Record central bank purchases of gold

Gold demand reached record highs over the past year and shows no sign of abating in 2023. Central bank purchases of gold are off to the best start to a year in more than a decade.

Concerns about contagion from the banking crisis in the United States, financial market volatility and geopolitical uncertainty have further heightened interest in gold, which is considered a safe-haven asset against any economic uncertainty. The upward trend is reflected by consumers, private investors, governments and central banks.

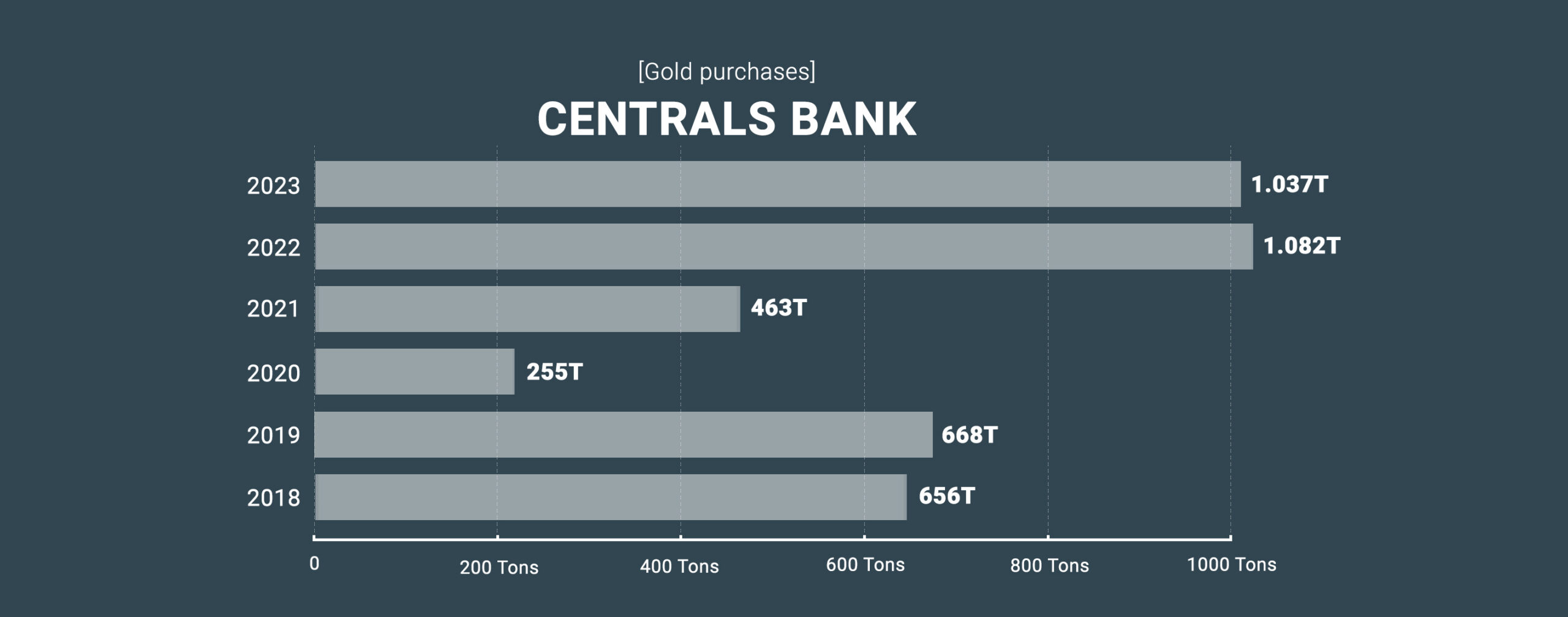

According to the latest data published by the World Gold Council (WGC), on a year-on-year basis, central banks have recorded net purchases of 125 tonnes of gold at the end of February this year. This is a figure not seen since at least 2010 and continues the upward trend experienced during 2022, ending the year with a record 1,136 tonnes of gold sold.

Therefore, this confirms that the gold market continues to receive support from the central banks of countries that want to diversify their reserves to shield their economies, which leads us to expect that the price of gold will continue to rise significantly throughout this year. The price of gold has risen by 9.2% in the first quarter of the year, a revaluation that is in line with Bank of America’s forecast of a 10% increase in the price of gold by 2023.

The big gold buyers

The increase in gold purchases has been driven largely by the relentless demand from China’s central bank and the Turkish central bank, with 25 and 22 tonnes added respectively in February, for a cumulative total of 2,050 and 587 tonnes representing 3.7% and 33% of their international reserves.

On the other hand, despite the ban on selling Russian gold in Western markets, the Central Bank of Russia continues to increase its gold reserves at a good pace. Although no specific data on its purchase schedule is available, it has disclosed that at the end of February 2023 it had 2,330 tonnes of gold reserves, 31 tonnes more than at the end of January 2022, representing 24% of Russia’s international reserves.

Gold purchases by central banks of countries such as Uzbekistan (8 tonnes), Singapore (7 tonnes) or India (3 tonnes) were added to the February net purchases figure. Kazakhstan’s central bank was the exception, reducing its gold reserves by 13 tonnes to a total of 342 tonnes. A deviation from the trend followed by the other banks need not be significant, given that central banks purchasing gold from local sources are often frequent sellers of gold.

Whether gold is accumulating as a reserve asset in the face of escalating hostilities in the US-China trade war, sanctions against Russia or instability in the Western banking sector, the sharp increase in buying has not gone unnoticed by geopolitical analysts. Could this accumulation of gold be a sign of a change in the international monetary system? Of a return to the gold standard? Of a new global crisis? Whatever the case, it is clear to central bankers that when things go wrong, nothing is as safe as gold.

Protecting savings with physical gold has been one of 11Onze’s main contributions to its community, and now the range of products is expanding. This is why, in the face of volatility, still high inflation and the growing crisis of confidence in the banking system, gold is once again strengthening its position as a safe-haven asset. Discover Gold Seed at Preciosos 11Onze.

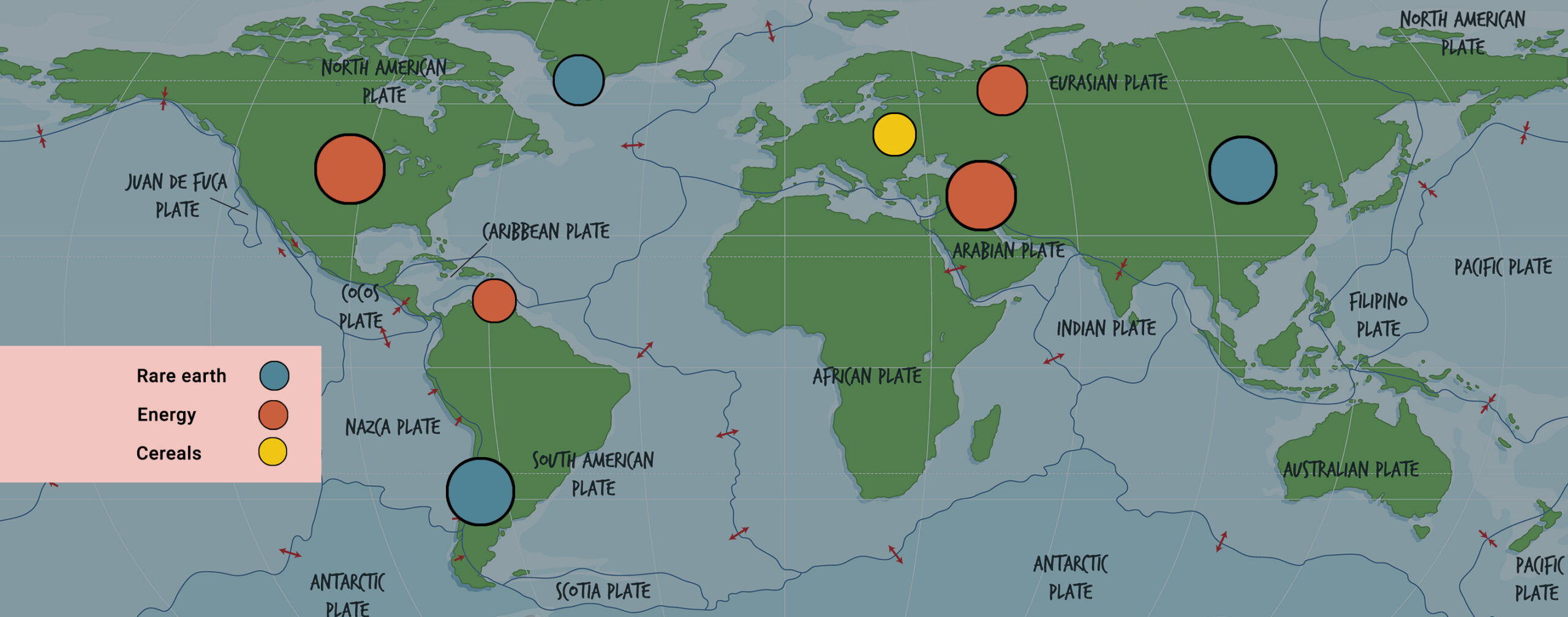

Modern wars are rarely explained solely by territorial or ideological disputes. If we look at the map of current conflicts with perspective —Ukraine, the Middle East, Venezuela, or even the growing interest in the Arctic— a recurring pattern emerges: energy, natural resources, and monetary power.

In a global economic system dominated by the dollar and hydrocarbon trade, control of oil and gas remains decisive. But in recent years, a new factor has been added: competition for tangible resources, such as gold, strategic minerals, or even food. In this context, geopolitics and economics once again move hand in hand.

The key resources that define current global conflicts.

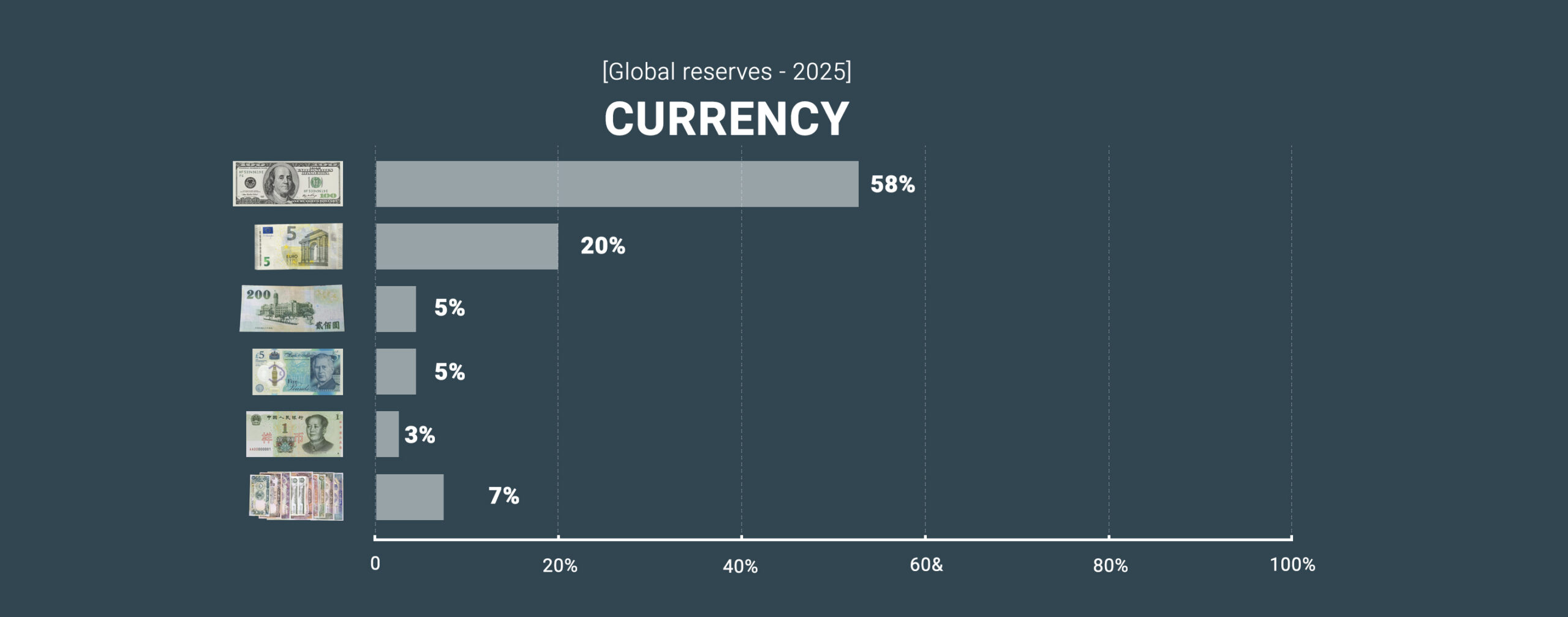

After World War II, the Bretton Woods agreements placed the dollar at the center of the international monetary system. Initially, the U.S. currency was linked to gold, but this system broke down in 1971 when the United States suspended the convertibility of the dollar into precious metal. From that moment on, the global monetary system was reorganized around another fundamental element: oil.

With the emergence of the petrodollar system, international hydrocarbon trade began to be predominantly denominated in dollars. This meant that any country wishing to buy oil had to hold reserves in this currency.

This mechanism generated a structural demand for dollars across the planet and consolidated the financial hegemony of the United States. The system allowed Washington to finance large deficits and public debt, while the world continued to use its currency to buy energy. In this sense, energy became one of the invisible pillars of global monetary power.

Source. International Energy Agency

De-dollarization: an emerging threat

For decades, this system functioned with relative stability, but in recent years movements have emerged that challenge this financial architecture. Countries such as China, Russia, and India have begun to promote bilateral trade agreements that reduce dependence on the dollar. This process, known as de-dollarization, seeks to create a more multipolar economic system.

Economic sanctions driven by the United States have also accelerated this trend. When a country can be expelled from the international financial system or blocked from the SWIFT system, many governments begin to look for alternatives to protect their economic sovereignty.

In this context, control of energy becomes even more relevant. If oil or gas were to be traded massively in other currencies, the dominant role of the dollar could be eroded.

Source. FMI – Currency Composition of Official Foreign Exchange Reserves

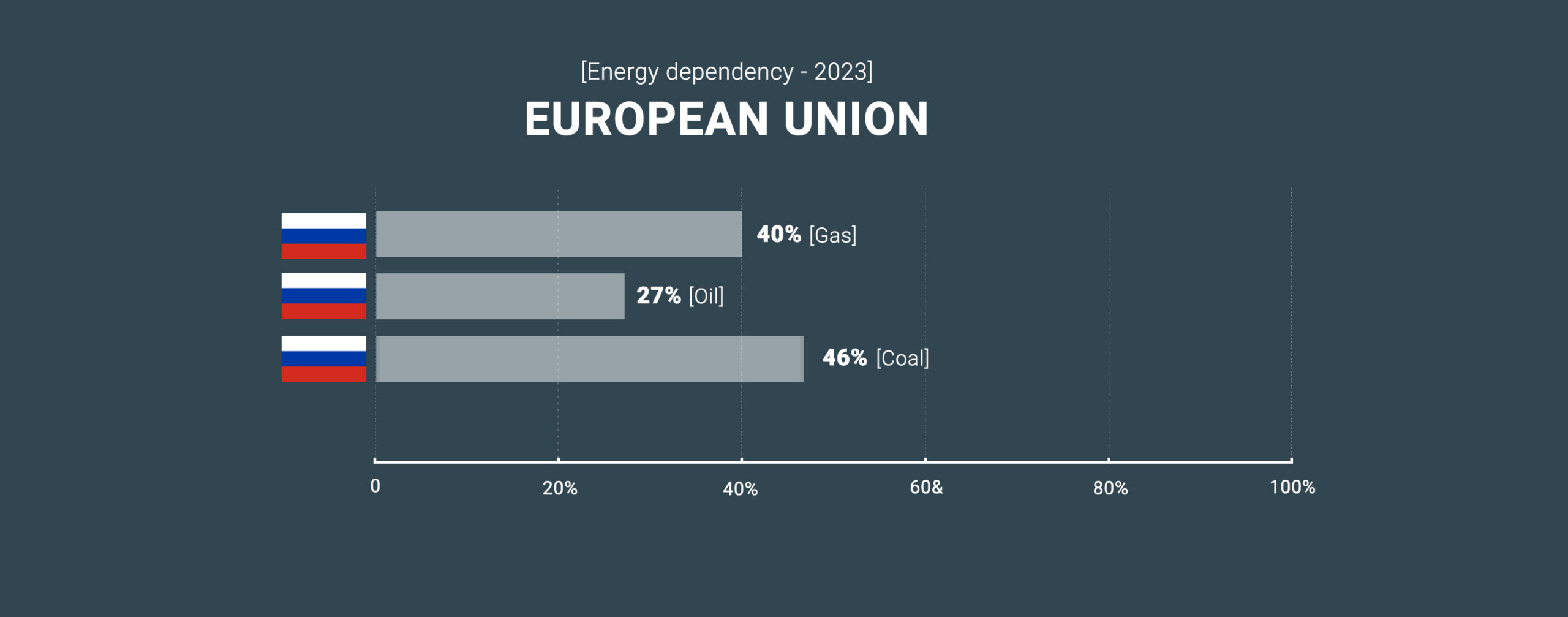

Ukraine: energy and geopolitics in Europe

The war in Ukraine has shown to what extent energy remains a central element of international politics.

Before the conflict, Europe depended heavily on Russian gas to fuel its industry and ensure energy supply. The Russian invasion and Western sanctions broke this balance and triggered a profound reconfiguration of global energy flows.

Europe has attempted to replace Russian gas with liquefied natural gas from the United States, Qatar, and other producers. This shift has had significant economic consequences, with a notable increase in energy costs for European industry.

The war in Ukraine is therefore much more than a territorial conflict: it is also a key episode in the reorganization of the global energy map.

Source. Eurostat / European Comission (Energy statistics, 2023)

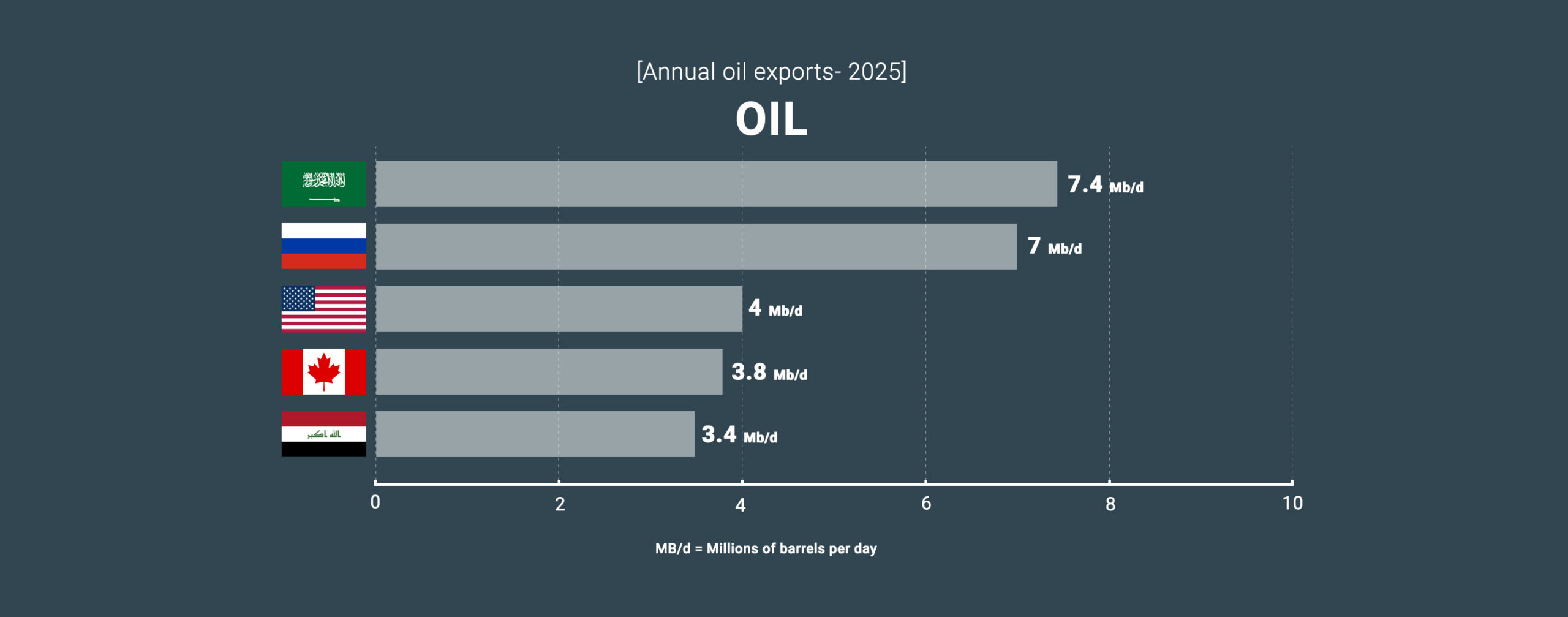

Middle East: the energy center of the planet

The Middle East remains one of the most sensitive regions in the world for an obvious reason: it concentrates a very significant share of global oil and gas reserves, making it a global energy epicenter and a key territory for international economic balances.

Any military escalation in the region —whether between Israel and Palestine, involving Iran, or in Lebanon— has an immediate impact on global energy markets, driving prices up and generating uncertainty in economies dependent on hydrocarbons.

In this context, beyond the media narrative focused on the political and humanitarian conflict in Gaza, a structural factor often overlooked emerges: the significant natural gas deposits discovered off the coast of Gaza. This energy reserve, known for decades, could alter the region’s energy balance and reduce external dependencies. Control over these resources is not only an economic issue but also a key element in the geopolitical struggle for energy dominance in the Eastern Mediterranean. Thus, the conflict acquires a strategic dimension that goes far beyond borders and national identities.

Moreover, strategic chokepoints such as the Strait of Hormuz or the Suez Canal are essential for transporting oil and gas to Europe and Asia, establishing themselves as true bottlenecks of global energy trade. Control over these trade routes is therefore a central element of international geopolitics and a constant source of tension between powers.

Venezuela: oil, sanctions, and power

Another clear example is Venezuela, the country with the largest oil reserves in the world, with nearly 300 billion certified barrels. This energy abundance, far from guaranteeing stability, has turned the country into a central actor on the global geopolitical stage, often subject to external pressures and highly dependent on its own extractive model.

Over recent decades, the South American country has been subject to economic sanctions and geopolitical tensions that have deeply affected its oil industry, limiting investment, deteriorating infrastructure, and reducing production. Control over Venezuelan energy production and access to its resources remain decisive factors in relations between Caracas, Washington, and other international actors, highlighting the extent to which energy is a tool of global power.

The return of tangible assets

However, current geopolitics no longer revolves exclusively around oil. For decades, the global economy has operated on a financial architecture based on debt, financial markets, and trust in fiat currencies —a system sustained more by expectations than by real value. But in recent years, a gradual shift has begun to question this model.

This shift points toward the recovery of the value of tangible assets —that is, physical resources with intrinsic value that do not depend solely on market confidence. We are talking about energy, precious metals, strategic minerals, or food: essential elements for the functioning of the real economy and increasingly decisive in a context of geopolitical tensions and resource scarcity.

Among these assets, gold stands out. For millennia, it has been a universal store of value and continues to play a key role in the global monetary system. Despite the end of the gold standard, central banks continue to accumulate this metal as a strategic asset to strengthen their reserves, especially in emerging countries seeking to reduce their dependence on the dollar and gain financial sovereignty in an increasingly uncertain world.

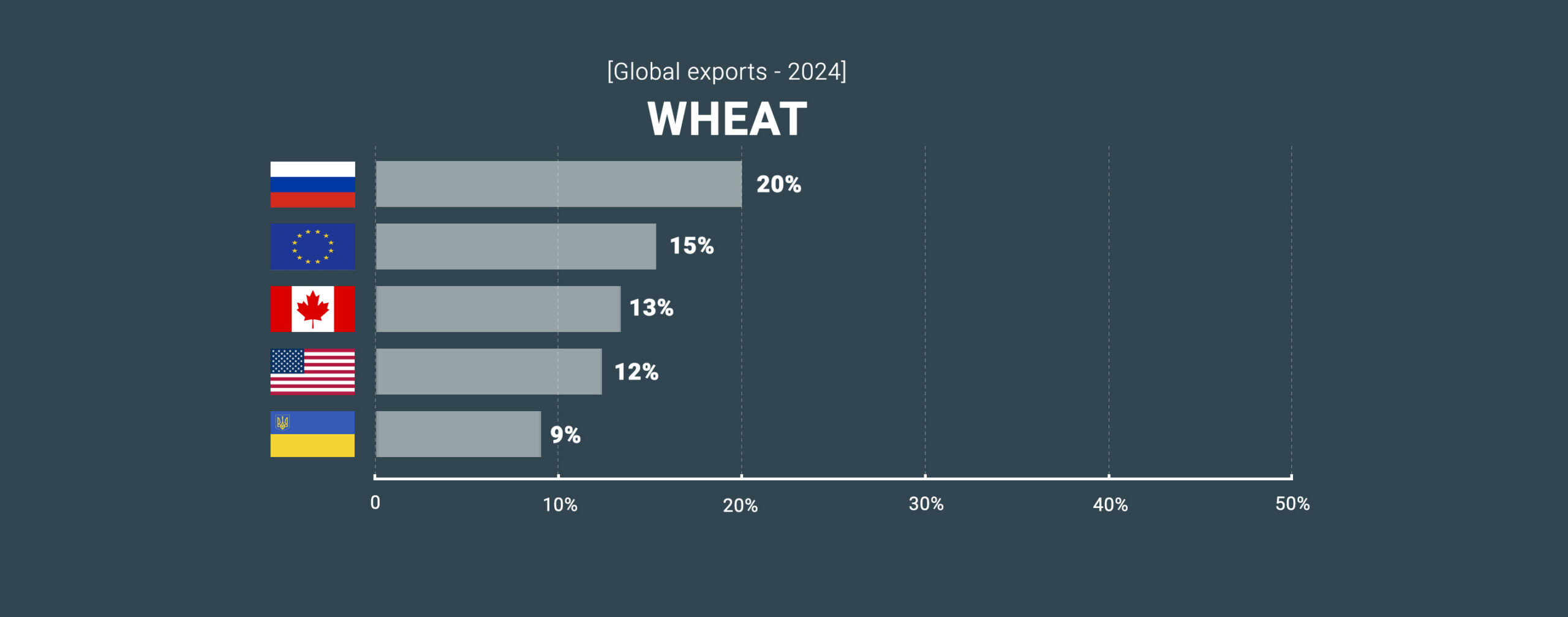

But gold is not the only critical resource. The war in Ukraine highlighted the extent to which food and fertilizers are key elements for global stability, becoming a new geopolitical weapon. Russia and Ukraine, major grain exporters, saw how the conflict disrupted supply chains and strained international food markets, causing price increases and putting the food security of many countries dependent on these imports at risk.

Greenland and the Arctic: the future of resources

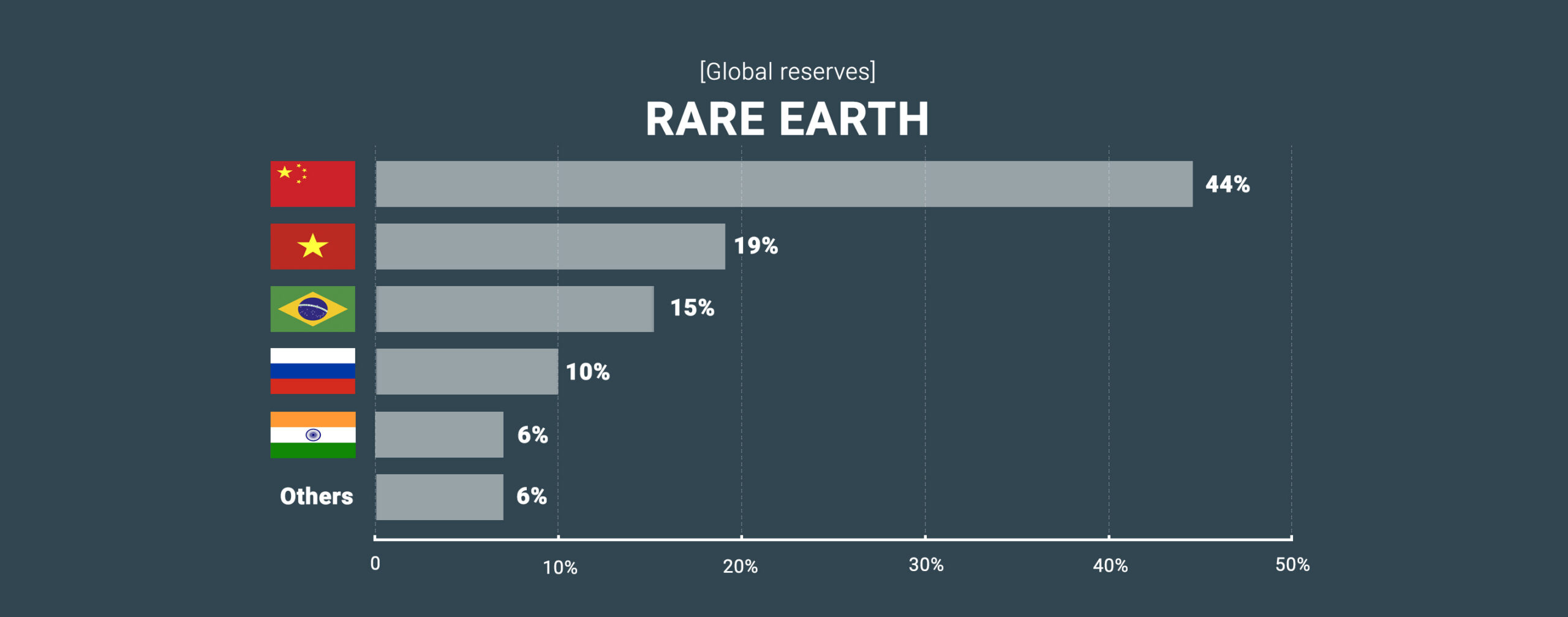

In this new geopolitical scenario, territories that until recently seemed peripheral have gained increasing importance. Greenland and the Arctic concentrate potential reserves of oil, gas, and strategic minerals, including rare earth elements essential for the technological industry and the energy transition, placing them at the center of new global power dynamics.

Moreover, the progressive melting of the Arctic is opening new trade routes that could profoundly transform global maritime trade, shortening distances between continents and altering traditional logistical flows. It is no coincidence that powers such as the United States, Russia, and China have intensified their interest in this region, aware that control over resources and new routes will be key in the economy of the future.

Source. US Geological Survey

A world returning to real resources

The geopolitics of the 21st century seems to be moving toward a model in which physical resources once again take center stage. Energy, metals, strategic minerals, and food are becoming fundamental pillars of the economic security of states, in a context marked by uncertainty and growing global competition. Increasingly, power is no longer measured solely in terms of financial capital or currencies, but in the ability to control the resources that sustain the real economy.

In this scenario, many analysts point to a paradigm shift: the transition from an economy dominated by financial capital to one more closely linked to tangible assets. Modern wars rarely have a single cause, but if we overlay the map of current conflicts with that of the planet’s energy and mineral resources, the coincidences are too evident to be accidental. Energy, the dollar, and natural resources are part of the same equation of power that defines international relations.

Understanding this relationship is key to interpreting current geopolitics and anticipating the movements of states in an increasingly tense world. In a context of geopolitical tensions, persistent inflation, and transformation of the international monetary system, understanding the role of strategic resources is more important than ever.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

L’arribada de l’euro digital significarà la desaparició dels diners en efectiu? Serà una eina de major control sobre els ciutadans? Quins són els arguments del Banc Central Europeu per estimular la seva implantació? Des d’11Onze, t’oferim la resposta a onze preguntes fonamentals sobre l’euro digital.

Christine Lagarde, presidenta del Banc Central Europeu (BCE), justificava recentment la necessitat d’un euro digital per la “transformació potencialment disruptiva” que està experimentant el model de pagaments a causa de l’augment de les transaccions digitals, l’aparició de nous actius digitals i l’entrada de gegants tecnològics com Google o Amazon en el mercat dels pagaments.

L’auge dels pagaments digitals queda patent en un estudi del BCE, que indica que l’any 2022 el valor dels pagaments amb targeta (46%) ja va superar al dels pagaments en efectiu (42%). I això sense comptar altres formes de pagament com les aplicacions mòbils. Davant aquesta realitat, Lagarde advertia que els diners tal com els coneixíem podrien perdre el seu paper d’àncora monetària, “amenaçant la seva funció clau per garantir la confiança en els pagaments”.

Sense aquesta “àncora pública”, l’aparició de nous tipus d’actius digitals, com les criptodivises, podria generar “inestabilitat i confusió entre els ciutadans sobre el que són diners i el que no ho són”, segons la presidenta del BCE, qui advertia sobre la volatilitat dels criptoactius i la necessitat de desenvolupar la regulació.

A més, Lagarde indicava que l’entrada dels gegants tecnològics en el mercat de pagaments “podria incrementar el risc de domini del mercat i la dependència de tecnologies de pagament estrangeres”, argumentant que “en l’actualitat més de dos terços de les operacions de pagament amb targeta a Europa són gestionades per empreses amb seu fora de la Unió Europea”.

En aquest context, està previst que al llarg d’aquest semestre la Comissió Europea faci una proposta sobre el marc legal de l’euro digital. Encara són moltes les incògnites sobre la futura moneda, encara que el Banc Central Europeu ja ha esbossat quins haurien de ser les grans línies mestres de la seva implantació. De totes maneres, no podem oblidar que el seu èxit o fracàs dependrà en última instància del grau d’adopció que assoleixi entre els ciutadans de la zona euro.

Substituirà l’euro digital als diners en efectiu?

No. El BCE ho ha deixat clar: l’euro digital seria un complement dels diners en efectiu, no un substitut, així que els bitllets i monedes seguiran en circulació. La idea és que l’euro digital funcioni en paral·lel a l’efectiu per donar resposta a la creixent demanda dels consumidors per fer pagaments digitals de manera ràpida i segura. Però la seva funció va més enllà. Segons la presidenta del BCE, l’euro digital “garantirà que els diners continuïn denominant-se en euros” i permetrà reforçar “l’autonomia d’Europa”.

Quin serà el seu calendari d’introducció?

El juliol de 2021 es va iniciar una fase de recerca del projecte que hauria de culminar l’octubre de 2023. En paral·lel, la Comissió Europea haurà d’elaborar una proposta de marc legal per a l’euro digital en els pròxims mesos. A la fi d’enguany, el BCE hauria de decidir si es passa a la següent fase, centrada en el desenvolupament de serveis integrats. En aquesta fase, que podria durar entre un i tres anys, es farien proves i possibles experiments reals amb l’euro digital. Amb aquests condicionants, els experts estimen que l’euro digital podria estar operatiu a partir de 2025 o 2026.

Es considerarà una moneda de curs legal?

Tot indica que sí. La presidenta del BCE ha dit que “seria inèdit emetre diners del banc central per als pagaments al detall sense estatus de moneda de curs legal només perquè circula electrònicament”. I afegia que “l’euro digital només pot funcionar com una àncora monetària si es converteix en un mitjà d’intercanvi digital convenient que formi part de la vida quotidiana dels europeus”. En aquest sentit, Lagarde apuntava que, per assolir els suficients efectes de xarxa, l’ús de l’euro digital hauria d’estendre’s no sols al comerç electrònic i els pagaments ‘peer to peer’, sinó també als pagaments digitals efectuats en botigues físiques, que en 2019 van suposar 40.000 milions de transaccions.

Existirà paritat entre els euros digitals i els físics?

Sí. En paraules de Christine Lagarde, l’euro digital “salvaguardarà la confiança dels ciutadans en què un euro és un euro, permetent-los convertir els diners privats en diners digitals del banc central en paritat”.

Quin nivell de privacitat oferirà?

Tot i que el 43% dels europeus va qualificar la privacitat com l’aspecte més rellevant de l’euro digital, la presidenta del BCE ha reconegut que “l’anonimat total que ofereix l’efectiu no sembla una opció viable” per a l’euro digital. No obstant això, el regulador bancari europeu indica que l’euro digital permetria efectuar pagaments sense compartir dades amb tercers, tret que sigui necessari per prevenir activitats il·lícites. I adverteix que, per tal que els pagaments continuïn sent una qüestió privada, caldria protegir diferents tipus de dades, inclosos la identitat de l’usuari, les dades de cada pagament (per exemple, el seu import) i metadades de l’operació com l’adreça IP del dispositiu utilitzat. En aquest sentit, és probable que existeixin diferents graus de privacitat en funció dels pagaments i que els usuaris hagin d’identificar-se la primera vegada que accedeixin als serveis de l’euro digital. Lagarde especificava que “almenys s’hauria de proporcionar un nivell de privacitat igual al de les solucions de pagament electrònic actuals” i assenyalava que s’està explorant si l’euro digital “podria replicar algunes característiques de l’efectiu i permetre una major privacitat en els pagaments de baix valor i baix risc, fins i tot en els pagaments offline”.

Serà una moneda alternativa dins de l’Eurosistema?

No. L’euro digital només seria una forma més de pagar en euros i seria convertible en paritat amb els bitllets físics. El BCE insisteix que l’objectiu és respondre a la creixent preferència dels ciutadans i les empreses pels pagaments digitals.

Quins avantatges tindrà respecte a les ‘stablecoins’ i els criptoactius?

L’euro digital estarà recolzat pel BCE, que recorda que una de les tasques encomanades als bancs centrals és la de “mantenir el valor dels diners, amb independència de la seva forma física o digital”. Si bé l’elevada inflació dels últims temps qüestiona la seva eficiència per complir aquest mandat, és evident que el suport del BCE garantirà una major estabilitat que l’exhibida per les ‘stablecoins’ i els criptoactius, que són molt volàtils. L’organisme europeu adverteix que “l’estabilitat i fiabilitat de les ‘stablecoins’ depenen de l’entitat que les emet i de la credibilitat i aplicabilitat del seu compromís de mantenir el seu valor al llarg del temps”. I afegeix que, quan no existeix una entitat reconeguda responsable d’un criptoactiu, els consumidors no poden reclamar els seus drets. A més, el BCE adverteix del risc que els emissors privats utilitzin les dades personals amb finalitats comercials.

Quins incentius tindran els consumidors per emprar l’euro digital?

El BCE assegura que l’euro digital serà un mitjà de pagament digital tan segur, fàcil de fer-se servir i barat com ho és l’efectiu actualment. La idea és que no tingui costos per a les persones que l’usin en els pagaments ordinaris i que pugui usar-se en qualsevol lloc de la zona euro. En un món en el qual els pagaments electrònics són cada vegada més freqüents, l’euro digital oferiria a individus i empreses una opció addicional per pagar fent servir diners del banc central. A més, l’euro digital podria oferir característiques avançades, com a funcions de pagament automatitzades o alguna forma d’identitat digital.

Hi haurà límits en la conversió d’euros físics a euros digitals?

Probablement. S’estan avaluant opcions que impedeixin mantenir imports elevats d’euros digitals com a inversió lliure de risc.

Hi haurà diferents nivells de remuneració?

També és molt possible. Segons el BCE, si la tinença d’euros digitals es remunerés, la remuneració del tram corresponent a pagaments al detall ordinaris (és a dir, de “nivell un”) seria zero o positiva i, per tant, mai inferior a la de l’efectiu. El regulador bancari europeu considera que la remuneració del “nivell dos” hauria de ser una mica inferior a la dels actius considerats segurs. L’objectiu seria evitar que l’euro digital es converteixi en una forma d’inversió.

Es basarà en la tecnologia ‘blockchain’?

Encara no s’ha decidit. L’Eurosistema es planteja diferents enfocaments i tecnologies per crear l’euro digital. Això inclou solucions centralitzades i descentralitzades, com ‘blockchain’, però encara no s’ha adoptat cap decisió sobre aquest tema.

En un món marcat per la revolució dels mitjans de pagament i l’auge dels criptoactius, que estan erosionant el paper dels bancs centrals i les monedes fiduciàries, el BCE vol que l’euro digital es converteixi en “la millor manera de gestionar la transició a l’era digital”.

11Onze és la fintech comunitària de Catalunya. Obre un compte descarregant l’app El Canut per Android o iOS. Uneix-te a la revolució!

Plogui, nevi o faci sol, el subministrament de l’aigua que consumeixen més del 80% dels catalans segueix en mans d’empreses totalment o parcialment privades. Malgrat els esforços per recuperar la gestió pública d’aquest servei, les multinacionals del sector es resisteixen a perdre un negoci milionari.

A través de l’empresa pública ONAIGUA, el consell comarcal d’Osona va assumir l’abril de l’any passat la gestió del subministrament d’aigua en aquesta comarca, pel que dona servei a 11.400 punts de consum i arriba a més de 25.000 habitants. Es va convertir en el primer consell comarcal a prendre una mesura d’aquest calat.

Podríem dir que es tracta d’una anomalia del mercat, ja que el subministrament de l’aigua a Catalunya està majoritàriament en mans privades. Un reduït nombre d’empreses privades administren i es lucren d’aquest bé preuat al nostre país gràcies a concessions moltes vegades qüestionades. I això que en el món la gestió pública assorteix al 90% de la població i Nacions Unides reconeix l’aigua com un dret humà.

Segons les dades de la plataforma Aigua és vida, més del 80% dels catalans obtenen l’aigua a través d’un servei totalment o parcialment privatitzat, mentre que el que el servei públic no arriba ni al 20% de la població. Aquest desequilibri s’explica pel domini del model privat en els municipis amb un major volum de població, que són els més rendibles.

Pressió per a municipalitzar un servei bàsic

Davant aquesta realitat, existeix una creixent pressió per recuperar la gestió pública d’aquest servei. L’Associació de Municipis i Entitats per l’Aigua Pública (AMAP) ja compta amb 68 membres i representa al 47% de la població de Catalunya. Recentment, publicava un informe amb propostes de reformes legislatives per canviar aquesta situació.

Sis municipis, l’Associació de micropobles de Catalunya i una nova empresa pública es van sumar a aquesta entitat l’any 2022. Dels nous municipis, només Mieres (la Garrotxa), Collbató (Baix Llobregat) i Torroella de Montgrí (Baix Empordà) gestionen directament l’aigua. Castelló d’Empúries està en procés de municipalitzar el servei, mentre que Manlleu i Sitges encara estan lligades a concessions per més d’una dècada amb Sorea i Agbar. Quant a l’Associació de micropobles de Catalunya, cal tenir en compte que el 70% dels municipis de menys de mil habitants, que són els menys rendibles, ja gestionen directament el subministrament d’aigua.

Gairebé un monopoli

Tot i que les empreses privades que gestionen l’aigua a Catalunya es presenten amb diferents noms segons el municipi, la majoria pertanyen al grup Agbar, que està valorat en uns 3.000 milions d’euros.

Aquest grup controla totalment l’empresa Sorea i posseeix gairebé el 80% de la Companyia d’Aigües de Sabadell (CASSA), el 68% d’Aigües de Rigat (Igualada) i el 49% de l’Empresa Municipal Aigües de Tarragona (Ematsa). A més, té al voltant del 35% de Mina Pública de Terrassa i el 31% de Girona SA.

Els seus beneficis no sols provenen de la venda d’aigua, que l’any passat pretenia encarir un 7,4% a Barcelona. També de la subcontractació de serveis a les seves filials. Això permet que a la Ciutat Comtal, per exemple, el cost dels comptadors d’aigua per a l’usuari final acabi més que triplicant el cost original. Això suposa uns 17 milions d’euros de benefici addicional a l’any.

Estratègia de judicialització

Davant un negoci d’aquesta grandària no resulta estrany que Agbar porti als tribunals qualsevol iniciativa encaminada a recuperar la gestió pública del subministrament d’aigua, com detalla el portal ctxt. Només a Barcelona, aquesta multinacional i les seves entitats afins han presentat una quarantena d’accions judicials.

La seva estratègia d’empantanar judicialment aquests processos per dilatar-los o diluir-los ha fet que fins i tot posés un contenciós contra un simple conveni entre l’Ajuntament de Barcelona i l’Àrea Metropolitana per a l’intercanvi d’informació entre institucions.

Un dels casos més sonats té a veure amb la consulta que l’Ajuntament de Barcelona volia impulsar per conèixer l’opinió de la ciutadania sobre una eventual gestió pública de l’aigua. Diverses entitats, entre les quals es troba Agbar, van interposar recursos. Finalment, el Tribunal Superior de Justícia de Catalunya (TSJC) va suspendre el reglament de participació ciutadana en la part relativa a les consultes i va impedir que la iniciativa tirés endavant.

El cas que afecta un major nombre de municipis és el que Agbar va impulsar contra diversos consistoris de l’Àrea Metropolitana de Barcelona. Inicialment, una sentència del TSJC en 2016 va anul·lar la concessió a Aigües de Barcelona del subministrament d’aigua en diversos municipis del cinturó metropolità, amb la qual l’empresa s’assegurava el servei a gairebé tres milions d’habitants durant 35 anys i uns ingressos de 3.500 milions d’euros. El tribunal veia “motius d’anul·lació per vicis en el procés de contractació” quan es va constituir l’empresa mixta en la qual participava Agbar. Tot i això, el Tribunal Suprem va revocar aquesta sentència l’any 2019 en considerar que el procediment emprat per l’Administració per adjudicar el servei sense concurs públic estava avalat per la Llei de contractes del sector públic.

Pràctiques tèrboles

Com denunciava Eloi Badia, regidor d’Emergència Climàtica i Transició Ecològica de l’Ajuntament de Barcelona, les tèrboles pràctiques d’Agbar per aconseguir concessions l’han dut a ser imputat en tres macrocauses judicials (Pokémon, Púnica i Petrum), a més de ser expulsat en 2017 de la gestió de l’aigua a Girona després de demostrar-se la seva vinculació amb la trama del 3%.

Els informes d’aquesta última causa constataven que, durant més de dues dècades, els gironins van pagar més d’1 milió d’euros de sobrecost pel servei d’aigua. A més, l’Agència Tributària advertia que els directius de l’empresa havien carregat despeses personals a la societat i va concloure que Girona SA havia cobrat centenars de milers d’euros per serveis no prestats.

Com expliquem en l’article “Els serveis públics, cada vegada més privatitzats”, la privatització de serveis essencials avança de manera implacable a Europa des dels anys vuitanta. I això està tenint un preu inqüestionable per al conjunt de la ciutadania. L’agent d’11Onze Jordi Coll apunta que aquest procés ha suposat sotmetre la prestació d’aquests serveis “a la lògica de criteris de mercat i, per tant, dels beneficis privats”.

Si vols descobrir com beure la millor aigua, estalviar diners i ajudar al planeta, entra a Imprescindibles 11Onze.

For decades, the West lived with the feeling that prosperity was almost a natural right. But today many European and North American citizens feel that their standard of living is deteriorating. Housing is more expensive, job stability seems more fragile, and social mobility has slowed down. The question is inevitable: have Western middle classes actually become poorer?

Some economists, such as the renowned specialist in global inequality Branko Milanović, qualify this narrative. According to his research, Western middle classes have not become poorer in absolute terms. What they have lost is something else: their privileged position within the global economy. And although this distinction may seem technical, it is key to understanding one of the major transformations of the 21st century.

If we observe the evolution of real incomes in Europe or the United States over the past three decades, the conclusion is clear: middle classes have not become poorer in strictly economic terms. Incomes have continued to increase, but at a very modest pace, often below 1 % annually. This growth is sufficient to avoid a widespread decline in living standards, but too slow to generate a clear sense of progress. In absolute terms, many Western households today have broader access to goods and services than thirty years ago, from digital technology to international travel or a much wider cultural and educational offering.

However, this gradual progress has occurred in parallel with much faster transformations in other areas of the global economy. On the one hand, the enormous concentration of wealth in the hands of a minority within Western countries themselves has widened internal inequalities. On the other hand, the rapid rise of new middle classes in major emerging economies has altered the global economic balance. This double movement —the accumulation of wealth at the top and rapid growth outside the West— has profoundly changed the perception of prosperity and has fueled the sense that the economic center of gravity of the world is shifting.

When comparison reshapes the perception of prosperity

For much of the 19th and 20th centuries, Europe and the United States occupied an almost undisputed position within the global economic system. The Industrial Revolution, technological leadership and control over the main international financial institutions placed the West at the center of the world economy. But this order is evolving. In recent decades, economies such as China, India, Indonesia and Vietnam have undergone extraordinary processes of industrialization and growth, allowing hundreds of millions of people to access income levels that were once exclusive to developed countries.

This process has produced a significant paradox: while global inequality between countries is decreasing, the map of economic power is being redistributed. The West still concentrates a very large share of global wealth, but it is no longer the only center of prosperity. The rise of new emerging economies is gradually modifying the commercial, technological and financial balances that for decades defined the international economic order.

This shift also has a social and psychological dimension. Sociologists speak of relative deprivation to describe the perception that arises when other groups or regions prosper more rapidly. It is not necessarily a real impoverishment, but rather a constant comparison. In a hyperconnected world, where the internet and social networks expose lifestyles and economic opportunities from all over the planet, this comparison multiplies.

Products, technologies and experiences that once seemed exclusive to the West are now part of the everyday consumption of millions of people in other regions of the world, inevitably transforming the perception of one’s own economic status.

The end of a historical exception

The sense of economic insecurity running through many Western societies has deeper roots than the evolution of wages or the cost of living. What is changing is the global economic order that was built after the Second World War. For decades, institutions such as the International Monetary Fund and the World Bank reflected a balance of power dominated by Western economies, consolidating a system in which Europe and the United States occupied the center of global financial power.

Today, however, this balance is being redefined. The growing economic weight of emerging economies is forcing a reconsideration of the rules of the international game and a redistribution of influence within the global system. This does not necessarily imply the decline of the West, but it does mark the end of an exceptional situation: that of a small group of societies concentrating a disproportionate share of global wealth. When a society moves from being clearly dominant to simply competitive, the perception of loss can be intense, even if living standards continue to improve.

Understanding this transformation is key to interpreting the political, economic and social debates of our time. The questioning of globalization, tensions between economic blocs or the rise of disruptive political movements are all part of this same process of global rebalancing.

At La Plaça of 11Onze, we analyze these changes with a critical and pedagogical perspective to help the community understand how the global economy is evolving and, above all, how we can make more informed financial decisions in a world that no longer revolves around the West.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

The energy crisis and global economic uncertainty has boosted the purchase of precious metals such as gold and silver. The tax season starts on 6 April, so it is a good time to remember how precious metals are treated for tax purposes.

The central banks of several countries are increasing their gold reserves exponentially, but there has also been an increase in demand for this safe-haven asset from people who want to protect their savings in the face of an inflationary economic scenario that has no end in sight. Even so, more and more investors are including precious metals in their portfolios in order to diversify their returns.

However, before investing in gold or any other precious metal, it is important to consider what taxes are payable when buying or selling these highly valued commodities in times of crisis. Taxation can vary depending on whether you are buying physical gold or digital gold, the purity level of the metal, and other factors to consider when assessing the potential returns on your investments.

Investment gold bullion and gold coins

Firstly, we need to be clear that we are not talking about ordinary precious metals, such as those in jewellery or industrial sectors, but about precious metals of investment value. This distinction is important because according to the European Union decree 77/388/EEC, investment gold does not pay VAT either on purchase or sale.

The Tax Agency defines this special scheme for investment gold as “a compulsory scheme, without prejudice to the possibility of waiver for each transaction, applicable to transactions involving investment gold where such transactions are generally exempt from VAT, with partial limitation of the right to deduct”. In other words, the current VAT Law establishes certain requirements for it to be considered investment gold.

Therefore, investment gold will be exempt from paying VAT as long as it is physical gold, that is, gold bars or coins, such as the gold we offer through Preciosos 11Onze. In addition, this gold must meet minimum purity requirements: 99.5% in the case of bullion, and 80% in the case of coins. Bullion and coins that do not reach this purity will have to pay VAT at 21%, the same rate that applies to the purchase of other precious metals.

Income tax

Silver and other precious metals pay VAT like any other product, and each country applies its own tax rate, 21% in the case of Spain. Therefore, as investors, we have to bear in mind that these are different investments from gold, and often more speculative.

In terms of personal income tax (IRPF), any sale of gold, or any other precious metal by the taxpayer, has to be included in the tax return, and will be taxed according to the capital gains or losses generated by the operation, by the taxable savings base.

In this way, if a capital gain has been achieved with the operation, it will be necessary to reflect it taking into account the purchase price, including expenses, and the sale price, excluding expenses, with applicable rates depending on the amount.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Marc Vidal, lecturer and commentator, warns that 2023 could be the year of a crisis that would leave all previous crises as a “pure anecdote”, as predicted in 2019 in a book by Marc Friedrich and Mathias Weik. A confluence of different circumstances could create the perfect storm.

Is the mother of all crises looming? That is the question posed in the book ‘The biggest crash of all time’ by Marc Friedrich and Mathias Weik, which was a bestseller in Germany in 2019. The book predicts that a big economic crash will come this year, with an unmitigated collapse of the European stock markets. In short, “a crisis that will make any previous crisis a mere anecdote”, according to the lecturer and commentator Marc Vidal.

The book also features central banks that are “printing money as if there were no tomorrow”, bank deposits for which they charge you, and a catastrophic commercial situation. To these ingredients, we must add the increase in interest rates, which the authors of the book did not foresee and which is already being implemented by institutions such as the US Federal Reserve.

The burden of public debt

Marc Vidal warns that the interest paid by Spain each year amounts to 26.8 billion euros, which represents 2.15% of GDP and nearly 7% of the budget or, in other words, “half the cost of public education”. And he stresses that this is “only to pay interest, not to pay off debt”. In fact, the lecturer clarifies that “no state amortises a single euro of debt, what they do is refinance it every year”. And he points out that Spain has to refinance “237 billion” euros this year.

Vidal’s analysis of the Spanish situation is bleak: CPI above 8%, GDP barely growing by 0.3%, domestic demand falling by 3.7%, public debt at 118%, the forgotten risk premium at 100, unemployment at 13.65%, and energy once again at unacceptable levels. According to the writer, in order to rebalance the accounts, budget cuts would have to be “almost 10%”.

To deal with such a crisis, Marc Vidal explains that the authors of the book recommend investing in “real assets”, such as gold, and fleeing from the stock market and physical money, which will be devalued by the large amount of money issued by central banks. He adds that “it’s time to get moving, not standing still”.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Aprendre a administrar com gastem els nostres diners és primordial a l’hora de reduir les despeses familiars, i els petits desemborsaments poden acabar llastant la nostra economia més del que ens pensem.

L’empresari escocès-estatunidenc Andrew Carnegie (1835-1919) va formular la vella dita: “Take care of the pennies and the pounds will take care of themselves“, que ve a ser: “Cuida els cèntims i els euros es cuidaran ells mateixos”, per recordar als seus empleats de la necessitat de controlar les petites despeses. Tanmateix, aquests petits desemborsaments poden acabar llastant la nostra economia familiar.

Es coneixen com a despeses formiga tota una sèrie de petits pagaments per serveis o productes, de vegades innecessaris, que realitzem diàriament, quasi inconscientment, però que de mica en mica van minvant una part important del nostre pressupost al cap de l’any. Quantes vegades ens hem preguntat: “Però, en què m’he gastat els diners aquest mes?”.

Normalment, no donem importància a aquestes despeses quotidianes gràcies al seu cost relativament baix, això no obstant, identificar-les i reduir-les pot significar la diferència entre no arribar a fi de mes, o tenir un pressupost que ens permeti estalviar i anar de vacances.

Reduir les despeses invisibles

Tots som conscients dels costos de les factures de la llum, telèfon, gas, aigua, i les tenim assumides com un fet consumat. Tanmateix, per mandra, o per evitar problemes, poques vegades ens plantegem canviar de proveïdor per reduir el preu de la factura mensual. Un petit esforç que podria significar centenars d’euros estalviats al cap de l’any.

El cafè, el croissant, el menú del dinar, són petits capricis que ens alegren el dia, però un exemple perfecte de microdespeses, tot i que no sempre prescindibles, de les que en podem reduir el cost. Portar el dinar fet de casa o comprar al supermercat en comptes d’anar cada dia al bar només ens estalvia uns pocs euros setmanals, així i tot, sense dubte, ens sorprendrà l’estalvi que podem assolir en calcular quant suposen aquestes microdespeses en la factura anual.

Les comissions bancàries i les targetes de crèdit són unes despeses a les quals no donem massa importància, però que van sumant. Algunes entitats bancàries s’aprofiten del fet que aquestes petites comissions no seran vistes o reclamades pels clients. Reduir o eliminar el nombre de targetes de crèdit, i optar per una modalitat de pagament ajornat a final de mes que ens eviti pagar interessos, i són opcions que només requereixen un mínim d’esforç per la nostra part.

Canviar els hàbits de consum

Fixar-se en la compra de cada dia, comparar preus entre establiments o aprofitar les ofertes ens pot estalviar una quantitat important de diners, però canviar els nostres hàbits de consum és igualment important. Evitar comprar aigua embotellada, que sovint té un preu desmesurat, i beure aigua de l’aixeta o fer servir filtres, ens pot suposar un estalvi considerable que, alhora, contribueix a la reducció de residus plàstics al medi ambient.

Tanmateix, quantes vegades agafem el cotxe per distàncies curtes? I quant temps i diners perdem buscant aparcament? Potser podem plantejar-nos si una passejada, agafar el transport públic o fer servir una bici són més adients per alguns d’aquests trajectes. La nostra butxaca, salut, i el planeta ens ho agrairan.

Fer un replantejament dels nostres hàbits de consum i reduir les despeses formiga no ens ha de conduir a fer una vida monacal d’austeritat, al contrari, ens pot ajudar a tenir un bon pressupost per gaudir dels capricis que ens enriqueixen la vida, mentre eliminem despeses que ens la fan més difícil.

Si vols rentar la roba sense embrutar el planeta, 11Onze Recomana Natulim.

Throughout history, governments and their central banks have protected countries’ reserves by buying gold. Even so, in the face of economic uncertainty caused by the health crisis and runaway inflation, they have increased purchases in recent years.

Data published by the International Monetary Fund (IMF) confirms that central banks’ demand for gold recovered in 2021, with an 82% increase over 2020. Net purchases of gold by central banks amounted to 463 tonnes in 2021. This represents a significant pick-up in demand from this sector after a decade low of 255 tonnes in 2020, and the twelfth consecutive year of net purchases, during which central banks have bought a net total of 5,692 tonnes of gold.

Although central bank demand is often driven by policy rather than market demands, and therefore may be less predictable than other sources of gold demand, an upward trend is confirmed. A phenomenon that is nothing new if we are talking about emerging countries or countries not aligned with Western geopolitical interests, but to which a whole series of central bank buyers from developed markets were added in 2021.

For example, the Monetary Authority of Singapore (MAS) increased its gold holdings by just over 26 tonnes, a 20% increase, the first increase in at least 21 years. “The change in gold holdings is a result of MAS’s ongoing and continuous efforts to ensure that the Foreign Official Reserves portfolio remains highly diversified and resilient across economic and market conditions,” a MAS spokesman said.

Russia and China boost gold purchases

Economic sanctions imposed on Russia have prompted the Russian central bank to announce it will suspend gold purchases from banks to meet rising household demand for the precious metal and weather the storm in Russian markets. The abolition of value-added tax on these transactions, coupled with the rouble’s plunge to record lows, is spurring gold purchases by a population that wants to protect its savings.

However, both Russia and China have been increasing their gold reserves significantly for years. China almost certainly owns far more gold than anyone else, including the United States. We have seen many examples in recent decades of the latter country exploiting and abusing the dollar’s status as the world’s reserve currency to punish other countries contrary to its economic interests, thus accelerating the process of de-dollarisation and the creation of alternative gold-based monetary systems.

A process that is accelerating thanks to the conflict in Ukraine, and to the collaboration between Russia and China, not only to counteract the sanctions of the United States and the European Union, but also to ensure that the days of the hegemony of the Western monetary system are numbered in a multipolar world in which the Asian continent has more and more weight in the global economic balance.

In short, the wide range of purchases in 2021 has shown that there continues to be a significant demand for gold as a safe-haven asset, and the upside performance of this metal during periods of crisis has become the main reason for central banks to hold gold. A financial protection resource that is not exclusive to central banks, but is also available to everyone.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price, the refuge value par excellence: physical gold.

Les inversions financeres sempre comporten riscos, però si volem rendibilitzar els nostres estalvis sense desvincular-nos de les inversions, els metalls preciosos, considerats valors refugi, són una bona opció de poc risc. T’expliquem per què poden ser una bona alternativa d’inversió en temps de crisi.

La inversió es mou per un conjunt de forces econòmiques i polítiques que conflueixen per determinar la seva rendibilitat. Per norma general, com més potencialment rendible sigui una inversió, també vindrà acompanyada d’un risc implícit més elevat. Tanmateix, en un context econòmic mundial marcat per la incertesa, és d’esperar que alguns inversors pensin a protegir el seu capital amb l’adquisició de valors refugi com els metalls preciosos.

Davant d’una inflació que continua augmentant, els metalls preciosos, com per exemple l’or, ofereixen una protecció inflacionista única basada en el seu valor intrínsec, que no comporta risc de crèdit i no pot inflar-se. Això és veritat sempre que estiguem parlant de comprar ‘or físic’, però no és el cas si comprem ‘or paper’, a través de fons d’inversió, o altres modalitats, en dòlars, euros o qualsevol altra moneda que sí que es pot veure afectada per la inflació.

Dit això, una inversió significativa en or, o qualsevol altre metall preciós físic, pot resultar massa costosa a causa de les despeses transaccionals i d’emmagatzematge, per la qual cosa els fons d’inversió amb derivats o accions d’empreses mineres ens poden ser, a la pràctica, més convenients i versàtils a l’hora de diversificar la nostra cartera d’inversions.

En quin metall preciós invertir?

El sistema de divises de canvis fixos vinculats a l’or es va trencar el 1971 amb la fi dels Acords de Bretton Woods. No obstant això, l’or continua sent l’actiu refugi per excel·lència i un dipòsit de valor sense parangó que té tendència a revalorar-se quan hi ha incertesa en els mercats.

La plata és un metall molt més comú que l’or i amb un valor fins a 100 vegades inferior que el seu germà daurat, per tant, és més assequible i fàcil d’adquirir i vendre. La seva volatilitat és més elevada, però molt més estable que les divises, accions o bons, i també és considerat un actiu refugi per antonomàsia en cas de crisi econòmica.

Igual que la plata, el pal·ladi i platí són considerats metalls industrials, en aquest cas, especialment per a la indústria automobilística en forma de catalitzadors, o en processos industrials i electrònica. Tanmateix, es tracta de metalls que no tenen la mateixa facilitat de subscripció i que sovint requereixen grans aportacions i més coneixements financers.

Metall físic o a través de productes financers?

De la mateixa manera que l’adquisició d’un objecte de valor o una antiguitat és una compra que comporta poca complicació i està a l’abast de tothom que vulgui fer una petita inversió, l’or i la plata són igualment accessibles en format físic. No obstant això, és important comprar en un establiment que tingui el segell de la London Bullion Market Association (LBMA), que permet als particulars comprar i vendre or i plata amb unes mínimes garanties.

Si ens decantem per un fons d’inversió o ETF, hem de tenir en compte que no tindrem possessió del metall preciós, fet pel qual perd gran part del seu valor intrínsec, i que és un model d’inversió que dona més versatilitat, però exigeix uns coneixements borsaris bàsics que requereixen intermediaris professionals del sector.

Encara que els metalls preciosos representen una via útil i efectiva per diversificar els nostres estalvis i inversions, i ens poden ajudar a obtenir liquiditat en cas de necessitat, és crucial avaluar el risc que estem disposats a assumir i definir clarament els objectius d’inversió, abans de tirar-s’hi de cap.

Preciosos 11Onze t’ho posa fàcil perquè puguis comprar or al millor preu i amb total seguretat. Truca’ns i parla sense cap compromís amb un dels nostres agents per aclarir qualsevol dubte que puguis tenir i protegeix-te de les crisis econòmiques amb el valor refugi per excel·lència: Or Patrimoni.