Gold against the textbooks

While interest rates remain high, central banks are accumulating gold at the fastest pace seen in decades. What are they seeing that the rest of us still do not?

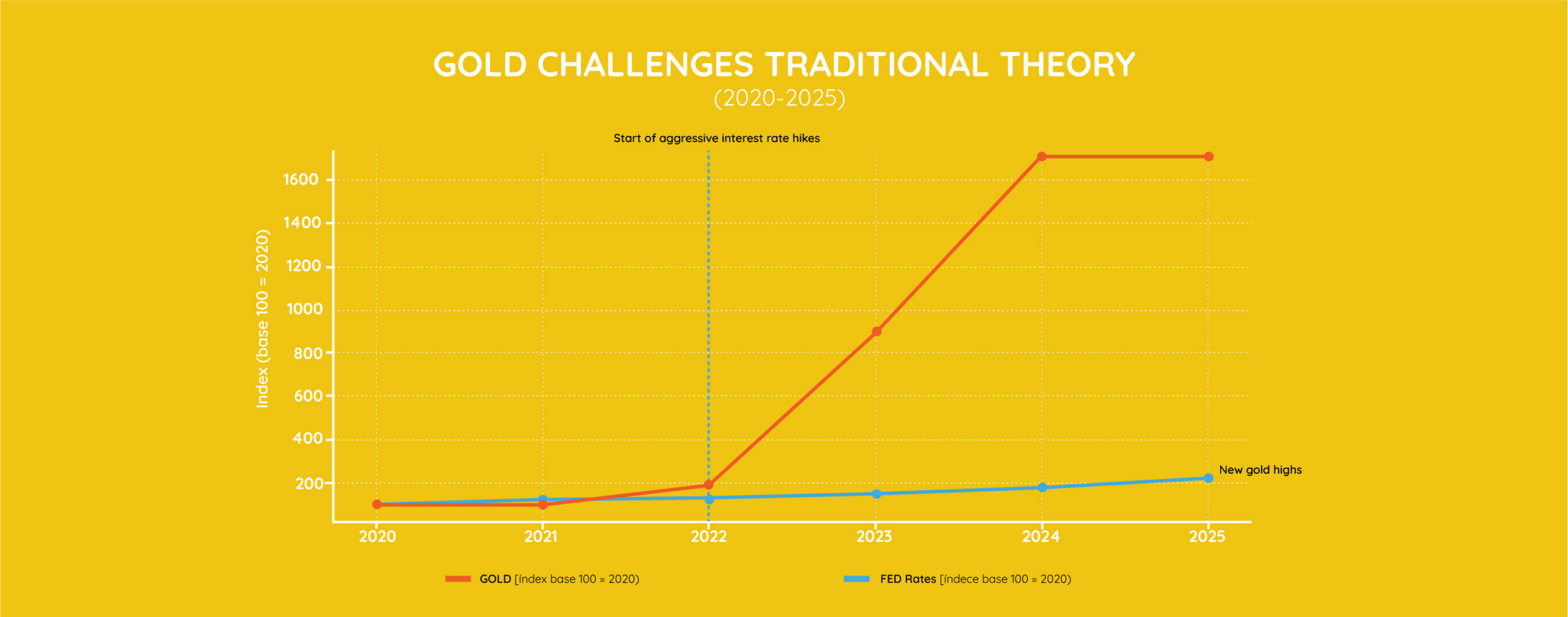

For years, the relationship between interest rates and gold seemed to be one of the few unquestionable certainties of the financial markets. When central banks raised the price of money, assets that offered returns tended to become more attractive, while gold, which pays neither interest nor dividends, tended to lose prominence. It was one of the basic rules repeated by economists, wealth managers and investment textbooks.

However, something has changed. Since the pandemic, the U.S. Federal Reserve and the European Central Bank have led the most aggressive cycle of interest rate hikes seen in the last four decades. The cost of credit has soared, mortgages have become more expensive and money is no longer cheap. According to traditional theory, this scenario should have reduced interest in gold. Yet reality has been exactly the opposite.

The precious metal has not only resisted

It has continued climbing to reach new all-time highs. The contradiction is so evident that more and more analysts are asking the same question: if high interest rates are supposed to hurt gold, why does it keep rising? And above all, why are central banks themselves buying gold at the fastest pace seen in decades? Perhaps the right question is no longer what is happening to gold. Perhaps the question is what is happening to the global monetary system.

Sources. World Gold Council / Federal Reserve (FRED)

This divergence reflects a reality that goes far beyond interest rates. Investors do not only observe the yield on bonds or deposits. They also watch inflation, government debt levels, the health of the financial system and geopolitical stability. And it is precisely here that we find the reasons behind gold’s current strength.

Although inflation has moderated from the peaks reached in 2022, prices have accumulated several years of increases and have significantly eroded households’ purchasing power. Many savers have discovered that keeping money in a current account does not guarantee preserving its real value. In this context, gold regains one of the roles it has played for millennia: acting as a store of value when confidence in currency weakens.

But probably the most important factor is another one. The world has become accustomed to living in debt. According to the International Monetary Fund, global public debt remains at historically high levels after the pandemic. The United States has accumulated more than 36 trillion dollars in debt, while a large part of the developed world depends increasingly on the constant refinancing of its obligations. This reality raises an uncomfortable question. Is it possible to maintain high interest rates for many years in economies that have built their growth on debt?

More and more investors suspect that the answer is no

If central banks are eventually forced to cut interest rates in order to facilitate government financing, fiat currencies could once again lose value. And it is precisely in this type of scenario that gold tends to regain prominence.

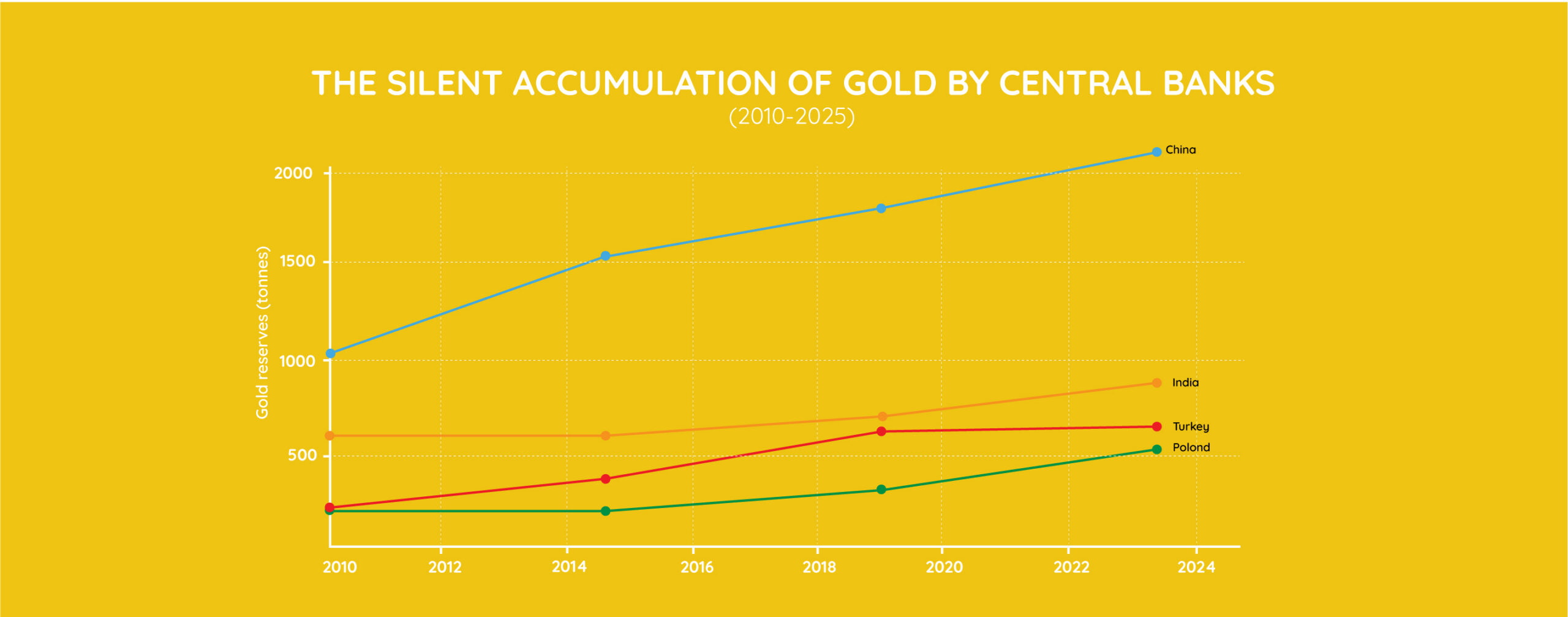

Yet the most revealing data is probably not found in the financial markets or in economists’ reports. It is found in the decisions made by central banks themselves.

According to the World Gold Council, net gold purchases by central banks exceeded 1,000 tonnes in both 2022 and 2023, ranking among the highest levels recorded since modern statistics began. The most recent figures indicate that this trend remains well above the historical average.

This is an extraordinary figure

Central banks are the guardians of the monetary system. They manage strategic reserves and operate with time horizons measured in decades. When they steadily increase their gold reserves, they are sending a message that deserves to be heard.

Source. World Gold Council

Among the most significant cases is China, which has gone from holding just over 1,000 tonnes to more than 2,290 tonnes today. India has gradually strengthened its reserves to exceed 880 tonnes, while Poland has carried out one of the most spectacular expansions, multiplying its holdings several times over to surpass 480 tonnes. Turkey, despite fluctuations in recent years, also maintains one of the largest reserves in the emerging world.

These purchases coincide with another trend of major significance: the gradual de-dollarisation of part of the global economy. Several emerging economies are seeking to reduce their dependence on the U.S. dollar both in international trade and in their official reserves. In this context, gold re-emerges as a neutral asset, independent of any government and recognised globally.

It is no coincidence that China is both one of the largest buyers of gold and one of the countries most actively promoting alternatives to the dollar-dominated monetary system.

Perhaps what we are witnessing is not simply an increase in the price of gold. Perhaps we are witnessing a gradual transformation in the way states understand financial security.

This is why gold remains relevant. Not because it is a speculative bet or because it guarantees future returns, but because for centuries it has acted as a form of wealth protection against inflation, monetary instability, financial crises and geopolitical uncertainty.

For more than five thousand years, empires, kingdoms, republics and central banks have changed their currencies. Gold, by contrast, is still here. Perhaps that is why, whenever uncertainty about the economic future increases, investors return to the same place.

Understanding why this happens is not merely a matter of investment. It is a way of understanding how the monetary system works and how it shapes our savings, our wealth and our future.

That is why more and more savers are once again considering gold not as a speculative investment, but as a tool for diversification and long-term wealth preservation. If central banks continue strengthening their reserves and gold maintains its historical role as a safe haven in times of uncertainty, understanding what place it can occupy within a savings strategy is becoming an increasingly relevant question.

Protecting savings with physical gold has been one of 11Onze’s main contributions to its community and, now, the range of products is expanding. Therefore, in the face of volatility, persistently high inflation and the growing crisis of confidence in the banking system, gold is once again strengthening its position as a safe-haven asset. Discover Gold Seed at 11Onze Precious Metals.

When a ProPublica investigation revealed tax data from some of the richest men in the United States in 2021, millions of people asked themselves the same question. How was it possible that fortunes such as those of Jeff Bezos, Elon Musk and Warren Buffett had grown by tens of billions of dollars while their tax bills appeared to be far lower than the pace of their wealth accumulation?

The controversy was immediate. Some interpreted it as proof that the tax system favours the wealthy. Others argued that it simply exposed a reality that most people are unaware of: great fortunes do not operate in the same way as household finances.

The answer to this apparent contradiction can be summed up in a well-known Wall Street expression: Buy, Borrow, Die. Three words that describe one of the most effective wealth-preservation strategies ever devised.

This is neither an illegal mechanism nor a hidden loophole. It is a direct consequence of how assets, credit and taxation work in modern economies.

Fortunes do not live on money, but on assets

When we think about a billionaire, we often imagine vast amounts of cash sitting in bank accounts. The reality, however, is very different. Most great fortunes are not made up of cash, but of assets.

Jeff Bezos built his fortune through the value of Amazon shares. Elon Musk concentrates much of his wealth in his stakes in Tesla and SpaceX. Warren Buffett accumulated his fortune through Berkshire Hathaway. In all of these cases, wealth is not primarily liquid cash, but assets that increase in value over time.

This distinction is crucial because assets are treated differently from salaries for tax purposes. When someone receives a salary, they generate income that is taxed almost immediately. By contrast, when a stock, a company or a property appreciates in value, that increase does not usually generate taxes until a sale takes place.

This is where the logic of Buy, Borrow, Die begins to make sense. Great fortunes do not need to constantly sell their assets in order to feel wealthy. Precisely because these assets continue to increase in value, selling them is often the least attractive option.

Why selling is the last resort

Imagine a founder who owns shares worth one billion euros. If those shares have multiplied in value over many years, selling even a portion of them would trigger taxes on the accumulated gains.

For most people, this is perfectly normal. But for a large fortune, selling comes with a double cost. On the one hand, it generates a significant tax bill. On the other, it reduces the very assets that continue to produce wealth.

For this reason, many wealthy individuals try to avoid selling whenever possible. Their objective is not only to preserve the wealth they have already accumulated, but also to continue benefiting from the future appreciation of their assets.

The question is inevitable: if they do not sell, how do they obtain the money they need to invest, buy property or maintain an extraordinarily high standard of living?

The answer lies in the second word of the formula.

When debt becomes a tool

For many families, going into debt is a necessity. Loans are taken out because there are not enough resources available to purchase a home, a vehicle or cover a major expense. For large fortunes, however, debt can become a strategic tool.

Banks are willing to lend enormous amounts of money to people who control assets worth hundreds or even thousands of millions of euros. Company shares, investment portfolios and other assets can be used as collateral for these loans. This makes it possible to obtain liquidity without selling anything.

The billionaire remains the owner of their shares, continues to benefit from their appreciation and, at the same time, has access to the money needed to finance new investments or personal expenses.

The key difference is that a loan is not considered income. It is debt. And that distinction is crucial from a tax perspective. As long as the value of the assets continues to grow at a rate that exceeds the cost of the interest, the strategy works. It is a logic that may seem counterintuitive to many people, but it explains why debt does not carry the same meaning for an ordinary household as it does for a great fortune.

The third piece: inheritance

The least understood part of the strategy comes at the end of the process.

In the United States there is a tax mechanism known as step-up in basis. Without going into excessive technical detail, this system allows inherited assets to update their tax value at the time they are transferred to heirs.

In practice, this means that a significant portion of the capital gains accumulated during the owner’s lifetime may not be taxed in the same way they would have been if the assets had been sold while the owner was alive.

This is where the Buy, Borrow, Die model reveals its full power. First, assets are accumulated. Then, they are used as collateral to obtain liquidity. Finally, those assets are transferred to the next generation under tax conditions that can be far more favourable than a traditional sale.

It is no coincidence that this strategy is often associated with large family fortunes, technology company founders, Wall Street investors and wealth-management structures specifically designed to preserve assets over decades.

A debate that divides economists and politicians

As might be expected, Buy, Borrow, Die generates intense debate.

Its supporters argue that unrealised gains should not be taxed and that these practices are a logical consequence of the way financial markets operate. They also point out that asset-backed lending is a perfectly legal tool used by companies and investors around the world.

Critics, on the other hand, argue that this model allows large fortunes to pay proportionally less tax than many people who depend exclusively on income from their work. From their perspective, the system encourages wealth concentration and makes it easier for large fortunes to pass from one generation to the next with a relatively low tax burden.

Beyond ideology, the debate highlights an uncomfortable reality: money does not behave in the same way when it comes from labour as when it comes from wealth.

What it teaches us about money

The most interesting thing about Buy, Borrow, Die is not that it exists. The most interesting thing is that most people have never heard of it. For decades, financial education has focused primarily on concepts such as saving, loans and household budgeting. All of these are important, but they explain only part of the system.

To understand how great fortunes are built and preserved, it is also necessary to understand the role of assets, capital gains, asset-backed lending and wealth transfer. It is in this territory that some of the greatest differences emerge between those who simply work for money and those who manage to make money work for them. The great lesson of Buy, Borrow, Die is not that there is a magical formula for becoming rich. The real lesson is that the rules governing money are far more complex than most people realise.

Financial knowledge is freedom

Buy, Borrow, Die is not a strategy that most people can apply in the same way as a billionaire. Yet understanding it is important because it reveals how the financial system truly works when wealth is built around assets rather than wages.

The most important lesson of this strategy is not that there is a way to pay less tax or preserve vast fortunes. The real lesson is that the rules governing money are often far more complex than we have been led to believe. While part of society learns how to use these rules to its advantage, most people are not even aware that they exist.

In this way, financial education should form part of every citizen’s general culture. Not to turn ourselves into billionaires or to replicate the strategies of large fortunes, but because understanding concepts such as debt, assets, taxation, inflation or money creation helps us better interpret the economic world around us and make more informed decisions about our future. Because, ultimately, economic freedom does not begin with wealth; rather, it begins with knowledge. And only when we understand the rules of the game can we aspire to make truly free decisions.

11Onze is Catalonia’s fintech community. Open an account by downloading the El Canut app for Android or iOS. Join the revolution.

Accelerating digitalisation has been one of the most important challenges for SMEs during the pandemic. The data say that 70% of companies in Spain have been digitalised during the pandemic, according to the consulting firm IPG. This means that 7 out of 10 have opened an online store.

While many SMEs have been thinking about digitalisation for years and it was one of the outstanding issues, the pandemic has accelerated and made many companies go online in record time and, probably thanks to this, they have not had to close. A company with less than 250 employees whose turnover does not exceed 5 million Euro is considered an SME.

The cost of digitalisation

When an SME searches the internet for a way to go digital, it will probably come up with many offers and very cheap prices from companies that are dedicated to this task. It can even buy a domain, which will cost less, as you can have one for €10 a year. It can also find many pages that provide with templates and, if it is accompanied by images, it can make a website on its own.

But, as the saying goes, you can’t teach an old dog new tricks.

There are many elements to consider when creating an e-commerce. It depends on the business you have, whether you have an extensive catalogue, whether you work internationally, or if you constantly have new products. The best thing to do when digitalising your business is to hire an agency to help you get this big project up and running. There are many things to keep in mind, and having a good e-commerce that works perfectly and that does not have errors will be the key to success.

Things to keep in mind

Before launching an online store, keep in mind:

- Make an analysis of the competition: surf the internet (visit websites and social networks).

- Make an analysis of the own company: identify your own e-commerce. Decide if it can be done by the company’s staff or if external help is needed, for example, an agency specialising in web pages.

- Take into account the stipulated time required to make a web page, as there may always be some surprise. Therefore, the launch date of the business must not be shared with the networks until it is 100% sure.

- Once the website is up and running, it needs to be constantly updated.

- You must be very fast: when a user asks about a product or service, you must answer as soon as possible because, otherwise, there is a risk that they may end up buying it elsewhere.

The pandemic has changed consumer habits, and it has also made it clear that if you want to keep the business going, you need to have an online site for potential customers to find and see what is offered.

We are in the age of omnichannelity, and you need to have the ability to satisfy both a customer who buys in the physical store and a customer who buys online, through a phone call, through an email, or even through the social media of the business.

The past

Years ago, it was unthinkable that a company could earn customers with a website. Until then, the usual technique for getting buyers was having a sales team that, along with a marketing strategy, did what is called “cold calling”, that is, selling the product or service from scratch. This commercial task, on many occasions, could last for weeks or months.

The present

Today, when you open a business, even if services are offered, you need to have a website where potential customers can see what is being offered, what has been done, the team that makes up the company, and an essential thing, its business philosophy (mission and vision). With just this information, the potential customer can get an idea of who they are.

Apparently, it may seem much easier to reach the customer through a website than doing it with a sales team, but it’s not quite that good. It’s not all about having a website. Social media is another tool that must be kept in mind in today’s society, which is permanently connected.

During the pandemic, companies have had to digitalise their businesses. This has been the only way to earn income. The data tells us that 7 out of 10 companies that did not have an e-commerce before the confinement had to go digital if they didn’t want to close the business. The food, fashion, electronics, beauty, and household products sectors are the ones that have benefited the most from having taken this step.

Do you want to be the first to receive the latest news about 11Onze? Click here to subscribe to our Telegram channel

When you ask for information to assess whether to make an investment, the first step is to sign a document certifying you as a qualified investor. This document does not compel you to make any investment, but it is a legal requirement for them to inform you.

It is highly recommended that you never make an investment without understanding it. We make investments with the intention of making a profit, but all investments involve risk. Sometimes the risk may be losing the capital, sometimes it may be not making a profit, and sometimes it may even put your assets at risk if you use them as collateral for the investment. In any case, before making an investment, it is essential to sign a document stating that we are aware of the risks and of our skills as investors.

11Onze Recommends Litigation Funding

In the case of 11Onze Recommends, the fact that the provider offering Litigation Funding is British means that it must comply with UK regulations. Therefore, before the provider can give you the full details of the product, what is known as a Self-Certified Sophisticated Investor document must be completed. Self-Certified Sophisticated Investor is the concept that the regulator responsible for supervising financial services in the UK, the Financial Conduct Authority (FCA), defines as an investor who meets certain criteria of knowledge and experience in financial matters.

In other words, it is the way in which the investor communicates to the investment firm or platform that they know what they are doing and are comfortable being informed of the risks involved in the investment. It is a requirement for investors in certain investment products or services offered from the UK, so that the business can be assured that its client understands the transaction.

What does self-certification require you to do?

Signing the document self-certifying you as an investor does not compel you to do anything. It only authorises the company to provide you with information about a sophisticated investment product. This allows clients to access certain types of investments that are not available to the general public, such as private company shares and other unlisted securities. Likewise, it helps protect less experienced investors from making potentially risky investments that they may not fully understand and to make better-informed decisions.

But filling it in does not mean you end up making the investment. In any investment, once you have the information you have to analyse it, ask all the questions you need to, understand the risks (if any) and decide if it is worth it. In the case of Litigation Funding, the provider is supervised by 11Onze to ensure quality and transparency in the management. Likewise, the 11Onze community can make any suggestions it deems appropriate. It was at the request of the community that 11Onze Recommends renegotiated the terms and conditions of Litigation Funding, simplifying them.

To invest or not to invest

All investments require investors, but not all investors are the same. Investing can be a complex decision, especially for beginners, so before making an investment it is important to know our investor profile and whether we have the basic knowledge to invest in a given product. We need to tailor investments to our possibilities and always understand what we are doing with our money. At a time of low yields on bank deposits and high inflation, it is necessary to learn how to invest safely so as not to lose purchasing power. At 11Onze we try to ensure that our community can do this with as little risk as possible, which is why 11Onze recommends 11Onze Litigation Funding to its community.

If you want to find out how to get returns on your savings with a social justice product, 11Onze recommends Litigation Funding.

While a minority concentrates an ever-growing share of global wealth, millions of people are finding it increasingly difficult to access housing, build savings, and achieve prosperity. Economic inequality is no longer an ideological issue. It is a measurable reality that is shaping the future of our societies.

For decades, Western economies have built their narrative around an apparently simple promise: if the economy grows, everyone benefits. This principle worked reasonably well throughout much of the 20th century. After the Second World War, Europe and the United States experienced an economic expansion that enabled the consolidation of the middle classes, widespread access to housing, and a sustained improvement in living standards.

However, data from the last forty years points to a different reality. Wealth continues to grow, but it is increasingly concentrated in fewer hands. At the same time, a significant portion of the population faces growing difficulties in accumulating wealth, maintaining purchasing power, or securing future prospects comparable to those enjoyed by previous generations. The great paradox of our time is that we are living through the most materially abundant period in history while perceptions of precariousness, insecurity, and impoverishment continue to rise.

An Increasingly Wealthy… and Unequal World.

The concentration of wealth is one of the most significant economic phenomena of the 21st century. According to the World Inequality Lab, the richest 10% of the Spanish population controls nearly 60% of the country’s total private wealth, while the poorest half of the population owns only a small fraction of total assets.

At a global level, the situation is similar. Data from the World Inequality Lab, the OECD, and the World Inequality Report show that the wealth of large fortunes has grown at a much faster pace than the real economy over recent decades. Financial crises, expansionary monetary policies, and rising asset values have ultimately benefited those who already possessed wealth.

We are not only talking about millionaires. The fundamental divide lies between those who own assets that appreciate over time—homes, stocks, businesses, or precious metals—and those who rely exclusively on their salaries to maintain their standard of living.This divide is creating a new social fault line that cuts across much of the developed world.

Catalonia: Less Statistical Inequality, but Greater Difficulty in Prospering.

Catalonia presents lower inequality indicators than the Spanish average. The Gini index is below the national level, and income distribution is relatively more balanced than in other territories. Yet income tells only part of the story.

The key issue is wealth. A family may earn a decent income and still find itself in a vulnerable situation if it cannot purchase a home, if it spends an excessive share of its income on rent, or if it is unable to generate savings. The latest data from Idescat indicate that nearly one quarter of the Catalan population is at risk of poverty or social exclusion. At the same time, access to housing has become one of the main economic concerns for citizens.

This reality explains an increasingly widespread perception: many people work, study, and produce more than ever, yet feel they have a harder time prospering than their parents did.

From a Wage-Based Society to a Wealth-Based Society.

To understand this transformation, we need to look back. For much of the 20th century, work was the primary mechanism for social advancement. Wages evolved relatively in line with productivity and allowed families to gradually build wealth.

This balance began to change in the 1980s. Financial liberalisation, economic globalisation, and market deregulation fostered an unprecedented expansion of capital markets. Meanwhile, wages grew at a much more moderate pace.

Economist Thomas Piketty (2013) “Le Capital au XXIe siècle“ a summarised this dynamic with an idea that has become an international reference: when the return on capital consistently exceeds the growth of wages and the productive economy, wealth tends to become increasingly concentrated (r > g). This is precisely what has happened over the last few decades.

Those who owned housing, shares or holdings have seen the value of their assets grow, but those who only had their wages have had to face accumulated inflation, considerable fiscal pressure and a continuous increase in essential goods. The consequence is that Western economies have progressively evolved into a heritage society, where asset ownership is increasingly determining rather than employability.

Housing: The Great Factory of Inequality.

If there is one element that exemplifies this transformation, it is housing.

For decades, buying a home was the main tool through which middle-class families accumulated wealth. Today, that possibility is slipping away for a growing share of the population.

Housing prices have risen much faster than wages, especially in major metropolitan areas. This forces many families to devote an ever-increasing proportion of their income to rent or mortgage payments. The result is an increasingly visible social divide between property owners and non-owners.

The former accumulate wealth thanks to the appreciation of real estate assets. The latter see a significant portion of their income devoted to financing that same wealth without ever becoming its owners.

When Inequality Stops Being Merely an Economic Problem.

Extreme inequality is not just a matter of social justice. It is also a matter of economic and democratic sustainability. The IMF and the OECD have repeatedly warned that excessive wealth concentration tends to reduce long-term growth, limit social mobility, and weaken institutional cohesion.

But there is another, even more worrying factor. When a significant share of the population perceives that working, studying, or making an effort no longer guarantees a real improvement in living conditions, trust in institutions deteriorates. Social frustration increases, giving rise to phenomena such as political polarisation, voter abstention, and the growth of populist movements.

History shows that societies with extreme inequalities tend to be less stable and more vulnerable to episodes of social tension.It is no coincidence that this debate has returned to the centre of the international economic agenda.

The Risk of a New Economic Feudalism.

Some economists and sociologists warn that Western economies may be moving towards a structure that resembles certain features of pre-industrial societies.

An increasingly small minority concentrates productive and real estate assets. An increasingly large majority depends exclusively on labour income to sustain its standard of living.

In this scenario, inheritance regains growing importance, social mobility declines, and economic opportunities tend to remain within the same family groups. The risk is not only economic. It is also democratic. When wealth becomes concentrated, so too does the capacity to influence political, regulatory, and media decisions.

There is no single or immediate solution. Governments can act through taxation, housing policies, business competition rules, and educational opportunities. However, these reforms require political consensus and time.

In the meantime, citizens face an immediate challenge: protecting the fruits of their labour.

In a world where inflation erodes the value of money, assets become more expensive, and wealth concentration continues to grow, traditional saving alone is no longer enough. It is essential to understand how markets work, how to diversify assets, how to manage financial risks, and how to preserve wealth over time. Financial education ceases to be a complementary skill and becomes an economic defence mechanism.

The great fracture of the 21st century is not only the one that separates rich and poor. It is also the one that separates those who understand how money works from those who are forced to constantly react to the economic decisions made by others. In a context marked by persistent inflation, global indebtedness, rising asset prices, and growing wealth concentration, financial knowledge is no longer optional—it has become a necessity.

Protecting savings with physical gold has been one of the main contributions of 11Onze to its community and, now, the range of products is expanded. Therefore, in the face of volatility, the still high inflation and the crisis of growing confidence in the banking system, gold is once again reinforced as a refuge value. Discover the Seed Gold at Preciosos 11Onze.

For years, stock buybacks by large companies, especially financial institutions, have been the norm. These operations can bring legitimate strategic benefits, but they can also be used to disguise accounting results and manipulate stock prices.

For most of the 20th century, share buybacks were considered illegal because they were believed to be a way of manipulating the stock market. It was in the 1980s that neoliberal policies allowed share buybacks to become one of the most popular financial engineering tools.

What is a stock buyback?

A share or stock buyback is a financial transaction whereby a company buys back its shares and redeems or disposes of them. The company’s overall financial position does not change, but by reducing the number of outstanding shares, each shareholder’s stake in the company increases.

Companies often argue that they do this in order to give value to shareholders, since this activity can increase the share price. In some cases, share buybacks can be used to prevent a shareholder or group of shareholders from acquiring sufficient shares to take control of the company.

Another advantage of share buybacks for shareholders is that, unlike dividend remuneration, as it is an indirect remuneration to shareholders this transaction has no tax implications unless they choose to sell the shares, in which case they would be taxed if they realised a capital gain. On the other hand, while the dividend is a distribution of past profits, when a share buyback materialises, it is in anticipation of future profits.

Potential market manipulation

The problem arises when these buybacks are carried out not to genuinely improve the financial situation of the company, but to make the shares look more attractive to short-term investors or to reward the managers of these companies who have bonuses linked to share performance.

This practice has become widespread and has overtaken dividend payouts, especially in the United States, where many corporations have prioritised short-term returns to management and shareholders overinvestment in the company’s future. One of the clearest examples of the negative consequences this business strategy can have is the crisis facing the Boeing company, where in a recent US Senate hearing its executives were accused of ‘strip-mining’ the company for profit.

Financial institutions have been one of the sectors that have made the most use of this practice, especially after the 2008 financial crisis and after many of these institutions were bailed out with public money. Stock buybacks have been financed by using accumulated profits or, in some cases, by increasing debt. Often, these operations are carried out at the expense of access to credit for businesses and consumers, improved services to customers, higher salaries for employees or through job cuts.

Critics also point out that stock buybacks distort market reality. Under the pretext of increasing shareholder returns or attracting new shareholders, buybacks can be used to disguise companies’ accounting results and artificially increase share prices, which should reflect their real economic situation. The need for strong regulation and transparency to prevent malpractice is obvious, yet the process of extracting value from capital seems likely to remain focused on short-term profit and to the detriment of productive investment.

Fund lawsuits against banks. Get justice and returns on your savings above inflation thanks to the compensation the banks will have to pay. All the information about Litigation Funding can be found at 11Onze Recommends.

A Golden Cross is an indicator within the technical analysis of trading that investors use to predict a potentially bullish reversal in a market. It occurs when the short-term moving average of an asset’s price rises above its long-term moving average, which has just occurred in the gold market.

It is essential to understand, identify and predict price movements to make the best investment decisions in stock markets. For this purpose, there are two contrasting analytical techniques, but they can be used complementary when deciding whether to buy or sell certain assets.

On the one hand, we have fundamental analysis, which attempts to calculate the real value of an asset by studying the primary variables of a company, such as the balance sheet of sales and profits or cash flow, which affect its current and future value, to find out whether it is a good or bad investment.

On the other hand, a technical analysis predicts when to buy or sell securities based on statistical indicators displayed on graphs, assuming that a thorough study of them will help us to forecast their future value. Specifically, it studies market movements, observing the price of the asset and stock market volume, using futures markets and stocks to determine upward or downward trends that complement fundamental analysis.

Moving averages, trend lines and crossovers

In charts used in technical analysis, a moving average is a technical indicator that combines prices of an asset over a set period and divides them by the number of data points collected to give a trend line. This trend line connects a variety of data points that reflect the highs or lows of prices over a given period.

Moving averages are intended to smooth out price fluctuations, thus helping us to see the trend of the security or index over time, beyond one-off or insignificant fluctuations. A moving average of prices can be calculated over the short (10 days), medium (50 or 100 days) or long term (150 or 200 days), and can be simple (all data are treated equally when calculating the average) or weighted (greater weight is given to more recent data).

A crossover occurs when the actual price line of an asset or index crosses the prediction line made by the moving average. In this case, it is considered that there is a change of trend, either bearish when it crosses it downwards or bullish when it crosses it upwards.

Golden Cross indicates an uptrend

When a short-term moving average crosses above a long-term moving average, it is called a Golden Cross, and is considered a clear indicator that the trend of the index is upward, therefore prices will continue to rise. It is in contrast to a Death Cross, a crossover below which indicates a long-term bear market.

Golden crosses have three key stages: first, there is a downtrend in the price of a stock that eventually bottoms out, followed by a crossing of the stock’s shorter moving average over its longer moving average, which triggers a change in trend. Finally, the stock continues its ascent towards higher prices.

This is what has taken place recently in the gold market. Although it has experienced a slight, one-off drop in value after making new all-time highs, the golden metal has formed a Golden Cross chart pattern, a sign that, some analysts say, more gains are coming and a prolonged upward cycle is beginning.

Protect yourself from economic crises with the ultimate safe-haven asset: gold. If you want your savings to keep or increase their value, Gold Patrimony.

The multiple bank failures that took place during the 2008 financial crisis familiarised us with the concept of a bailout, a mechanism whereby a government uses public money to rescue financial institutions. However, there is another, less well-known option where shareholders, creditors, and depositors can take over the losses.

Big banks have become used to playing Russian roulette with money that is not theirs. If business is good, they keep the profits, while if it goes badly, the losses are socialised at the taxpayer’s expense. This is a globalised phenomenon that has been repeated over time and became evident with the multiple bank bailouts and financial sector restructuring that took place during the 2008 financial crisis.

Thus, to avoid the collapse of the banking system, the first option for many countries was to bail out ailing institutions or, in other words, use taxpayer’s money to cover the red numbers caused by the irresponsible financial management of the bankrupt institutions’ management teams.

In the case of Spain, major international organisations estimate the costs of the bank bailout at 6% of GDP. More than 64 billion euros in public money was injected into the banks, much of which has already been written off after the banks have only returned a tiny amount to taxpayers.

External bailout vs. internal recapitalisation

The two basic models currently used by the financial system to help struggling banks are the bailout or external rescue and the bail-in or internal recapitalisation. While in a bailout the state, i.e. the public as a whole, bears the cost of recapitalisation, in the case of a bail-in the losses are borne by shareholders, creditors and ultimately depositors, as happened in Cyprus in 2013. The concept of bail-in is based on the notion that if the bank needs to rebalance its balance sheet, it must first use its own capital.

Since January 2016, a bail-in system has been in force in the European Union. According to this resolution mechanism, shareholders receive the first blow. If this does not stabilise the bank, subordinated creditors take over. Next in line are the holders of senior bonds and, finally, uninsured depositors, i.e. those with more than 100,000 euros in their accounts, with preference given to the deposits of large companies over those of households and SMEs, while small depositors remain unaffected.

It is therefore a mechanism designed to minimise the possibility that the costs of resolving a non-viable institution will be borne by taxpayers, while at the same time ensuring that systemically important institutions are resolved without endangering financial stability.

Can the bank or the State take my savings in case of bail-in or bankruptcy?

Yes, if you have more than €100,000. If you have less than €100,000, you will be excluded from the bail-in and will be covered by the Deposit Guarantee Fund in case of bankruptcy. This body guarantees the return of money from savings accounts, current accounts and fixed-term deposits.

Let us remember that the FGD guarantees 100,000 euros per depositor and institution. Therefore, to insure higher amounts, it is advisable to have the capital distributed among different entities, without exceeding 100,000 euros in any one of them. Alternatively, if an account with 200,000 euros is shared by two people, each of them would have 100,000 euros insured.

Another option is to open a current account with a fintech such as 11Onze, which operates through an Electronic Money Institution (EMI) and is required by law to insure 100% of its customers’ deposits in the event of bankruptcy, regardless of the amount.

Are there any real examples of bail-in?

In Spain, on 7 June 2017, Banco Popular was the first Spanish bank to be bailed-in under the European Union’s new framework for bank resolution. Shareholders and subordinated debt holders lost their investment, and the bank was sold for one euro to Banco Santander, thus avoiding the use of public money. In this case, depositors, even if they had more than 100,000 euros in savings, did not lose their money.

The bank bailout in Greece in 2012 led to the liquidation of Laiki Bank and the restructuring of the Bank of Cyprus through a bail-in. In this case, customers with up to €100,000 in savings did not lose their money, but big depositors lost a large part of their savings or, in some cases, this money was converted into shares.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

The American multinational investment company has consolidated its position as the largest shareholder of Banco Sabadell, Banco Santander and BBVA, while increasing or maintaining its position as one of the main investors in CaixaBank, Bankinter and Unicaja.

New York-based BlackRock is the world’s largest asset manager. With more than $9 trillion in assets under its management, 70 offices in 30 countries and clients in more than 100, its influence extends far beyond Wall Street, managing investments for clients ranging from individual investors to large corporations and governments.

The list of corporations with assets under its stewardship is almost endless: from technology companies such as Apple, Meta and Microsoft, to oil companies such as ExxonMobil, Chevron and Shell, to banks such as Goldman Sachs, JPMorgan and Bank of America. In fact, it would be easier to list ‘the few’ large global companies that are not part of BlackRock’s stock market portfolio.

In Spain, the presence of the US investment giant is well established. BlackRock is the main shareholder of the Ibex-35, doubling its workforce in the last five years and controlling 42,000 million euros in investment assets. Iberdrola, Red Eléctrica, Repsol, Enagás, Telefónica… and, according to data from the Comisión Nacional del Mercado de Valores (CNMV), also lord and master of Spanish banking.

Over 25% of the shareholding with an investment of more than 6,000 million euros

BlackRock’s presence in Spanish banking shareholdings has increased progressively over the last few years, consolidating its position as the main reference shareholder in the Spanish banking sector.

In the case of BBVA, Banco Santander and Banco Sabadell, BlackRock is their largest shareholder with 7.4%, 6.2% and 4.46% respectively. On the other hand, it is now the third-largest shareholder of CaixaBank, the fifth of Bankinter, and maintains a small stake in Unicaja.

An upward trend implies a greater influence in the management and direction of these banks, but it is not free of controversy due to the possible conflict of interest it could entail. As Gerald Davis warned, BlackRock is a silent giant, but an incredibly powerful one.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

If you are an investor, you must understand what stock indices are and what they are used for. A stock index is a statistical indicator that reflects the change in the price of the main shares listed on a given stock exchange and can be used as an investment tool.

Stock indices are benchmark instruments characteristic of the world of finance and essential for investors. They are tools that measure the performance of a specific group of assets in the stock market, providing a clear view of the price of a set of related stocks or securities.

There are multiple indices around the world which, as Joan Benedicto, 11Onze agent, points out, ‘will tell us whether shares in a particular economic sector are rising or falling in price and how they will perform as a whole’. Therefore, they can be key when it comes to knowing the stock market and making investments.

The agent Joan Benedicto explains what stock market indices are.

What are the main stock market indices?

Stock market indices can include from a few to hundreds of companies. The best-known international examples are:

- The Dow Jones Industrial Average (DJIA), created by Charles Henry Dow, editor of The Wall Street Journal, measures the share prices of the 30 largest companies listed on the New York Stock Exchange.

- S&P 500, which includes the 500 largest companies in the United States and is considered the most representative of the real market situation.

- NASDAQ, which includes the largest market capitalisation technology companies and other companies in high-growth sectors.

- FTSE 100, pronounced ‘Footsie one hundred’, is a stock market index published by the Financial Times and comprises the top 100 stocks on the London Stock Exchange.

- NIKKEI 225, the main indicator of the Tokyo Stock Exchange that measures the results of the 225 Japanese public companies with the highest capitalisation and liquidity belonging to various industrial sectors.

- In the case of Spain, we find the IBEX 35. Therefore, when you hear that, for example, the Spanish stock market has fallen by 0.10%, it means that the market values of the thirty-five companies in the main stock market index of the Spanish market have fallen by 0.10%.

These indices work by points, which will increase or decrease depending on the evolution of the value of the companies that make up the index, but as Benedicto explains, ‘we have to bear in mind that not all the companies that make up these indices are taken into account equally, while some may influence the index by 10%, others may only influence it by 0.5%’.

If you want to discover the best option to protect your savings, go to Preciosos 11Onze. We will help you buy at the best price the ultimate safe haven asset: physical gold.