Gold is the world's most valuable asset

The asset with the top market capitalisation is not a company, but a precious metal. Gold is the world’s most valuable asset, ahead of the stock of any corporation. Throughout history, it has maintained or increased its value through all market fluctuations, establishing it as the ultimate safe-haven asset.

The global accumulated public debt as a percentage of gross domestic product has created an imbalance in terms of the capacity to generate wealth. States are paying more than they can afford and are increasing the fiscal pressure on a population hit by high interest rates in an attempt to contain inflation.

In this context of economic uncertainty, the intrinsic value of gold, which carries no credit risk and cannot be inflated, has made it the ultimate safe-haven asset for investors and particularly attractive for diversification and assured returns on savings.

While many investors are looking ahead to the expected rate cuts by the Federal Reserve (Fed) and the European Central Bank (ECB) later this month, the volume of trading in the golden metal has exceeded 150 billion euros per day in the last twelve months, making it the most traded financial asset after currencies.

On the other hand, company stocks can fluctuate dramatically due to several variables. We have seen this happen over the last few years with the big technology companies, where their market capitalisation has faced considerable headwinds from fears of overvaluation and the spectre of rising interest rates, although they have staged a remarkable recovery since the beginning of the year.

This has not been the case for the price of gold, which continues the upward trend it has experienced throughout its history. This year alone, it has already gone up by 17%, after rising by 15% in 2023 due to the US banking crisis, geopolitical tensions, military conflicts and the Fed’s monetary policy.

Top assets by market cap.

Source. companiesmarketcap

The most brilliant asset

Market capitalisation is the total value of a company’s shares on the stock market and is calculated by multiplying the total number of outstanding shares of a company by the current unit price of each share. In the case of precious metals, market capitalisation is obtained by multiplying their current price by the price of the existing stock of the metal that has already been mined.

Stocks with larger market capitalisations tend to be a safer bet, yet smaller companies may have greater potential for rapid growth and higher returns. In general, stocks with a large market capitalisation help investors diversify their portfolios to manage risk.

Gold, as an asset, has a current market value of $15.899 trillion. Far above Microsoft ($3 trillion), Apple ($2.9 trillion) and NVIDIA ($2.8 trillion). It exceeds the total value of the next five companies in the ranking and by almost ten times the value of silver, making it the world’s most valuable asset and a haven if we want to protect our savings.

If you want to discover the best option to protect your savings, go to Preciosos 11Onze. We will help you buy at the best price the ultimate safe haven asset: physical gold.

BBVA’s takeover bid for Banco Sabadell has the potential to transform the eurozone banking sector and revives the debate on the need for European banking consolidation that Brussels has been advocating for years. Even so, this concentration of financial services may have negative effects on banking competition and social inclusion.

A week ago, the CEO of Banco Sabadell, César González Bueno, was convinced that the hostile takeover bid would not go ahead because of the evolution of the stock premium. ‘I don’t think it will happen, it’s too complicated’. In any case, a month after it was leaked that BBVA was preparing a merger offer with Sabadell, the debate over banking consolidation is back on the table.

While the Spanish government is reticent about the operation, arguing that it will increase banking concentration and therefore hurt employment, the provision of financial services and financial stability, the European Union welcomes any bank consolidation that helps to eliminate alleged overcapacity and improve cost efficiency.

Bank consolidation refers to the process by which financial institutions merge or are acquired by other institutions, resulting in fewer banks with a larger market share. In Europe, this phenomenon has accelerated in recent years, driven by several economic and regulatory factors and with the support of the European Central Bank.

The creation of the banking union

After the financial crisis of 2008 and subsequent sovereign debt crises, the need to improve supervision and regulation of the EU financial sector became evident, especially regarding the eurozone.

In this context, the European banking union was established in 2014 to ensure the financial stability, safety, and soundness of the banking sector in the euro area and the EU as a whole. This is achieved through a single rulebook consisting of a set of legislative texts that must be complied with by all banks operating in the member states.

There are currently more than 4,500 active banks in the EU, a large part of which are small and medium-sized institutions. The ECB argues that such mergers, especially cross-border, could be conducive to risk diversification and financial market integration. It also points out that the new rules and this bank consolidation close loopholes and thus contribute to a more efficient functioning of the single market.

“The main mergers in the Spanish banking sector after the financial crisis”

Source. Álvaro Merino (2023) EOM

The darker side of consolidation

The current banking concentration in Spain is plain to see when we remember the number and diversity of building societies present three decades ago, when they had half the market share of the banking business.

The bailout of the Spanish banking sector with public money reduced their business and capacity. This consolidation resulted in a massive closure of branches and cash points. The risk of financial exclusion was real and, despite the government’s directives, the measures taken by the banks to alleviate it need to be revised.

The lack of competition in the banking market has also meant that Spanish banks’ interest rates on deposits are much lower than those offered on average in the EU. All this has happened in a context in which the big banks -CaixaBank, Banco Santander, BBVA, Banco Sabadell, Bankinter and Unicaja- have increased their profits exponentially.

Beyond bankruptcy protection, the success of bank consolidation will depend on the ability of regulators to balance profits with the need to maintain a competitive, diverse and inclusive banking sector. This will be no easy task, given that the promiscuous relationship between the political class and the banking sector has for decades been part of a system where looking after the public interest is not a priority.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Central banks worldwide have been buying record amounts of gold since the beginning of 2022. The pace and regularity with which these state-owned financial institutions are stocking up on gold is unprecedented. What is behind this new gold rush?

It is no secret that gold is a strategic safe-haven asset that plays a key role in diversifying investment portfolios. Throughout history, it has established itself as the ultimate store of value precisely because it maintains or increases its price during periods of economic uncertainty.

That said, in recent years, especially since 2022, the price and demand for gold have reached record highs and show no sign of abating. This upward trend has been driven by the accumulation of gold by central banks, which have been buying record amounts of the golden metal and continue to hoard it at a frenetic pace.

According to data from the World Gold Council (WGC), in Q1, central banks added 290 tonnes to their reserves, up 1% year-on-year and 69% more than the quarterly average of the past five years. This is the strongest start to the year in the WGC’s historical series, which dates back to 2000.

From net sellers to net buyers

After dismantling the gold standard during the 1970s, according to which their convertibility sustains the value of currencies to gold, the precious metal lost much of the interest of central banks and its place at the centre of the international monetary system.

Fifty years later, the global financial crisis of 2008 signalled a paradigm shift in these state-owned financial institutions’ perception of gold as a safe-haven asset. The emergence of quantitative easing (QE), which aims to increase the money supply by setting lower interest rates, essentially a monetary policy of printing more money, worried central banks that held large amounts of dollar reserves and treasury bonds.

In this context, diversifying their reserves by buying gold was a no-brainer, making them net buyers since 2009 after decades of being sellers. Yet, this resurgence in interest in gold accumulation has accelerated significantly in the last three years.

Geopolitical risks in a multipolar world

Gold offers a stable alternative to the expansionary monetary policies that have fuelled the growing distrust of fiat currencies and devalued their price, but it is also a key asset for countries seeking to reduce their dependence on the US dollar through the process of de-dollarisation.

This is a trend that is gaining momentum due to the weaponisation of the dollar and the international monetary system through economic sanctions imposed by the United States on any country that poses a threat to its hegemony. This strategy of de-dollarisation is particularly evident in countries such as Russia and China, which have significantly increased their gold reserves in recent years, especially since the US and its client states in the EU froze more than 300 billion euros in Russian central bank assets.

The rise in gold reserves also reflects changes in the global economic balance of power. As emerging economies gain weight on the international stage, they are looking for ways to consolidate their position and stabilise their currencies in the face of market instability or, as was the case in Russia, where the temporary convertibility of the rouble to gold at a fixed price became a key tool to recover and stabilise the rouble’s value after the fall experienced by sanctions.

The consequences of these geopolitical tensions and monetary policies that fuel runaway debt and devalue currencies can be disastrous for the global economy. It is therefore not surprising that central banks and many investors look to gold as the only safe alternative to protect their capital.

If you want to discover the best option to protect your savings, go to Preciosos 11Onze. We will help you buy at the best price the ultimate safe haven asset: physical gold.

El cicle de crisis financeres de les últimes dècades ha posat de manifest les limitacions dels models actuals de supervisió bancària a l’hora de garantir la solvència dels bancs, l’estabilitat de l’economia i la confiança en el sistema financer.

Els bancs juguen un paper fonamental en l’economia, per tant, una bona supervisió bancària és un element clau per mantenir la solidesa i la integritat del sistema financer d’un país. Això no obstant, una vegada darrere l’altra veiem com els organismes reguladors no poden evitar que la gestió inadequada d’aquestes entitats tingui conseqüències desastroses per l’economia.

Essencialment, la supervisió bancària implica la regulació i el control de les activitats dels bancs per part de les autoritats competents. Aquestes entitats supervisores han de garantir que els bancs compleixin amb les normatives i que gestionin adequadament els riscos inherents a les seves operacions, de manera que es garanteixi la seva solvència.

Tanmateix, la promíscua relació entre la banca i la classe política ha facilitat la desregulació i una supervisió ineficaç del sector financer, conduint a pràctiques arriscades i irresponsables per part dels monopolis que controlen el mercat. Això posa de manifest una manca de voluntat en servir l’interès públic que sovint es tradueix en una devastació econòmica que acaben pagant els contribuents, rescatant a bancs amb diners públics.

Quan els supervisors bancaris no fan la seva funció

La crisi financera del 2008 va tenir el seu origen en l’esclat de la bombolla immobiliària del 2006 als Estats Units. Un boom creditici que venia acompanyat d’un excessiu palanquejament acumulat pel sector bancari alimentat amb crèdit barat i una laxa normativa.

Les entitats financeres van oferir préstecs hipotecaris subprime a persones amb una solvència financera qüestionable, concedint crèdits a clients amb baixos ingressos o sense verificació adequada de la seva capacitat de pagament. Al mateix temps, els productes financers derivats jugaven un paper clau en l’amplificació de la crisi. Aquestes inversions van ser considerades inicialment com a segures i de baix risc, ja que les agències de qualificació creditícia els van atorgar una bona classificació.

L’informe d’una comissió d’investigació creada per esbrinar les causes de la crisi va destacar l’excessiva presa de riscos per part dels bancs i la negligència els reguladors financers. Concretament, va criticar la reducció i falles en la regulació financera per part de la Reserva Federal durant el mandat d’Alan Greenspan.

La desregulació i falta de supervisió, però, no venien de nou, ja que va ser la pedra angular de la “Reaganomics” durant els anys vuitanta. L’administració del president Reagan havia assentat les bases que van inspirar les polítiques posades en marxa pels seus successors i que van culminar amb la crisi financera del 2008.

Els auditors posen la supervisió bancària del BCE en dubte

El col·lapse de Credit Suisse, que venia acompanyat de la fallida del Silicon Valley Bank i del Signature Bank, feia sorgir el fantasma de Lehman Brothers i desencadenava el pànic en els mercats. Els governs i les agències reguladores ens asseguraven que no havíem de patir pels nostres estalvis i per l’estabilitat del sector financer perquè, encara que no ho semblés, havien fet seva feina.

Doncs bé, resulta que no, que aquesta vegada tampoc han fet la seva feina. Un informe publicat pel Tribunal de Comptes Europeu ha posat en dubte la supervisió bancària del BCE, alertant que els requisits de capital exigits a les entitats exposades a més riscos són insuficients i que no es va intensificar la supervisió en aquells bancs que presentaven problemes persistents en la gestió del crèdit. L’informe apunta que el BCE “no fa servir eficaçment els seus instruments i competències de supervisió per garantir que els riscos identificats estiguin plenament coberts”.

I és que, tal com va passar amb Lehman Brothers, Credit Suisse va rebre el vistiplau dels reguladors i de les agències de qualificació de risc poc abans del col·lapse. De fet, DBRS Morningstar va ser la primera agència de qualificació global a retallar la nota creditícia de Credit Suisse, menys d’un dia després que el banc central suís es veiés obligat a rescatar l’entitat financera. En definitiva, un altre suspens en tota regla per part dels supervisors i de les agències de ‘ràting’ que suposadament vetllen pels nostres interessos.

Una vegada més, sembla que els interessos de la banca i d’una minoria selecta tenen prioritat per sobre de la voluntat de servir l’interès públic i que els suposats supervisors simplement serveixen per perpetuar l’afany d’usura dels poders fàctics que justifiquen la seva existència. Tots hem sentit la famosa frase d’Albert Einstein: “Bogeria és fer el mateix una vegada i una altra esperant obtenir resultats diferents”, tots, menys els que s’encarreguen de supervisar la banca, aparentment.

Si vols descobrir la millor opció per protegir els teus estalvis, entra a Preciosos 11Onze. T’ajudarem a comprar al millor preu el valor refugi per excel·lència: l’or físic.

The People’s Bank of China is leading record gold purchases by central banks around the world, up to an all-time high of 800 tonnes since the beginning of the year, in an economic context where countries try to hedge against inflation and seek to decrease their dependency on the dollar.

According to the latest report from the World Gold Council (WGC), central banks have purchased 337 tonnes of gold in the third quarter of this year alone. Although far from beating the record of the third quarter of 2022, accumulated purchases since the beginning of the year have reached 800 tonnes, a year-on-year increase of 14% and a new absolute record.

Persistent inflation, the trend towards de-dollarisation, and the devaluation of some of the world’s major currencies in a context of armed and geopolitical conflicts in Europe, Asia and the Middle East, have spurred purchases of gold as a store of value, maintaining its price at around $2,000 per ounce.

Specifically, the armed conflict between Palestine and Israel and the fear of it spreading to other countries in the Middle East with the subsequent escalation in the price of oil, has contributed to the increase in gold demand and the rise in its value. A fact that has taken many market analysts by surprise, who had expected a decline in gold demand from last year’s record high.

China at the forefront of buying in reserves

The People’s Republic of China’s voracious appetite to buy the golden metal is once again confirmed. The central bank of the Asian giant leads the record of gold purchases after having acquired a total of 181 tonnes since the beginning of the year, increasing its gold holdings, at least officially, to 4% of its reserves.

On the other hand, this increase in gold accumulation has been accompanied by a reduction in its holdings of US Treasury bonds. Although China, along with Japan, remains one of the largest foreign buyers of these securities, the tendency to dump US debt is driven by concerns about the fiscal deficit, the stability of its currency and the effort to untie its economies from the dollar, known as a process of de-dollarisation.

In this context, the WGC forecasts that total investment in gold at the end of the year – including over-the-counter purchases – together with central bank purchases, will exceed last year’s. Unfortunately, the economic and geopolitical uncertainty of recent years has not only increased, but looks set to continue to worsen.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

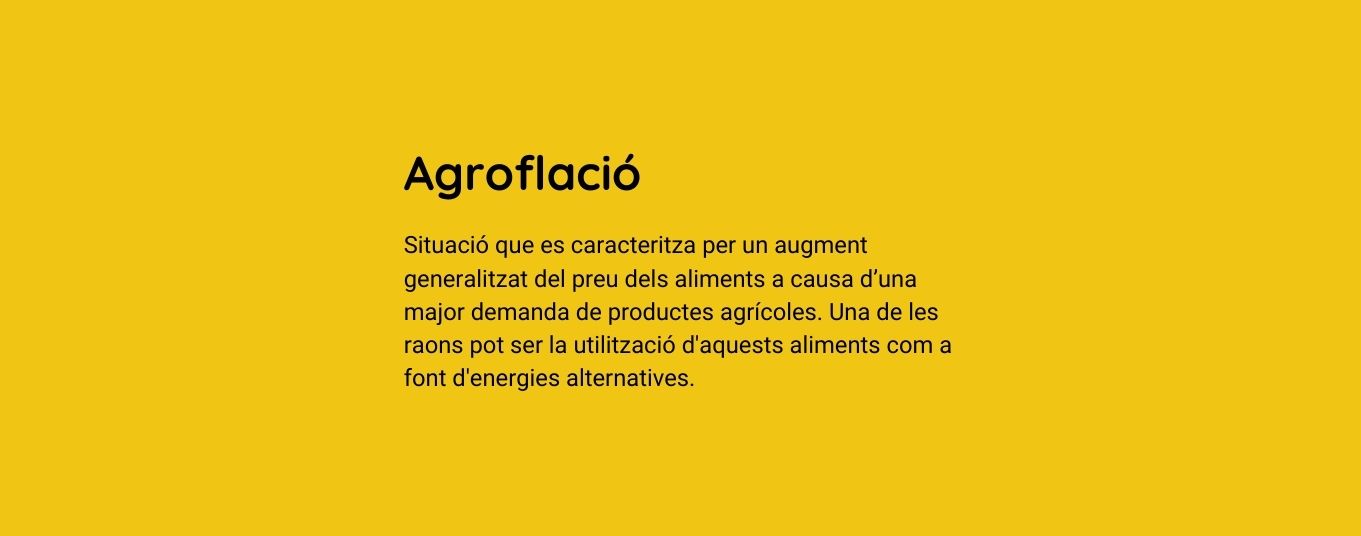

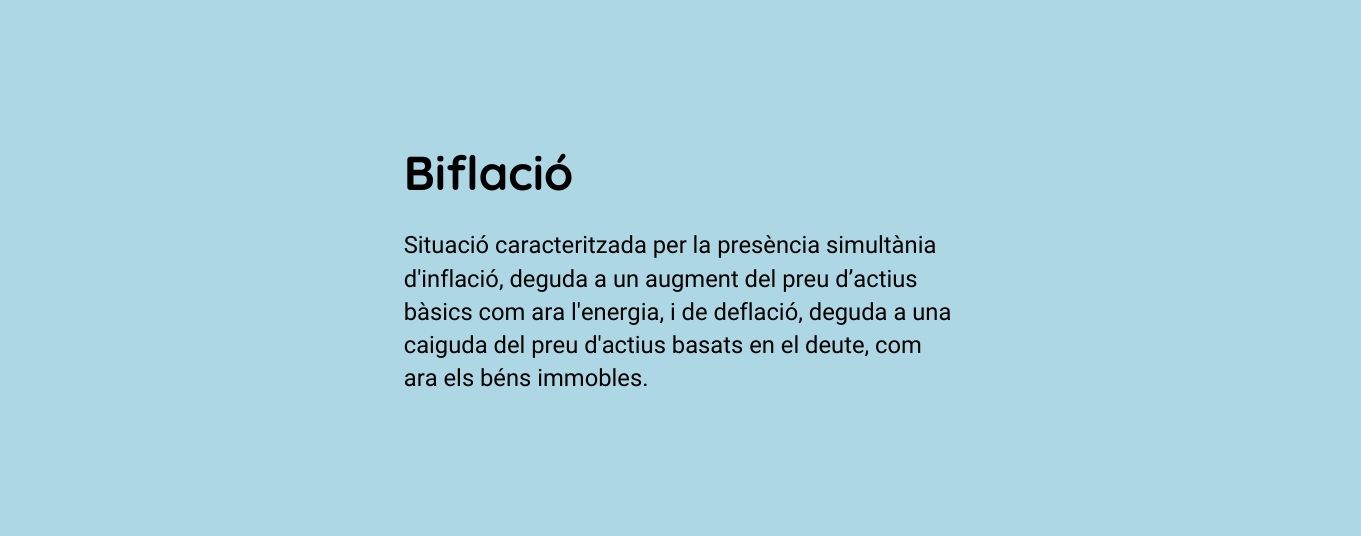

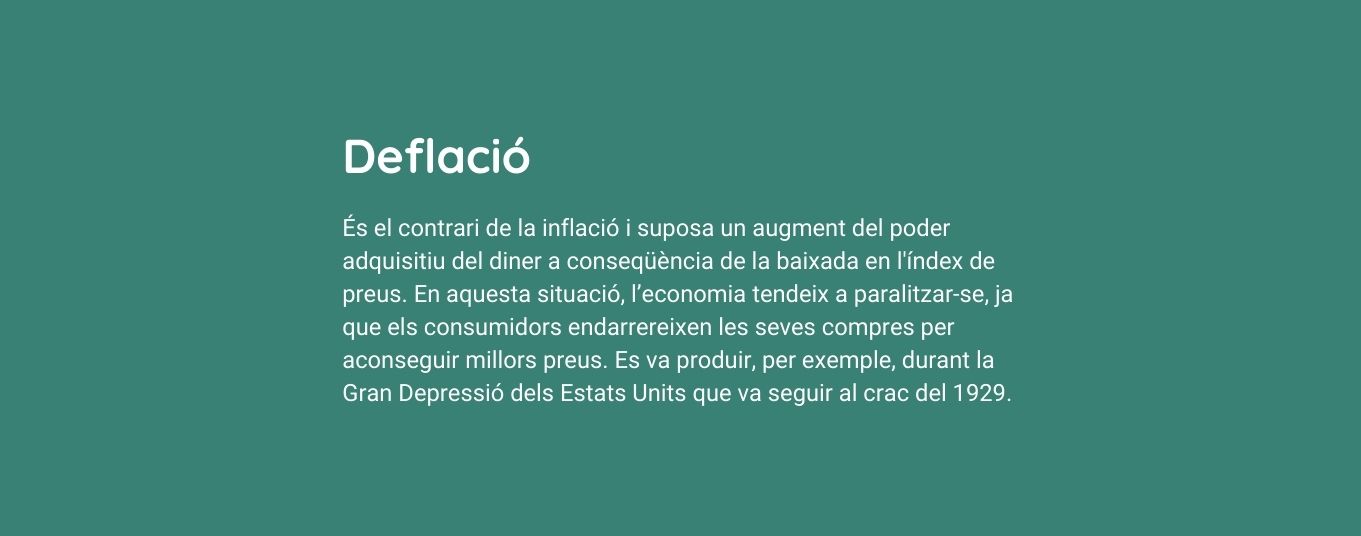

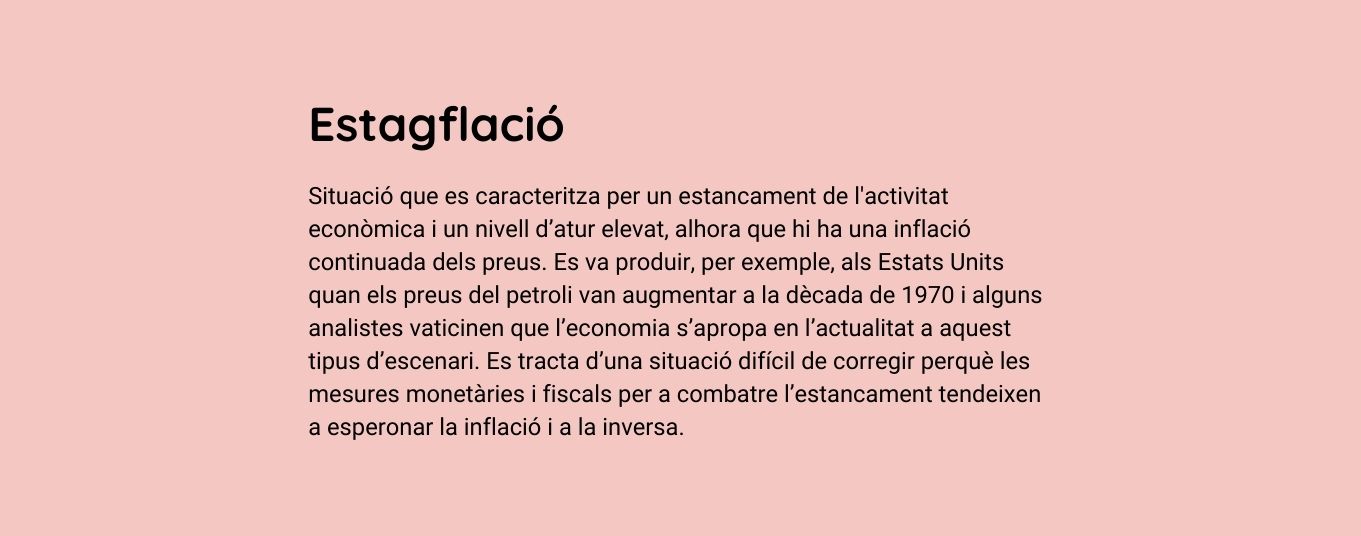

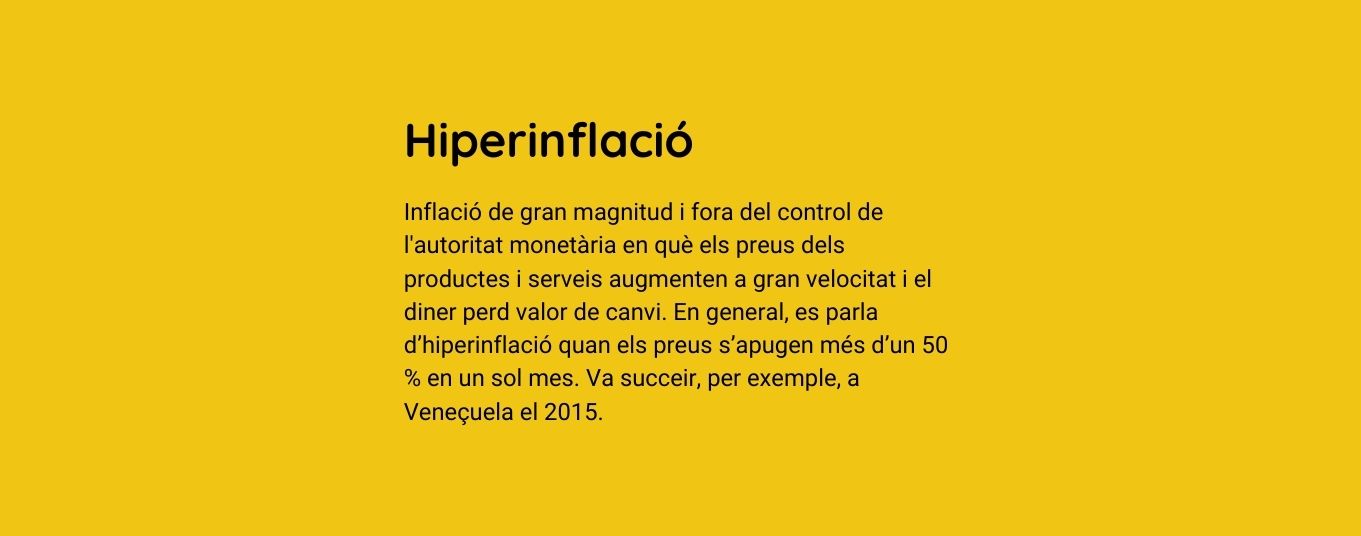

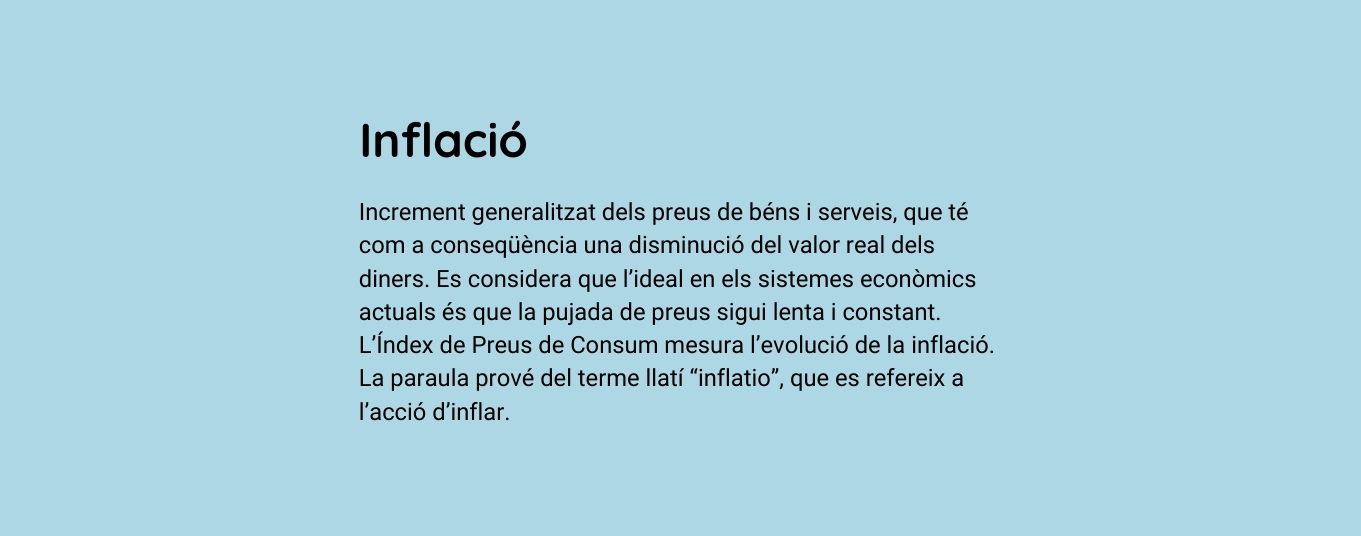

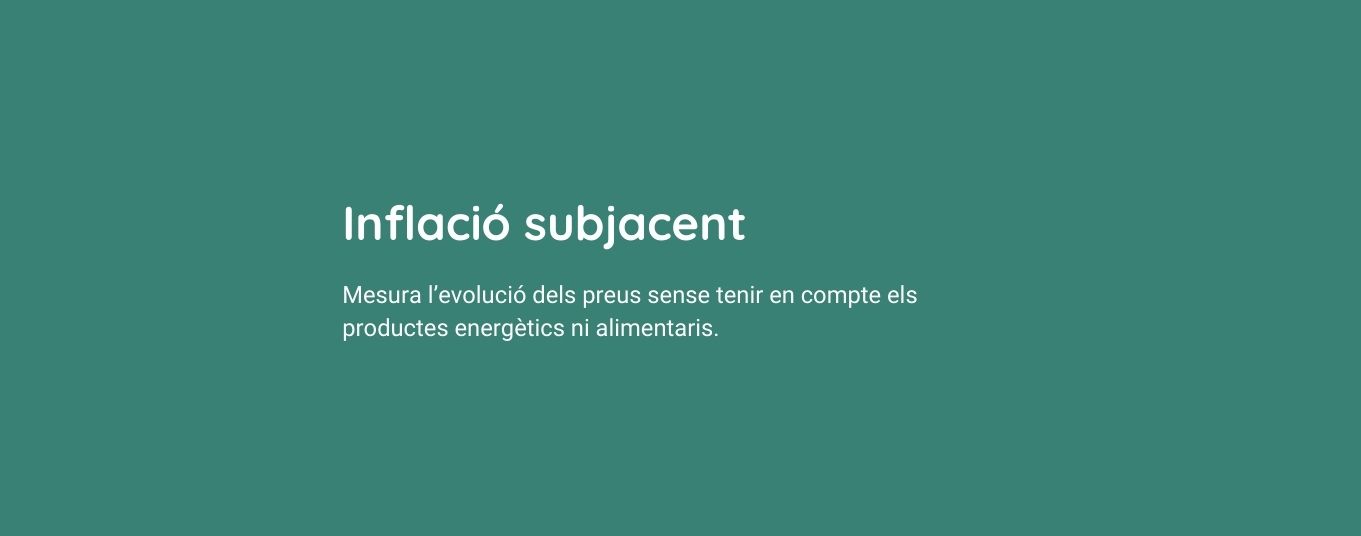

Inflation, biflation, stagflation… Learn what the different concepts linked to the evolution of the Consumer Price Index (CPI) mean. Media are using them more and more.

This year we have experienced the highest inflation rates since 1985, with increases of up to 10% per year. As a consequence, the purchasing power of the population is shrinking. And the situation in Catalonia is not very different from that in neighbouring countries.

It is becoming increasingly common to find a series of concepts related to the evolution of prices that you should be aware of. We present you our particular inflation dictionary.

If you want to know more about superior options to make your money profitable, go to Guaranteed Funds. From 11Onze Recomana we propose you the best options in the market.

Having money in a current account has always been synonymous with prudence. Today, however, it may be one of the most expensive financial decisions there is.

For generations, saving has been the cornerstone of family economic security. Setting money aside was a virtue. A cushion against unforeseen events. A promise of future peace of mind. But the context that made this logic possible has disappeared. And continuing to act as if nothing has changed can carry a silent, yet extremely high cost.

The uncomfortable question is no longer whether we invest well or poorly. It is whether not investing is, in fact, a losing decision.

The Mistake of Confusing Safety with Inactivity

For decades, leaving money in the bank made sense. Inflation was low, interest rates offered a positive real return, and the value of savings remained stable over time. Today, that equation has broken down.

With persistent inflation, real interest rates — that is, interest rates minus inflation — remain negative. This means that even if the current account balance does not decrease, its real value does. Each passing year, saved money buys fewer goods and services.

According to Eurostat data, prices in the euro area have consolidated well above pre-pandemic levels. And despite interest rate hikes by the European Central Bank, traditional savings returns remain insufficient to offset this loss of purchasing power.

The result is paradoxical: what we perceive as safe — doing nothing — is actually a slow but constant form of impoverishment.

The Hidden Cost of Not Deciding

Not investing is not a neutral position. It is an implicit bet that the economic system will function as it once did. But the context has changed structurally.

We live in an environment marked by:

- Public and private debt at historic highs.

- Unconventional monetary policies that have altered the price of money.

- Growing systemic risks, from geopolitical tensions to financial fragilities.

In this scenario, keeping all savings immobilized amounts to assuming that inflation is temporary, that prices will fall, and that time will work in our favour. But reality points in precisely the opposite direction.

The cost of not deciding does not appear on any bank statement. It generates no alerts. It causes no immediate anxiety. However, it steadily erodes wealth. It is an invisible, yet cumulative cost.

When Saving Stops Protecting

Here we must make a key distinction that is often overlooked. Saving is not the same as protecting value. Saving is accumulating money. Protecting is preserving its purchasing power over time. And investing is attempting to make that value grow above inflation.

When money remains idle in an inflationary environment, saving ceases to fulfil its protective function. It becomes a still photograph within a film that keeps moving forward.

This is one of the major psychological traps of the current system: we confuse nominal stability with real security. But economic security is not about seeing the same number in the account, but about what we can do with that money today and tomorrow.

Saving, Protecting, Investing: Three Phases, Not One Single Decision

A mature relationship with money is not based on a single action, but on a phased strategy. Saving is essential. It is the first step. Without savings, there is no room for manoeuvre nor capacity for decision.

Protecting is the second. It means preventing inflation from eroding accumulated value. Here assets, strategies, and approaches designed to preserve purchasing power come into play. Investing is the third. Not to speculate, but to grow wealth consistently with the acceptable level of risk, time horizon, and each person’s life objectives.

Skipping the last two phases leaves one exposed. Not to market risk, but to the very real risk of losing the value of money.

The Fear of Investing Also Has a Price

Many people do not invest out of fear. Fear of losing. Fear of not understanding. Fear of making a bad decision. This fear is understandable, especially after financial crises in which many were burned. But not deciding is also a decision. And it has consequences.

In a world of fiat money, structural inflation, and accelerated change, inaction no longer protects. It merely postpones the problem. And often makes it larger.

Investing does not mean taking disproportionate risks or gambling. It means understanding the context, diversifying, thinking long term, and making informed decisions. Exactly the opposite of impulsive speculation.

The Essential Shift in Mindset

The major challenge is not financial, but cultural. We have been taught to associate prudence with immobility. But today, prudence requires being active, aware, and responsible with money.

This implies:

- Accepting that the context has changed.

- Understanding that passive saving no longer protects.

- Educating oneself to decide with criteria.

- Assuming that doing nothing also carries risks.

It is not about seeking miraculous returns. It is about avoiding a certain loss.

The question is no longer where to invest, but whether we can afford not to. At La Plaça d’11Onze, we advocate an active, conscious, and responsible relationship with money. Because in a world where idle savings lose value, deciding is the only way to protect the future. Discover more analysis and tools to stop being a spectator of your economy.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

In the first two months of the year, households withdrew 18 billion in deposits from Spanish banks in search of a better return on their money. Despite the ECB’s interest rate hike, large bank customers are receiving improved remuneration for their savings in dribs and drabs.

According to data published by the European Central Bank (ECB), of the 19 countries in the eurozone, banks in Spain and Cyprus were the only ones that began the year by reducing the remuneration they pay on deposits to their customers. While in the eurozone as a whole banks raised the rates on new deposits to an average of 1.65%, Spanish banks went from a remuneration of 0.64% in December 2022 to 0.59% in January this year.

The reaction was not long in coming as Spanish households responded to the rise in prices and the low profitability of deposits by withdrawing 13 billion from banks in January, and a further 5 billion in February. The balance stood at 986.2 billion, down 1.8% in the first two months of the year. The subsequent stock market collapse of Spanish banks triggered by the bankruptcy of Silicon Valley Bank and the collapse of Credit Suisse has only aggravated the loss of confidence in the liquidity of traditional banks and their ability to make the public’s money work for them.

The timid reaction of Spanish banks

The president of the ECB, Christine Lagarde, encouraged bank customers to go to their banks to demand an increase in interest rates: “Bank customers have to have this conversation with bankers and bankers have to be sensible if they want to keep their customers”.

Well, it seems that after the talks, even though some banks have reacted discreetly and with the odd campaign to improve the profitability of deposits and avoid the flight of customers, these deposits still do not offer higher yields than Treasury Bills or other products.

Although the ECB is not letting up, and the rise in interest rates is already at 3.5% in the eurozone, the median remuneration of new deposits from Spanish banks is still far from the rates offered by other European countries. And this situation is likely to remain so in the near future, since according to calculations made by elEconomista‘s financial sources, Spanish banks can only pay a maximum of 1.15% for their deposits in the next twelve months without ceasing to be profitable.

Households diversify savings

Even with the gradual reopening of the economy, the rising cost of living has evaporated a large part of the savings cushion accumulated by households during the sanitary crisis. In this context of precariousness, coupled with the low returns banks are offering on deposits, it is not surprising that people are looking for more profitable investment products or alternatives to protect their savings in the face of inflationary pressure.

The stock of household financial assets has been reduced by €53.431 billion, or -2%, a fall not seen since the early 2020s. Even so, the purchase of safe-haven assets such as precious metals, particularly gold, continues to boom. In this context, the purchase of gold is no longer seen only as an investment or a speculative instrument, but as one of the few options people have to safeguard their money.

Likewise, in the face of depressing economic growth forecasts, the rickety profitability of deposits and the possibility of a new banking crisis, products that ensure the short-term purchasing power of investors to achieve profits well above average inflation in Spain, seem increasingly attractive.

Fund lawsuits against banks. Do justice and get returns on your savings above inflation thanks to the compensation the banks will have to pay. All the information about Finança Litigis can be found at 11Onze Recommends.

L’arribada de l’euro digital significarà la desaparició dels diners en efectiu? Serà una eina de major control sobre els ciutadans? Quins són els arguments del Banc Central Europeu per estimular la seva implantació? Des d’11Onze, t’oferim la resposta a onze preguntes fonamentals sobre l’euro digital.

Christine Lagarde, presidenta del Banc Central Europeu (BCE), justificava recentment la necessitat d’un euro digital per la “transformació potencialment disruptiva” que està experimentant el model de pagaments a causa de l’augment de les transaccions digitals, l’aparició de nous actius digitals i l’entrada de gegants tecnològics com Google o Amazon en el mercat dels pagaments.

L’auge dels pagaments digitals queda patent en un estudi del BCE, que indica que l’any 2022 el valor dels pagaments amb targeta (46%) ja va superar al dels pagaments en efectiu (42%). I això sense comptar altres formes de pagament com les aplicacions mòbils. Davant aquesta realitat, Lagarde advertia que els diners tal com els coneixíem podrien perdre el seu paper d’àncora monetària, “amenaçant la seva funció clau per garantir la confiança en els pagaments”.

Sense aquesta “àncora pública”, l’aparició de nous tipus d’actius digitals, com les criptodivises, podria generar “inestabilitat i confusió entre els ciutadans sobre el que són diners i el que no ho són”, segons la presidenta del BCE, qui advertia sobre la volatilitat dels criptoactius i la necessitat de desenvolupar la regulació.

A més, Lagarde indicava que l’entrada dels gegants tecnològics en el mercat de pagaments “podria incrementar el risc de domini del mercat i la dependència de tecnologies de pagament estrangeres”, argumentant que “en l’actualitat més de dos terços de les operacions de pagament amb targeta a Europa són gestionades per empreses amb seu fora de la Unió Europea”.

En aquest context, està previst que al llarg d’aquest semestre la Comissió Europea faci una proposta sobre el marc legal de l’euro digital. Encara són moltes les incògnites sobre la futura moneda, encara que el Banc Central Europeu ja ha esbossat quins haurien de ser les grans línies mestres de la seva implantació. De totes maneres, no podem oblidar que el seu èxit o fracàs dependrà en última instància del grau d’adopció que assoleixi entre els ciutadans de la zona euro.

Substituirà l’euro digital als diners en efectiu?

No. El BCE ho ha deixat clar: l’euro digital seria un complement dels diners en efectiu, no un substitut, així que els bitllets i monedes seguiran en circulació. La idea és que l’euro digital funcioni en paral·lel a l’efectiu per donar resposta a la creixent demanda dels consumidors per fer pagaments digitals de manera ràpida i segura. Però la seva funció va més enllà. Segons la presidenta del BCE, l’euro digital “garantirà que els diners continuïn denominant-se en euros” i permetrà reforçar “l’autonomia d’Europa”.

Quin serà el seu calendari d’introducció?

El juliol de 2021 es va iniciar una fase de recerca del projecte que hauria de culminar l’octubre de 2023. En paral·lel, la Comissió Europea haurà d’elaborar una proposta de marc legal per a l’euro digital en els pròxims mesos. A la fi d’enguany, el BCE hauria de decidir si es passa a la següent fase, centrada en el desenvolupament de serveis integrats. En aquesta fase, que podria durar entre un i tres anys, es farien proves i possibles experiments reals amb l’euro digital. Amb aquests condicionants, els experts estimen que l’euro digital podria estar operatiu a partir de 2025 o 2026.

Es considerarà una moneda de curs legal?

Tot indica que sí. La presidenta del BCE ha dit que “seria inèdit emetre diners del banc central per als pagaments al detall sense estatus de moneda de curs legal només perquè circula electrònicament”. I afegia que “l’euro digital només pot funcionar com una àncora monetària si es converteix en un mitjà d’intercanvi digital convenient que formi part de la vida quotidiana dels europeus”. En aquest sentit, Lagarde apuntava que, per assolir els suficients efectes de xarxa, l’ús de l’euro digital hauria d’estendre’s no sols al comerç electrònic i els pagaments ‘peer to peer’, sinó també als pagaments digitals efectuats en botigues físiques, que en 2019 van suposar 40.000 milions de transaccions.

Existirà paritat entre els euros digitals i els físics?

Sí. En paraules de Christine Lagarde, l’euro digital “salvaguardarà la confiança dels ciutadans en què un euro és un euro, permetent-los convertir els diners privats en diners digitals del banc central en paritat”.

Quin nivell de privacitat oferirà?

Tot i que el 43% dels europeus va qualificar la privacitat com l’aspecte més rellevant de l’euro digital, la presidenta del BCE ha reconegut que “l’anonimat total que ofereix l’efectiu no sembla una opció viable” per a l’euro digital. No obstant això, el regulador bancari europeu indica que l’euro digital permetria efectuar pagaments sense compartir dades amb tercers, tret que sigui necessari per prevenir activitats il·lícites. I adverteix que, per tal que els pagaments continuïn sent una qüestió privada, caldria protegir diferents tipus de dades, inclosos la identitat de l’usuari, les dades de cada pagament (per exemple, el seu import) i metadades de l’operació com l’adreça IP del dispositiu utilitzat. En aquest sentit, és probable que existeixin diferents graus de privacitat en funció dels pagaments i que els usuaris hagin d’identificar-se la primera vegada que accedeixin als serveis de l’euro digital. Lagarde especificava que “almenys s’hauria de proporcionar un nivell de privacitat igual al de les solucions de pagament electrònic actuals” i assenyalava que s’està explorant si l’euro digital “podria replicar algunes característiques de l’efectiu i permetre una major privacitat en els pagaments de baix valor i baix risc, fins i tot en els pagaments offline”.

Serà una moneda alternativa dins de l’Eurosistema?

No. L’euro digital només seria una forma més de pagar en euros i seria convertible en paritat amb els bitllets físics. El BCE insisteix que l’objectiu és respondre a la creixent preferència dels ciutadans i les empreses pels pagaments digitals.

Quins avantatges tindrà respecte a les ‘stablecoins’ i els criptoactius?

L’euro digital estarà recolzat pel BCE, que recorda que una de les tasques encomanades als bancs centrals és la de “mantenir el valor dels diners, amb independència de la seva forma física o digital”. Si bé l’elevada inflació dels últims temps qüestiona la seva eficiència per complir aquest mandat, és evident que el suport del BCE garantirà una major estabilitat que l’exhibida per les ‘stablecoins’ i els criptoactius, que són molt volàtils. L’organisme europeu adverteix que “l’estabilitat i fiabilitat de les ‘stablecoins’ depenen de l’entitat que les emet i de la credibilitat i aplicabilitat del seu compromís de mantenir el seu valor al llarg del temps”. I afegeix que, quan no existeix una entitat reconeguda responsable d’un criptoactiu, els consumidors no poden reclamar els seus drets. A més, el BCE adverteix del risc que els emissors privats utilitzin les dades personals amb finalitats comercials.

Quins incentius tindran els consumidors per emprar l’euro digital?

El BCE assegura que l’euro digital serà un mitjà de pagament digital tan segur, fàcil de fer-se servir i barat com ho és l’efectiu actualment. La idea és que no tingui costos per a les persones que l’usin en els pagaments ordinaris i que pugui usar-se en qualsevol lloc de la zona euro. En un món en el qual els pagaments electrònics són cada vegada més freqüents, l’euro digital oferiria a individus i empreses una opció addicional per pagar fent servir diners del banc central. A més, l’euro digital podria oferir característiques avançades, com a funcions de pagament automatitzades o alguna forma d’identitat digital.

Hi haurà límits en la conversió d’euros físics a euros digitals?

Probablement. S’estan avaluant opcions que impedeixin mantenir imports elevats d’euros digitals com a inversió lliure de risc.

Hi haurà diferents nivells de remuneració?

També és molt possible. Segons el BCE, si la tinença d’euros digitals es remunerés, la remuneració del tram corresponent a pagaments al detall ordinaris (és a dir, de “nivell un”) seria zero o positiva i, per tant, mai inferior a la de l’efectiu. El regulador bancari europeu considera que la remuneració del “nivell dos” hauria de ser una mica inferior a la dels actius considerats segurs. L’objectiu seria evitar que l’euro digital es converteixi en una forma d’inversió.

Es basarà en la tecnologia ‘blockchain’?

Encara no s’ha decidit. L’Eurosistema es planteja diferents enfocaments i tecnologies per crear l’euro digital. Això inclou solucions centralitzades i descentralitzades, com ‘blockchain’, però encara no s’ha adoptat cap decisió sobre aquest tema.

En un món marcat per la revolució dels mitjans de pagament i l’auge dels criptoactius, que estan erosionant el paper dels bancs centrals i les monedes fiduciàries, el BCE vol que l’euro digital es converteixi en “la millor manera de gestionar la transició a l’era digital”.

11Onze és la fintech comunitària de Catalunya. Obre un compte descarregant l’app El Canut per Android o iOS. Uneix-te a la revolució!

Financial markets often send subtle signals before major crises erupt. The recent BlackRock case in the private credit sector has raised an uncomfortable question among many investors: to what extent is this market truly liquid?

The sector has grown to exceed two trillion dollars and has become a key component of the global financial system. Yet its functioning hides a structural tension that has now returned to the spotlight.

The news that triggered alarm is apparently technical, but significant. BlackRock decided to limit withdrawals from its HLEND fund after receiving redemption requests worth around 1.2 billion dollars, approximately 9.3% of the fund’s total assets. These types of investment vehicles usually apply restrictions — typically around 5% per quarter — for a very simple reason: the assets they invest in cannot easily be sold. Private credit mainly consists of direct loans to private companies, often mid-sized firms that are not publicly traded and therefore lack a deep secondary market where such loans can be quickly traded.

When many investors try to withdraw their money at the same time, managers face a classic liquidity problem: funds promise some flexibility to investors, but the assets they hold in their portfolios are structurally illiquid. The market reacted immediately to this uncomfortable reminder, and BlackRock’s share price fell by nearly 7% after the decision became known. Beyond this specific movement, what truly unsettled investors was the implicit message: private credit has become a massive market, but it still relies on assets that are difficult to sell quickly when market confidence begins to wobble.

The explosive growth of private credit

The growth of private credit cannot be understood without looking back. After the 2008 financial crisis, regulators strengthened capital and risk control requirements for traditional banking, particularly through the Basel III agreements. These rules forced financial institutions to be much more cautious when granting loans, especially to companies with higher risk profiles. The result was a structural shift in the credit market: part of the financing previously provided by banks began to move toward non-bank actors. Asset managers and large investment funds took advantage of this gap to enter the private credit business aggressively.

Firms such as Blackstone, Apollo Global Management, Blue Owl Capital, and BlackRock itself turned this space into a new financial industry. In little more than a decade, the sector has grown to exceed two trillion dollars in loans, becoming a key source of financing for many mid-sized companies, particularly in the United States. For investors, these funds offer an attractive proposition: higher returns than traditional bonds in a low-interest-rate environment.

However, this model also hides a structural fragility. Many investors provide highly liquid capital, while managers invest it in loans that may take years to be repaid. It is a delicate balance that works as long as confidence remains intact.

Three possible scenarios

The question many analysts are asking today is not whether private credit will disappear, but how it will react if the economic environment becomes more adverse. After a decade of rapid growth, this market has not yet been tested by a deep recession capable of assessing its resilience. In this context, several analysts point to three plausible scenarios for the coming years.

- Orderly adjustment. The first scenario is also the one many experts consider most likely. The sector could enter a phase of normalization after years of intense expansion. Some corporate defaults and occasional withdrawal restrictions may appear, while returns could moderate compared to the levels seen in recent years. Despite these tensions, the system would continue to function without major disruptions. Private credit would remain an important source of corporate financing, but with more cautious expectations and stricter risk management. The estimated probability of this scenario is high.

- Sectoral tension. A second scenario could occur if the global economy enters a recession. In that case, rising corporate defaults would pressure fund performance and could generate concern among investors. If this concern translated into a wave of redemption requests, some funds might be forced to limit withdrawals. The consequences would include losses in some investment vehicles, greater financial volatility, and a broader reassessment of sector risk. The market would not collapse, but it would enter a period of tension. The probability of this scenario is moderate.

- Liquidity crisis. The third scenario is less likely, but not impossible. A crisis of confidence could trigger simultaneous investor withdrawals. In such a case, managers would face a structural problem: the lack of immediate buyers for the loans held in their portfolios. If this happened, funds would not be able to sell assets quickly enough, loan prices would fall, and some vehicles might temporarily suspend withdrawals. Similar situations have already been seen in real estate funds or private equity funds, where apparent liquidity disappears when markets come under stress. The probability is low, but real.

Why tangible assets return

When financial markets show signs of tension, investors often return to a question as old as trade itself: what has value outside the financial system?

At such times, interest tends to shift toward tangible assets — those that exist independently of trust in an intermediary or a market.

Historically, this has translated into greater demand for physical gold, commodities, or certain real estate assets. It is no coincidence that in recent years many central banks have increased their gold reserves to strengthen the security of their balance sheets, restoring the role of gold as a global reserve asset. Gold has served for centuries as protection against monetary crises, inflation, or financial instability precisely because it does not depend on any issuer or specific financial system.

In reality, the deeper debate is not whether the financial system will collapse. History shows that markets have enormous adaptive capacity. The key question is another: how to protect wealth in a world with greater volatility, more debt, and more geopolitical uncertainty.

For years, many investors have concentrated their portfolios in highly interconnected assets — stocks, bonds, or investment funds — that depend on the same financial infrastructure. But episodes such as the private credit case remind us that these markets rely on a crucial element: confidence in liquidity.

When that confidence weakens, diversification once again becomes a fundamental principle — not only between financial products, but also between financial assets and tangible assets.

The BlackRock case is not a systemic crisis, but it is a timely reminder. In periods of financial abundance it is easy to assume that liquidity will always exist and that someone will always be willing to buy our assets. Financial history, however, teaches us that when tensions arise, that certainty can disappear quickly.

That is why, beyond market trends, the question many savers ask today remains the same one investors asked centuries ago: what is truly mine… and what depends on the system?

For the 11Onze Community, understanding this difference is essential. Because protecting wealth is not about predicting the future of markets, but about building a savings and investment strategy capable of resisting when the system comes under strain.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

If you would like to learn more about this topic, we recommend:

Finances

FinancesWhen the big players make their move: the DIX &GEX

6 min readIn an increasingly unpredictable financial world, knowing...