If you love them, gift them gold

If you also celebrate Valentine’s Day, you must be looking for a unique and special gift that symbolises your love for the person you cherish. At 11Onze we suggest you give ‘Amor amb Or’ as a gift. A gift that will last forever and that retains its value over time. For Valentine’s Day, gift gold coins!

We all know that Valentine’s Day in Catalonia is Sant Jordi, but if you want to give something more than just a rose or a book to the person you love… maybe you want to jump on the bandwagon of romantic gifts for Valentine’s Day. So, if you’ve already ruled out cologne, chocolates, romantic food and other typical gifts… at 11Onze we have a proposal for you that is as classic as it is surprising: give gold.

Gold coins for the person you love

Gold has always had an air of mystery and magic, a timeless gift with a special symbolic meaning that represents love and prosperity. Celebrate special moments with ‘Amor amb Or’. Surprise your loved one with a unique and precious gift that will remind him/her of your love forever.

‘Amor amb Or’ is the perfect gift for those special moments you want to celebrate with the people you love. Whether for a birthday or Valentine’s Day, giving gold coins as a gift will be an unforgettable detail that symbolises love and will maintain its value over time. If you want to give a unique and special gift, give ‘Amor amb Or’.

Preciosos 11Onze offers the option to buy gold coins from €220. For 11Onze members with an El Canut account, shipping is free. For all other buyers, it costs €9.99. If you want to buy gold coins as a gift, fill in this form and an agent will contact you. You will receive a personalized digital postcard with the name of the person to whom you give the gift. It will also need a physical address to send, shortly after, the gold coins.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Yesterday Monday’s correction in the price of gold has generated concern among some savers. But not every decline is a warning signal. Often, it is simply a pause within a much more solid underlying trend.

The first thing that must be clarified is that we are not facing a paradigm shift. The fall in the price of gold is framed as a specific technical correction, after weeks —and months— of strong revaluations. When an asset accumulates significant gains, it is common for part of the market to take profits. Therefore, it does not weaken the asset, but rather normalizes it.

Gold does not behave like a speculative stock or a highly volatile cryptocurrency. Its behaviour responds to slow, deep and, above all, global macroeconomic forces.

First factor: the dollar and interest rates

One of the main drivers behind the decline has been the rebound of the dollar and the movement of real interest rates.

When the dollar strengthens, gold —which is priced in this currency— becomes relatively more expensive for international buyers. This reduces short-term demand and puts downward pressure on the price.

In addition, any expectation of higher interest rates for longer works against gold in the short term. Not because gold loses intrinsic value, but because it does not offer financial yield. It competes with bonds and deposits, and when these promise higher immediate returns, part of the capital temporarily shifts.

Second factor: less fear… for now

Gold is, by definition, a thermometer of systemic fear. In recent days, markets have priced in a slightly more optimistic scenario: less negative macroeconomic data, lower immediate tension in financial markets and a sense —perhaps excessive— of control by central banks.

When fear subsides, gold takes a breath. But that does not mean that risks have disappeared; it means that the market, often myopic, looks only at the short term.

Third factor: short-term speculative movements

A significant part of the price of gold moves in futures and derivatives markets. Here, funds and operators intervene who do not buy gold to protect wealth, but to speculate on price. When these actors detect technical resistance levels or changes in sentiment, they execute rapid sell-offs that amplify movements. Therefore, we are dealing with noise rather than fundamentals.

In fact, according to data from the World Gold Council, structural demand for physical gold —especially from central banks and long-term wealth investors— remains solid.

What has not changed

Nothing that underpins gold as a safe-haven asset has changed, not even minimally. Global debt continues to grow at a faster pace than the real economy, with states and governments trapped in a permanent refinancing dynamic that is only viable through further monetary issuance.

Fiat currencies, detached from any real asset for decades, continue to lose purchasing power structurally —a slow but constant process that erodes savings quietly. Added to this is a fragmented geopolitical landscape, with open conflicts, increasingly closed economic blocs and growing distrust among major powers. It is no coincidence that, in this context, central banks —the very institutions that print money— are accumulating gold as they have not done for decades. When those who issue money seek refuge in a tangible asset, the message is clear.

For this reason, a temporary drop in the price of gold does not invalidate in any way the structural trend that supports it. On the contrary, it is part of its natural behaviour within market cycles. Historically, gold does not rise in a straight line, but advances with pauses, corrections, and necessary breathing phases after sustained upward moves. These corrections are not signs of weakness, but market-cleansing mechanisms, often caused by short-term speculative movements or temporary changes in sentiment.

Viewed with perspective, they have repeatedly been moments of opportunity for patient savers, not threats to the asset’s underlying value. Gold is not designed to reassure us every day, but to protect us when the system falters. And that remains fully valid today.

Gold is not an asset to watch every day, nor to judge by headlines. It is an asset designed to protect value over time, precisely because it does not depend on immediate market noise. Those who understand this are not unsettled by a temporary decline; they place it within a broader cycle. At 11Onze we speak of conscious saving, informed decisions and the ability to look beyond short-term fluctuations. Understanding gold not as a bet, but as a form of wealth insurance, is key to preserving the value of savings in an increasingly uncertain world.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

A PISA report confirms that our country is in tenth position out of the 15 OECD countries analysed, according to Price Water House (PwC), on financial knowledge of children between 13 and 15 years of age. In other words, Spain devotes far fewer hours to financial content at school than other countries, despite having the longest school day.

Financial education could be defined as a person’s ability to understand how the economy works and to make decisions based on that understanding. This type of information allows us to develop skills that will ultimately translate into greater economic well-being and, therefore, be better prepared for times of economic crisis such as those we are currently experiencing.

If we educate children from an early age in the concept of saving, in the good use of money, they will be better prepared for future crises that may occur. Responsible use and economic planning is essential for future generations. An example of this is the Inspiring Girls Foundation, which has launched the Inspiring Girls Financial Club with the aim of helping teenagers and young people learn to manage their own finances and learn about new trends and the financial market in a simple way. They are supported and have the experience of real women who work in prestigious companies.

Literature can also help us

BAPI, is a book written by Pilar Mellado, a CNMV technician, integrated in the Financial Education volunteers program, and its objective is to bring financial education to children. The author had the idea of creating this book to disseminate concepts through the main character, BAPI, an imaginary elephant that stars in a children’s book for children to learn basic financial concepts, such as “piggy bank”, “bank”, “spending”, “saving” or “debt” in a fun way.

Mellado states that “it is important that children are immersed in stories that transport them to a universe of superheroes, princes and princesses, fantastic animals or objects that come to life”. These stories, in addition to being entertaining for them, can be accompanied by what he called educational pills, and that is BAPI’s objective, to entertain by handing out financial pills.

The impact of social networks on consumption

It is true that nowadays, it is difficult to do this exercise, we live in a consumerist society, where everything is shown. Social networks do not help children to become aware of what it costs to earn money, let alone save.

In this social network, many influencers sponsored by big brands show an endless number of products and services. This is where the knowledge of the older generations is important, explaining that not everything we see and want can be bought.

If we want the little ones to be educated people, with values and success, we have to inculcate the sacrifice that comes with saving with the effort to get the things they want.

One of the first steps we can take is to give them a piggy bank from an early age. From that moment on, on their next birthday or special date, if they receive any economic gift, they will have to deposit it in their piggy bank. It is important to explain to them that with the money they have been saving for X amount of time, they could buy what they want, but if they spend it all, they will end up with zero money.

Later on, you can also propose activities to earn money. Create a calendar with weekly goals for household chores. Make them simple, but require the investment of a minimum of time and effort, and if they do everything that has been proposed, they can get money. With this method they will know what it costs to earn money through sacrifice.

Financial education comes from home, if we start with these practices and we get schools to talk more and more about personal finance and put it into practice, we will be creating new habits for the new generations that will make their lives easier and more bearable, and we will also get them to appreciate things more when they buy them with the fruit of their effort and tenacity.

If you want to wash your clothes without polluting the planet, 11Onze Recommends Natulim.

This 2025 has been a year that will go down in history for the true explosion of gold. Beyond occasional spikes, the yellow metal has reaffirmed its role as a safe haven, a diversification asset, and a sign of distrust toward conventional assets. Now, with the 2026 horizon ahead, it is worth asking: is this only a temporary surge or the prelude to a new cycle? And above all, what will it mean for savers and investors like you?

For almost a decade, gold lived in a kind of exile. Modest returns, institutional disinterest, and a dominant narrative proclaiming that technological assets —and even cryptocurrencies— were “the future.” In this context, the yellow metal seemed like a relic useful only at specific moments of turbulence.

But 2025 has completely turned this script upside down. The price of gold has not only climbed; it has done so by breaking psychological and structural levels it had not breached for years. Financial demand has regained unexpected vigour: in the United States alone, gold ETFs recorded a 58% year-on-year increase in the third quarter, according to World Gold Council data. It is a move that had not been seen in a long time and reveals a profound shift in investor sentiment.

This reappearance is not accidental. It responds to a cocktail of factors that, combined, create the kind of scenario that has historically fueled gold bull markets:

- Geopolitical uncertainty. Conflicts in Europe, rising tension in the Middle East, and a reconfiguration of global power among blocs. When political maps tremble, capital seeks refuge.

- Inflation that does not give way. Despite the slowdown from the 2023 peak, inflation remains above central bank targets. The loss of purchasing power becomes a real threat… and gold returns as the traditional shield against this phenomenon.

- Structural doubts about the dollar. U.S. fiscal policy, runaway debt, and de-dollarization moves led by emerging countries put pressure on the hegemonic currency. When the dollar hesitates, gold advances.

Taken together, these factors have made gold, far from being “out of place,” regain center stage in the financial arena, reaffirming its key function as an asset for preserving value.

The new driving force

If in the past retail investors were the ones who set gold’s bull cycles, 2025 has made a deeper change evident: demand has come from the system’s major players. And when central banks move, the market listens.

Over recent years, these institutions have been strengthening their gold reserves as part of a strategy of gradual de-dollarization and risk diversification. According to the World Gold Council, this trend will not only continue but will accelerate, and there is no indication that it should slow. Emerging countries —led by China, India, and Turkey— are at the center of the movement, but even some European central banks, have resumed purchases after decades of inactivity.

Added to this institutional demand is another engine: listed financial capital. In the United States, ETFs linked to physical gold have absorbed more than 37,000 million dollars in net inflows through September, a figure not seen since the last major bull cycle. The entry of these volumes shows a return of “smart money” toward tangible, resilient assets that are independent of monetary policy.

This context, combined with solid fundamentals, has led multiple international analysts to revise their forecasts upward. According to Mining, the price of gold could stand between 4,400 and 5,300 dollars per ounce in the coming year, a scenario that would place the metal in territory it has never reached.

But one of the most discussed predictions is Goldman Sachs’s, which anticipates an additional 6% increase through mid-2026. The determining factor, according to the institution, will not be jewelry demand or speculative funds, but the structural accumulation by central banks, a slow, steady, and extraordinarily powerful market force.

The key factors that explain this rise are mainly:

- Weakening of the dollar: the loss of confidence in the dollar’s role as the hegemonic currency pushes entire economies to strengthen tangible alternatives such as gold.

- Expectations of rate cuts in the U.S.: lower rates reduce bond yields and make gold —which does not generate cash flows but preserves value— more attractive.

- Geopolitical and trade tensions: global fragmentation creates an environment in which risk assets suffer and safe havens thrive.

- Accumulation of reserves outside the West: emerging countries seek to shield themselves against sanctions, devaluations, and financial instability.

Taken together, these elements do not describe a simple cyclical rebound. They point to a reconfiguration of the monetary order, where gold once again acts as a natural counterweight to fiat currencies and to an increasingly fragile financial system.

Where are markets looking in 2026?

If it is confirmed that gold can reach 4,400–5,300 dollars per ounce, we are facing a profound mutation of the market: gold would cease to be an “alternative asset” and become, de facto, an essential asset for preserving value. And this idea, which until recently seemed exaggerated, is today a serious hypothesis in many research offices.

The levers sustaining this possible new stage are clear. On the one hand, institutional and central-bank demand maintains a solid pace, driven by the need to diversify reserves and reduce monetary dependencies. In addition, the macro environment continues to play in the metal’s favor: if inflation persists or central banks choose to keep interest rates high, gold strengthens its role as a natural hedge against the loss of purchasing power.

Geopolitics adds even more pressure, because any shock between China and the U.S., a new episode in the Near East, or tensions in supply chains can immediately reactivate flows into safe-haven assets. And if, in parallel, bonds offer meager returns and stock markets enter phases of volatility, the metal shines again as a stable alternative amid the noise.

Even so, the path is not free of risks. An unexpected tightening of interest rates or a rebound in the dollar could slow the rise. There is also the phenomenon known as gold fatigue: when everyone takes for granted that it will keep rising, the market can lose momentum. And finally, it cannot be ruled out that other emerging assets, such as certain cryptocurrencies or industrial metals such as silver, capture part of investor attention.

Despite these nuances, the consensus is clear: if 2026 confirms the current trajectory, we will not be talking simply about a rebound, but about a change of era in gold’s role within the global financial system.

Impact for savers, investors, and the Fintech ecosystem

In an environment of persistent uncertainty, gold once again acts as a protective cushion for the saver: it does not replace a complete portfolio, but a moderate exposure can help soften monetary or stock-market shocks. At the same time, the Fintech revolution has democratized access to the metal: today it can be invested in through physical purchase, ETFs, digital platforms, fractional investment, or tokenization systems that were previously unthinkable.

For the end customer, the rule remains the same as always: balance and diversification. Neither concentrating everything in gold, nor ignoring an asset that has shown resilience when other markets weaken. And it should be kept in mind that, in many European countries, investment gold enjoys a specific tax treatment, an element that can influence the real return of any strategy.

If 2025 has been the year of the breakout, 2026 could be the year of consolidation. But nothing is automatic: gold’s trajectory will depend on inflation, the dollar, geopolitics, and central bank decisions. Gold is not a magic wand, but it is a key piece within a broader financial puzzle that the 11Onze community must observe with a critical and informed outlook.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

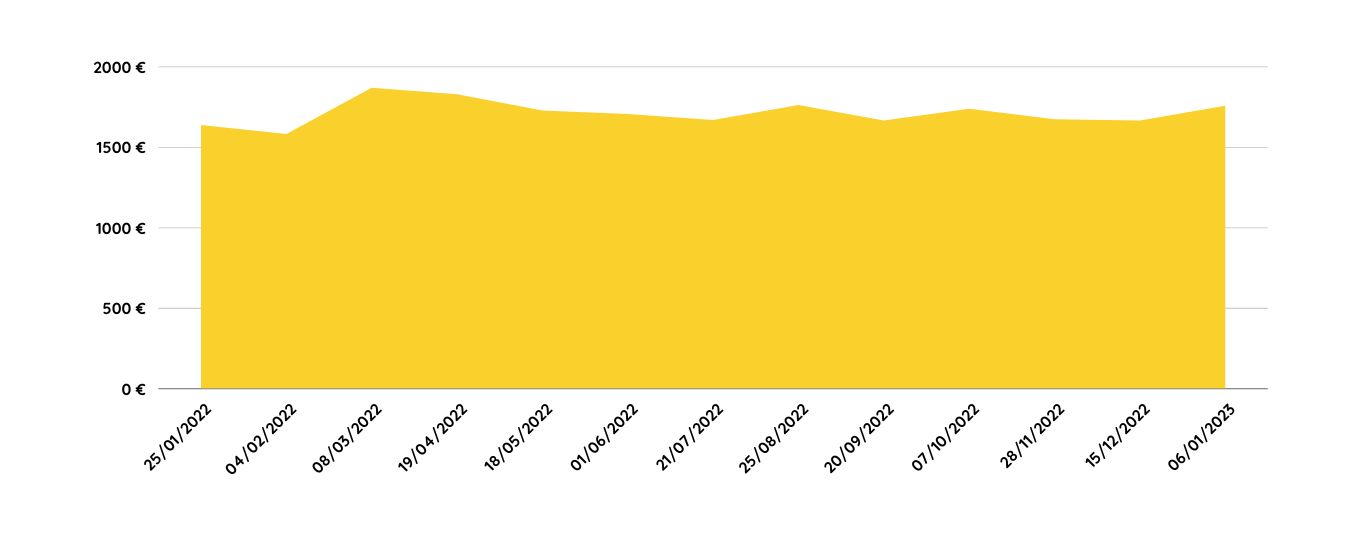

Year-on-year inflation in Spain in 2022 was 8.4%. Preciosos 11Onze gold has appreciated by 9.5%. In February 2022 we launched Preciosos 11Onze, offering members of our community to buy gold to protect themselves against inflation. Almost a year later, the gold price confirms the forecast.

It is no secret that an analysis of the historical evolution of the value of gold shows that, despite some occasional downward fluctuations, it is a real safe-haven asset that protects our savings, especially in times of economic crisis. This was obvious during the three-year period of the sanitary crisis, when gold prices increased by 40%.

After the return to ‘normality’, 2022 was seen as the year to consolidate the economic recovery. Even so, geopolitical uncertainty and the energy crisis, together with high inflation and currency tension due to the loss of value of the euro against the dollar, caused many families to lose much of their purchasing power.

A safe haven in the face of uncertainty

In this context, buying gold was not an investment or an instrument of speculation, but one of the few options people had to safeguard their money. That is why we launched Preciosos 11Onze, as a tool for our community to protect their savings in an extremely turbulent context.

The strength of the dollar and uncertainty about the possible rise in interest rates contributed to the fluctuation in the price of gold during 2021, but by early 2022 a new upward trend was confirmed. So, since then, has it maintained its reputation as a safe-haven asset? Without a shadow of a doubt, yes. When we launched Preciosos 11Onze, an ounce of gold was trading at €1.599, and today it is priced at €1.749, a rise in value of almost 9.5%.

This means that in the face of the depreciation of the euro due to inflation and competition from the dollar, having your money in gold would not only have prevented the loss of its value, but would have increased it considerably. Of course, it should be borne in mind that historical returns are not indicative of future returns and that any purchase of precious metals carries some risk, but as we have seen, leaving your money in the bank can be much worse.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Starting a new year is like starting a notebook. This 2022 has to be, by force, a year of plenty, because the previous two years have been pandemic and have been a real lesson for us, as well as helping us to prioritise our lives. As well as helping us to prioritise our lives, they have certainly helped us to learn how to save, and now it’s time to put all these lessons into practice!

To start the year off on the right foot, agent Silvia Granado gives us 11 tips for saving for 365 days. So that you have enough money left over to go on that weekend getaway you’ve been thinking about for a long time, or to shop during the sales, or to pay for that language course you know you need.

Let’s start with the basics: buy what you really need, organise a box with 12 envelopes for the 12 months of the year where you can hide some notes that will add up to a good amount at the end of the year, save the extra payments right away in the savings account, make a budget for holidays and divide the amount by 12 months to know how much you have to save each month, reduce lunches and dinners out and review subscriptions to content platforms. Want to know more tips? Check out the other half in the video below!

11 tips to start the year saving

We close a year in which the general rise in prices has made it difficult for many families to make ends meet. How will the economy evolve in 2023? What can we do to adjust the family budget? We talk about it with Xavi Viñolas, Editor of 11Onze and Gemma Vallet, Director of 11Onze District, in a new episode of La Plaça, Territori 17’s radio show.

With a year-on-year inflation rate of 8.4%, 2022 has been disastrous for many families who have seen their purchasing power fall to unsustainable levels. Runaway price rises have pushed up the cost of living at a time when many households were just recovering from the shock of the pandemic. What lies ahead for 2023?

This year, we will see whether central banks can halt the rise in prices without neutering the recovery of economies. Financial analysts predict that inflation will fall to 5%, but as Viñolas points out, “in a context of uncertainty and high economic volatility, we have to take any economic forecast with a grain of salt, the same experts told us that current inflation would only last a few months”.

La Plaça – Territori 17: Cost of living

Proactivity in reducing expenses

Now, more than ever, it is necessary to have a piggy bank for possible unforeseen events. But, faced with an economic context that does not favour saving and where our money has lost a good part of its value, it is not easy to reduce our monthly expenses in order to save.

The editor of 11Onze suggests we be proactive and look at reducing some fixed expenses, which are not always difficult to cut. Services contracted on a permanent basis, such as home or car insurance, can be renegotiated, or we can simply switch to a provider that offers a policy without permanence and more suited to our needs, which can be much cheaper.

Likewise, suppliers of utilities, such as electricity, can give us some room for manoeuvre, changing the contracted power or switching from the free market to the regulated market. Modifying the contract or looking for more reasonable offers can mean considerable savings and help us to balance the budget at the end of the month.

If you want to discover fair insurance for your home and for society, check 11Onze Segurs.

The limitation of the price of gas has lowered the price of electricity and gas compared to 2022. However, energy consumption is one of the most expensive fixed costs for Catalan households, so we propose ideas to reduce consumption.

We leave behind the holidays and winter begins to peek timidly to the head. This combination forces us to consider how to save on heating, because the pockets are shorter than ever at the beginning of the year. For this reason, from 11Onze the head of agents Mireia Cano raises 5 tricks to heat the house saving to the maximum.

This winter, save!

- Avoid sudden changes. When heating the house or a room, either with a stove or heating, do it gradually. Set a low temperature and raise it as the room warms up. If you set the temperature too high all of a sudden, the energy demand will be much higher.

- Take advantage of the hours of sunshine. We do it little in winter, but it is important. During the hours of sunshine, remove the curtains. If it is not cold at midday, take the opportunity to open the windows. The sun’s rays will warm the floor and the interior walls of the house. It’s not much, but every little helps!

- Insulate well. It is necessary to have good insulation, if not you can lose 30% of the heat of the house. Windows and doors are key. In the video, Mireia Cano suggests some homemade ideas that can help you. Something very simple and important is to lower the blinds every night so that the coldness does not radiate through the windows.

- Heat efficiently. It is not necessary to heat the whole house if you do not use all the rooms. Do you need the dining room? The bedroom? The bathroom? Then heat these spaces. It is obvious that air circulation will tend to balance the temperature, so what you should do is close the doors of the rooms you do not need.

- Invest in fabrics. If you don’t want it to get cold, keep the house warm. What does this mean? That the fabrics retain heat very well, therefore, carpets and curtains will help us to have a warmer home.

And finally, Mireia Cano adds an extra tip: heat the bed the way our grandparents did, with hot water bottles. Or, if you want, with bags of seeds that are heated in the microwave. Saving is key, for the pocket and for the planet. Applying these tricks won’t make you rich, but it sure will save a little. And as the saying goes, every stone makes a wall.

11Onze is the community fintech of Catalonia. Open an account by downloading the app El Canut for Android or iOS and join the revolution!

En la situació econòmica actual, estalviar és un objectiu que a tots ens agradaria assolir, però que sembla pràcticament impossible. Et presentem un mètode d’estalvi que es basa en percentatges i que et permet estalviar una quantitat mensual de diners més fàcilment del que et penses.

“És un mètode que s’utilitza habitualment per tots els que, no només volen estalviar, sinó que volen portar un control mensual de les seves despeses”, afirma Coral Santacruz, especialista de màrqueting d’11Onze.

Aquest mètode consisteix a separar el sou en tres percentatges diferents, “el 50% s’ha de destinar a les despeses fixes, el 30% a les despeses evitables, i el 20% es destina a l’estalvi”, detalla Santacruz. Seguint aquesta regla és fonamental que no destinem mai més de la meitat dels ingressos mensuals a cobrir les nostres necessitats bàsiques.

Com explica l’especialista de màrqueting, “per assegurar-nos de poder utilitzar aquest mètode sempre que puguem”, hem d’intentar posar-lo en pràctica “just quan rebem la nòmina, per no córrer el risc de gastar més durant el mes”.

Mètode d’estalvi 50 30 20

Si vols descobrir la millor opció per protegir els teus estalvis, entra a Preciosos 11Onze. T’ajudarem a comprar al millor preu el valor refugi per excel·lència: l’or físic.

Si et preocupa la qualitat de l’aigua que beu la teva família, probablement carreteges grans quantitats de garrafes o d’ampolles d’aigua mineral que al cap de l’any et costen més de 1.000 euros. Amb un filtre a la teva aixeta pots continuar gaudint d’aigua de qualitat, reduir per 15 la teva despesa, ajudar el planeta i estalviar-te maldecaps i d’esquena.

Estalviar no significa necessàriament privar-se de moltes coses. Sovint significa evitar sobrecostos innecessaris en productes essencials. Per això neix Imprescindibles 11Onze, perquè puguis reduir despeses en productes dels quals no pots prescindir.

El primer d’aquests productes disponibles a la web d’11Onze està relacionat amb l’aigua, el líquid essencial per a la vida. Hem de beure’n dos litres diaris i el més habitual és que acabem comprant un munt d’ampolles o garrafes de plàstic, amb el consegüent impacte mediambiental del plàstic que comporten.

Una família de quatre membres hauria de beure una mitjana de 2.920 litres d’aigua a l’any. Això equival a una despesa mínima de 1.196 euros si comprovem els preus de les ampolles d’1,5 litres més populars als principals supermercats d’Espanya i fem la mitjana.

En termes mediambientals, aquest consum suposa més de 60 kg de plàstic abocats al planeta i una quantitat de CO₂ similar emès a l’atmosfera durant la seva fabricació i transport.

Més de mil euros d’estalvi

És possible beure aigua de bona qualitat, amb bon sabor, estalviar i ajudar a preservar el planeta? La resposta és sí. Tan senzill com substituir el consum d’aigua envasada per aigua filtrada. El filtre Tappwater, que està fet en un 70 % de closca de coco, captura fins a 100 substàncies que podem trobar a l’aigua corrent, metalls pesants inclosos.

Pel que fa a l’estalvi econòmic, la senzilla instal·lació d’aquest filtre, que no requereix cap eina, equival a un estalvi de més de 1.100 euros a l’any per a una família de quatre membres. De gairebé 1.200 euros que suposa la compra d’aigua envasada es passa a menys de 90 euros en total.

El kit amb el filtre i els recanvis necessaris per al consum anual costen 79,99 euros. I a això només s’han de sumar menys de 10 euros de consum d’aigua de l’aixeta, tenint en compte que el preu mitjà a Espanya és d’aproximadament 0,0019 euros per litre i que amb el paquet anual de Tappwater es poden filtrar fins a 4.800 litres.

El planeta també s’estalvia plàstic i CO₂

Addicionalment, el medi ambient s’estalvia unes 1.947 ampolles de plàstic que no hauràs de carregar fins a casa i 63 kg de CO₂. I també t’assegures que l’aigua està lliure dels microplàstics que poden desprendre els envasos de plàstic quan es degraden per l’escalfor, i que ja s’ha demostrat que arriben al nostre torrent sanguini.

Tots els productes de Tappwater passen estrictes proves de qualitat abans de ser enviats als clients, i per això ofereixen una garantia d’un any.

Si vols descobrir com beure la millor aigua, estalviar diners i ajudar al planeta, entra a Imprescindibles 11Onze.