el seu lloc de residència o les seves destinacions habituals, sinó també d’altres molt més sensibles, com a expressions facials, estat de salut i informació genètica o sobre la seva vida sexual, tot això mitjançant dispositius connectats, micròfons i càmeres.

Segons l’estudi, un 84% de les marques analitzades comparteixen o venen les dades dels propietaris i un 92% atorga als conductors poc o cap control sobre les seves dades personals. Tot i que totes les marques suspenen en el tractament de dades, Tesla obté el pitjor resultat, mentre que Renault, Dacia i BMW, respectivament, tenen menys mala puntuació.

Alguns van qualificar aquest informe d’alarmista, tanmateix, pocs mesos després, el New York Times informava que algunes marques ja estan compartint dades dels hàbits de conducció dels seus clients amb les asseguradores i que als “mals conductors” ja els havien apujat les pòlisses fins a un 21%, sense haver tingut cap accident.

Kenn Dahl, un informàtic de Seattle, als Estats Units, que condueix un Chevrolet Bolt elèctric, va aconseguir un informe de LexisNexis, una agència de dades amb seu a Nova York que treballa amb asseguradores, on s’havien registrat les 640 vegades que ell o la seva dona havien agafat el cotxe en els últims sis mesos, amb tot luxe de detalls, com l’hora d’inici i fi del trajecte, les distàncies recorregudes, i totes les vegades que va passar de 130 km/h, o quan va fer frenades brusques o fortes acceleracions.

Totes aquestes dades es van recopilar i, sobretot, es van vendre sense que el Sr. Dahl ho sabés. En aquest cas es van vendre a companyies d’assegurances, però de la mateixa manera es podien haver venut a altres empreses de qualsevol àmbit.

Estem protegits per la legislació europea?

La normativa europea sobre el tractament de les dades personals aplicada als cotxes connectats es basa en el Reglament General de Protecció de Dades (RGPD) i en la Directiva ePrivacy, que estableixen els principis i drets que han de respectar-se en el tractament de les dades personals.

Entre altres obligacions, les empreses responsables del tractament de dades han d’informar els interessats sobre l’ús de les seves dades, obtenir el seu consentiment quan sigui necessari, garantir la seguretat i confidencialitat de les dades, minimitzar la quantitat i el temps de conservació de les dades i permetre l’exercici dels drets d’accés, rectificació, supressió, limitació, oposició i portabilitat.

Bàsicament, la mateixa normativa que ja s’aplica quant al tractament de dades i privacitat dels dispositius mòbils com ara els telèfons intel·ligents. Dit això, no és cap secret que feta la norma, feta la trampa, per la qual cosa els experts sempre recomanen revisar minuciosament els termes i condicions i només facilitar les dades o acceptar funcionalitats que realment aportin un valor real, cosa a la qual estem acostumats quan fem servir el mòbil, però que fins fa poc era impensable haver de tenir en compte cada vegada que engeguem el “nostre” cotxe.

11Onze és la fintech comunitària de Catalunya. Obre un compte descarregant l’app El Canut per Android o iOS. Uneix-te a la revolució!

Si t'ha agradat aquest article, et recomanem:

Tecnologia

TecnologiaLa transformació de la indústria automobilística

2 min readEn un nou episodi de La Plaça a Territori 17 analitzem com...

The world is not abandoning the dollar overnight, but more and more countries are trying to reduce their dependence on a financial system dominated by the United States.

For decades, the U.S. dollar has been much more than a currency. It has been the center of gravity of global trade, central bank reserves, and the international financial system. But something is changing. Slowly. Quietly. And, probably, irreversibly.

While headlines continue to focus on wars, sanctions, and geopolitical tensions, a much deeper movement is taking place beneath the surface: the fragmentation of the global monetary system built after the Second World War. The growing use of the dollar as a tool of geopolitical pressure has led many powers to start looking for alternatives to protect their economies and reduce vulnerabilities.

This is not yet the end of the dollar. But it is the beginning of a new scenario in which countries such as China, Russia, and India are promoting trade agreements in local currencies, strengthening alternative payment systems, and accumulating gold reserves at a very high pace. At the same time, central banks are developing digital monetary infrastructures that could redefine how the global financial system works over the coming decades.

Bretton Woods: the origin of the dollar’s global dominance

To understand what is happening today, we need to go back to 1944. With Europe devastated by war and the United States having become the planet’s leading industrial and financial power, the Bretton Woods Agreements established a new international monetary order.

The system was apparently simple: the dollar was linked to gold, and the rest of the world’s currencies were linked to the dollar. In practice, this turned the United States into the world’s financial referee. However, the system began to crack when Washington printed more money than it could back with gold reserves. In 1971, Richard Nixon suspended the dollar’s convertibility into gold, definitively burying the gold standard. From that moment on, the dollar was no longer backed by a physical asset and came to rest on something else: trust and geopolitical power.

The petrodollar: the great key to the system

The great strategic move came shortly afterwards. During the 1970s, the United States consolidated agreements with Saudi Arabia and other oil-exporting countries so that global crude oil would be sold exclusively in dollars. Thus, the petrodollar system was born.

The consequence was enormous. Any country that needed oil —that is, practically everyone— first had to obtain dollars. This created artificial global demand for the U.S. currency and allowed the United States to finance gigantic deficits with an ease impossible for any other country. The dollar thus became a trade currency, an international reserve, a financial safe haven, and a tool of geopolitical power.

But this privilege also created tensions. For decades, the system worked because there was no real alternative. However, the growing use of sanctions, financial blockades, and trade restrictions has led many powers to start seeing the dollar as a strategic vulnerability. When a country can be expelled from the SWIFT system, see its reserves frozen, or lose access to international trade because of a political decision made in Washington, dependence on the dollar ceases to be merely economic and becomes geopolitical. That is where dedollarization begins.

Russia, China, and the BRICS accelerate the shift

The invasion of Ukraine and the sanctions against Russia acted as a historic accelerator. Many countries understood that, if dollar reserves could be frozen, perhaps they were not as safe as they seemed. Since then, Russia and China have increased bilateral trade in yuan and rubles, India has purchased oil outside the traditional dollar circuit, the BRICS have promoted alternative payment systems, and several countries are exploring their own digital currencies to reduce dependence on the Western system.

It is no coincidence that central banks are accumulating gold at a very high pace. Gold remains one of the few monetary assets with no counterparty risk. It does not depend on any government, it cannot easily be sanctioned, and it preserves value outside the traditional financial system. When central banks buy gold massively, they do not do so out of historical romanticism. They do so because they are looking for protection.

This movement is not only taking place in reserves, but also in payment infrastructures. In parallel, central banks have been working for years on their own digital currencies —CBDCs—. Officially, they are presented as a tool to modernize payments and increase the efficiency of the financial system. But they also represent a new monetary architecture with unprecedented potential for control: they make it possible to track financial movements, limit the use of capital, apply monetary policies directly, and increase the supervisory capacity of states. That is why the great question is not only which system will replace the current one, but what degree of financial freedom citizens will retain within this new model.

Dedollarization will not be a collapse, but a transition

The most apocalyptic narratives constantly announce the imminent fall of the dollar. But reality will probably be slower and more complex. The United States remains the planet’s leading financial power, the dollar still represents a central share of global reserves, and no currency currently has the real capacity to replace it completely.

But that does not mean the system is immutable. Major monetary changes usually happen gradually, until a crisis accelerates processes that had been developing for years. The world is not suddenly destroying the dollar: it is building alternatives in order not to depend exclusively on it. Perhaps the real change will not be seeing the dollar disappear, but seeing it cease to be indispensable.

The great unknown is what will come next: a multipolar system with several regional currencies, a greater role for gold, digital currencies controlled by central banks, or a hybrid system in which all these tools coexist. It is still too early to know, but one thing is clear: dedollarization is no longer a marginal theory.

It is a real process that is redefining the global economic balance. And, as always happens in major historical transitions, the cost will not be paid only by those who design the system, but above all by the citizens who live within it. That is why, for the 11Onze community, understanding these changes is not alarmism: it is financial culture, wealth protection, and personal sovereignty. Those who understand the system can prepare better. Those who do not understand it only suffer its consequences.

Protecting savings with physical gold has been one of 11Onze’s main contributions to its community and, now, the range of products is being expanded. That is why, in the face of volatility, still-high inflation and the growing crisis of confidence in the banking system, gold is once again strengthening as a safe-haven asset. Discover Gold Seed at Preciosos 11Onze.

The confinement in the wake of the pandemic and two and a half years of runaway inflation have changed our spending habits. Recent economic data shows that we have reduced spending on material goods, but, despite rising prices, we are spending more on leisure activities. This is known as ‘funflation’.

Agroflation, biflation, deflation, stagflation, hyperinflation… If you have managed to keep up with the endless repertoire of inflation-related terms that emerged in recent years, here is another one to add to your dictionary: ‘funflation’.

It is an economic concept that combines the apparent contradiction between fun and inflation to reflect a society that prefers to enjoy the present, going to bars, restaurants and hotels, despite rising prices. Although high inflation continues to erode household savings, people have reduced their spending on material goods but have not stopped spending on leisure activities, and tourism remains at record levels.

We find ourselves with new and not-so-new generations aware of the near impossibility of owning a home or having a salary that allows us to save money but convinced that life must be enjoyed.

More spending on restaurants, hotels, leisure, and culture

Data from the latest Household Budget Survey conducted by the National Statistics Institute (INE) show that the average expenditure per household was 32,617 euros in 2023, an increase of 3.8% over the previous year.

The sectors where the average expenditure per household increased the most were restaurants and hotels, leisure and culture. Specifically, 3,331 euros were spent per household on restaurants and accommodation services, 386 more than in 2022, representing 13.2% of expenditure. While in leisure and culture, the biggest increase was in package holidays, with an average total expenditure per household of €1,651, 138 more than in 2022.

According to Business Insider, the economic data shows that spending on restaurants and leisure has increased, while buying material goods has decreased. Pedro Rey, professor at ESADE’s Department of Economics, specialising in behavioural economics, explained to the business publication that the difference lies in the fact that experience is now prioritised more, to the detriment of other items, such as clothes, household appliances or cars, the price of which is high in lean times.

The trend is to enjoy the present and life’s pleasures as if the world is coming to an end. After the shock of the confinement and the subsequent crises that have followed the sanitary crisis, it is not surprising that many consumers prioritise their mental well-being and social interaction over financial security.

Protect yourself from economic crises with the ultimate safe-haven asset: gold. If you want your savings to keep or increase their value, Gold Patrimony.

For years, talking about de-dollarisation, the return of gold or the decline of the Western monetary order seemed like an extravagance. A subject reserved for heterodox economists, geopolitical analysts or investors obsessed with systemic crises. Meanwhile, the dominant narrative repeated that the dollar was impregnable, that central banks had everything under control and that gold was little more than a relic of the past.

But history has a persistent habit: it always returns. And now, even the major international financial institutions are beginning to verbalise what was already visible to any attentive observer of the foundations of the global monetary system. The recent report by the Deutsche Bank Research Institute is not just another financial analysis. It is the recognition that the world is entering a new monetary, geopolitical and economic stage.

At 11Onze, we have been explaining this transformation for some time. Because this is not just about gold. It is about trust. It is about power. It is about monetary sovereignty. And it is, above all, about understanding the world before the official narrative admits that it has already changed.

The End of the Unipolar World

After the fall of the Berlin Wall, the West lived through an exceptional period. The United States became the undisputed power on the planet and the dollar consolidated itself as the backbone of global trade, international reserves and financial markets. The system worked because the world trusted the US.

Central banks accumulated dollars and US Treasury bonds. Exporting countries recycled their surpluses by buying American debt. And international trade moved within an architecture dominated by Western institutions such as the IMF, the World Bank or SWIFT.

At 11Onze, we were already explaining years ago that this architecture was beginning to show cracks. More and more countries were seeking to reduce their dependence on the dollar in the face of economic sanctions, the weaponisation of the financial system and the uncontrolled expansion of US debt. Today, that process is impossible to ignore.

The dollar’s share of global reserves has been gradually declining, while central bank gold purchases have accelerated. The freezing of Russian reserves after the war in Ukraine acted as a psychological turning point: many countries understood that their dollar-denominated assets could become political instruments. When money ceases to be neutral, states look for alternatives. And gold inevitably returns to the centre of the system.

The Silent Return of Gold

For decades, the modern financial system tried to relegate gold to a secondary role. But central banks never stopped considering it a strategic asset. The difference is that now they no longer hide it. At 11Onze, we have been explaining for years that gold is much more than a precious metal: it is a monetary asset with no counterparty risk, physically limited and impossible to print by political decision.

In a world of chronic fiscal deficits, permanent monetary expansion and structural inflation, central banks are recovering an instinct that has accompanied humanity for millennia: accumulating real assets. Gold purchases by emerging economies are not the result of short-term speculation, but of a structural trend. The major institutional players are preparing for a more fragmented, less stable and far more multipolar world.

Source. FMI

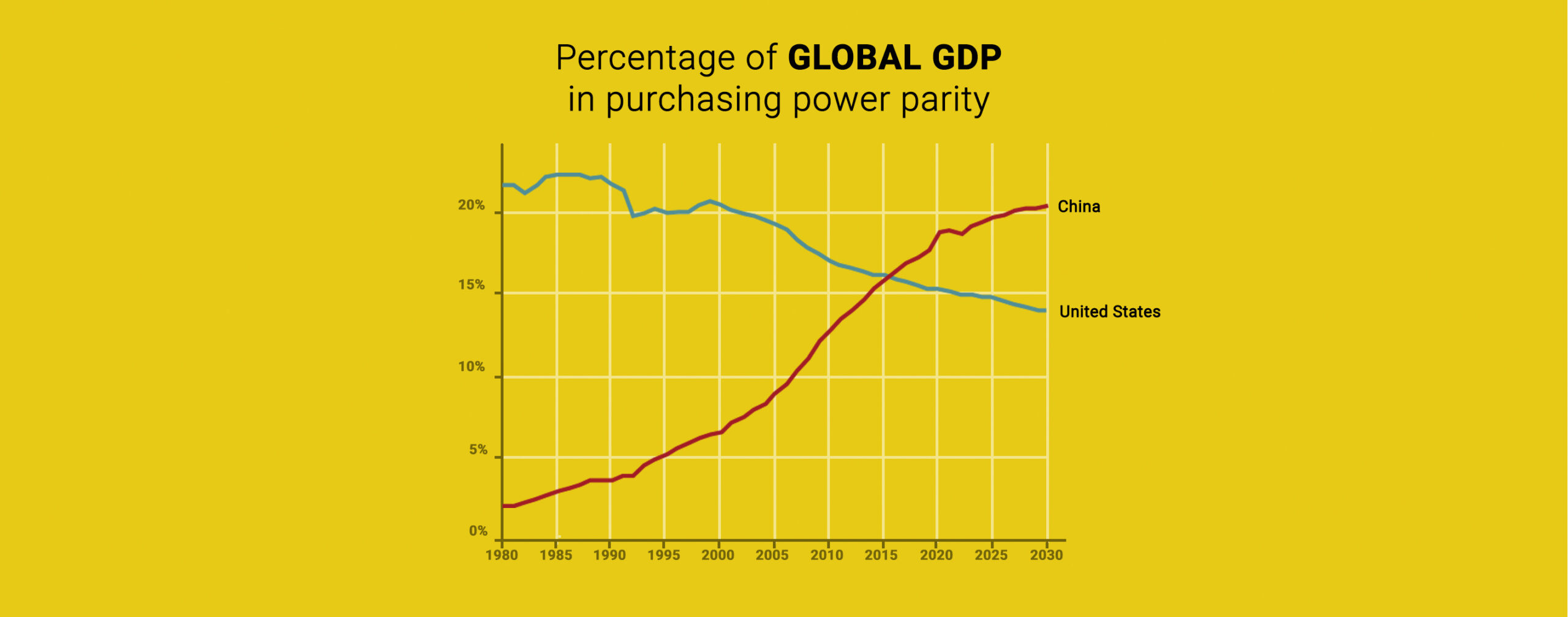

China Is No Longer the Future. It Is the Present.

This snapshot becomes one of the most significant economic images of recent years, because it shows us how China already represents close to 20% of global GDP in purchasing power parity, far surpassing the United States. This is not a simple statistical detail. It is the reflection of a historic shift in the world’s economic centre of gravity.

For two centuries, the West has dominated industry, finance, technology, maritime trade and the international monetary architecture. Now, for the first time in generations, a world is emerging in which that dominance is no longer absolute. And this has inevitable monetary consequences, because the international monetary system always ends up reflecting the real distribution of economic and productive power.

The current crisis is not only financial. It is, above all, a crisis of trust. Central banks have multiplied their balance sheets, governments have driven deficits upwards, inflation has reduced purchasing power and citizens are realising that working more does not always mean preserving more wealth. In this context, the major banks are not anticipating the future when they talk about the return of gold or de-dollarisation: they are simply adapting their discourse to a reality that is already too evident to continue ignoring.

And this is where a community like 11Onze adds value, because financial sovereignty does not consist only of buying an asset or protecting wealth, but of understanding the structural movements of the world before they become media consensus. The twenty-first century will not resemble the end of the twentieth century. The unipolar world is running out of steam, blind trust in fiat money is weakening and the new monetary architecture is already under way. The question is not whether the world will change. The question is who will be prepared to understand it before everyone else.

Protecting savings with physical gold has been one of 11Onze’s main contributions to its community and, now, the range of products is being expanded. That is why, in the face of volatility, still-high inflation and the growing crisis of confidence in the banking system, gold is once again strengthening as a safe-haven asset. Discover Gold Seed at Preciosos 11Onze.

If you would like to learn more about this topic, we recommend:

Economy

EconomyThe current state of the extractive system

5 min readAs with the resolution of past conflicts, the meeting of...