The improvement of the extractive system

L’exuberància econòmica de finals del segle XVII farà creure a les monarquies europees que la riquesa del món és estàtica i que només cal repartir-la. La constant entrada d’or i de plata dins l’economia els permetrà universalitzar la seva idea de civilització, i s’aprofitaran de la meravella causada en aquelles cultures amb pràctiques i creences ancestrals. Dels 700 milions de persones que habitaran el món, quasi 120 milions viuran a Europa, atès que la mundialització —iniciada dos segles abans— els possibilitarà una varietat alimentària que els permetrà allargar la seva esperança de vida.

En finalitzar el segle, els europeus hauran verificat empíricament tota la terra, la qual cosa els permetrà generar una cartografia basada en l’observació de la realitat. Lluny quedarà aquella geografia imaginària fonamentada en les supersticions dogmàtiques. D’aquesta manera, apareixeran infinitud de descripcions sobre civilitzacions exòtiques dins l’imaginari europeu, el qual dibuixarà un canvi en els gustos —més orientalitzats— i suscitarà una progressiva actitud crítica davant les creences que els europeus tenen sobre el món. Aquest sentiment d’universalitat cultural s’anirà diluint a mesura que l’europeu entengui que el món també està habitat per una multitud de cultures i civilitzacions, les quals són diferents de les descripcions contingudes a la Bíblia.

Per tant, l’adopció del pensament crític comportarà la codificació enciclopèdica de la natura a través del revolucionari mètode científic, el qual es basarà en l’observació, l’experimentació i l’especulació empírica. La física —escrita amb llenguatge matemàtic— descriurà les formes i les mides dels cossos celestes, mitjançant l’ús de la recentment creada geometria analítica. I a partir d’aquest moment, la ciència esdevindrà un corpus de coneixement diferenciat de la filosofia i la religió. Tot plegat desembocarà en una percepció de la realitat que provocarà que les elits intel·lectuals europees es qüestionin conceptes tan bàsics com la propietat, la justícia, el poder i, per damunt de tot, la religió.

“L’adopció del pensament crític comportarà la codificació enciclopèdica de la natura a través del revolucionari mètode científic, el qual es basarà en l’observació, l’experimentació i l’especulació empírica.”

El qüestionament de la divinització del poder

De forma clara, l’Església — tant la catòlica com la protestant— haurà de fer front a multitud de veus discordants que dubtaran sobre l’origen diví dels textos sagrats, atès que es qüestionarà l’autoria divina de les Sagrades Escriptures. Aleshores, la religió esdevindrà un assumpte individual i privat entre l’home o la dona amb Déu. I en virtut d’aquesta privatització, els europeus progressivament s’alliberaran de dependre obligatòriament de les disciplines dogmàtiques imposades per l’Església des del segle X.

El fet de qüestionar el fonament sagrat que justificava l’existència dels Estats cristians, esquerdarà la legitimitat confessional de l’autoritat política representada pel monarca. Amb la presa de consciència del propi jo —a través del principi racional “cogito ergo sum”— s’inaugurarà la filosofia moderna que portarà als savis il·lustrats a qüestionar obertament la divinització del poder reial.

Aquest innovador pensament racional provocarà un xoc frontal entre els partidaris del poder absolut —en mans d’una sola persona i defensat aferrissadament per totes les monarquies europees— contra els defensors de l’estat natural de l’ésser humà, els quals argumentaran que “cap home no pot ser sotmès a la voluntat arbitrària d’un altre home, ni pot ser obligat a obeir lleis que un altre home no seguiria com ell.” Aquest pensament provocarà una profunda crisi de la consciència europea, la qual obrirà el camí cap a la invenció de la llibertat i la reclamació de la igualtat social.

El poder absolut i el mercantilisme

Els teòrics del poder monàrquic —com Jean Bodin o Thomas Hobbes— justificaran l’absolutisme com la forma més perfecta de govern i l’única capaç de gestionar la gran acumulació de riqueses que s’extreuen de les colònies. L’alt funcionariat —designat pel mateix rei— desenvoluparà mecanismes cada vegada més eficaços per organitzar meticulosament les finances de l’Estat, atès que els seus guanys no només s’aconseguiran per mitjà de la introducció de gran quantitat d’or i de plata dins del sistema econòmic, sinó que també es maximitzaran les exportacions i minimitzaran les importacions amb l’ajuda d’estratègics aranzels.

Convençuts que la riquesa del món era estàtica perquè només calia agafar-la, intercanviar-la o robar-la, les monarquies absolutistes perseguiran qualsevol intromissió o iniciativa privada que desestabilitzi el sistema del comerç internacional, com per exemple la persecució sistemàtica de la pirateria. En canvi, la multitud de conflictes bèl·lics entre les diferents monarquies europees —al llarg del XVII i XVIII— seran vistos com un intercanvi necessari de riqueses, territoris o persones en què totes hi sortiran guanyant o perdent, i d’aquesta manera es mantindrà el sistema econòmic viu, el qual sempre haurà de sumar zero.

Les monarquies europees —aclaparades per l’abundància— s’oblidaran completament de la vida dels seus súbdits. Meravellades per la situació, seran incapaces d’aplicar millores socials i econòmiques i aviat toparan amb el greu problema de la pobresa col·lectiva dins les seves societats. I en un context d’un incipient conflicte social —com serà el de principis del segle XVIII—, els economistes de l’època, Colbert, Mun, Serra o Misselden, defensaran l’aplicació d’una política de salaris baixos com única via per aconseguir la competitivitat en el comerç internacional, seguit del pervers argument que “si la població disposa de salaris superiors al nivell de subsistència, aquests esdevindran els causants de la reducció en l’esforç laboral.”

La riquesa extreta de les colònies, no només s’acumularà o es transformarà en els recursos productius que l’economia requereix, sinó que sobretot s’utilitzarà per ser exhibida a través de les arts —arquitectura, pintura i escultura—, les ciències i la cultura. I tot plegat desembocarà en una paradoxa quan les principals monarquies absolutistes —francesa, austríaca, russa o castellana— seran capaces de viure dins dels seus fastuosos palaus, en la més exquisida i refinada opulència, sense importar-los l’escassetat de recursos amb els quals vivien la majoria dels seus súbdits. Tanmateix, aquesta dinàmica estructural s’esmicolarà amb la irrupció del racionalisme il·lustrat dins del pensament europeu, que contribuirà al trencament definitiu de l’statu quo de segles d’excessos monàrquics. El despotisme il·lustrat li atribuirà al monarca la missió de portar el progrés econòmic i el benestar social a tots els seus súbdits, cosa que produirà infinitud de conflictes socials. I en aquest punt, no totes les monarquies europees abordaran el problema de redistribuir la riquesa de la mateixa manera.

“Les principals monarquies absolutistes seran capaces de viure dins dels seus fastuosos palaus, en la més exquisida i refinada opulència, sense importar-los l’escassetat de recursos amb els quals vivien la majoria dels seus súbdits.”

Dues solucions per a un mateix problema

Una de les respostes la donarà la Corona de Castella a través de les seves polítiques econòmiques, les quals encara li permetran ostentar una relativa predominança internacional. Malgrat tot, l’extracció massiva de metalls preciosos del “Nou Món” —que li havia permès obcecar-se amb la seva particular idea d’universalització cultural— li havia provocat una miopia i una nul·la adaptabilitat als moviments canviants de l’economia. Per tant, davant el repte de redistribuir la prosperitat entre els seus súbdits, es trobarà atrapada entre un deute gegantí i una societat poc dinàmica que dependrà majoritàriament de les decisions reials i dels recursos que arriben de les colònies. Tot plegat posarà de manifest l’existència d’una piràmide social parasitària que provocarà que un sol camperol —condicionat pel sistema de censos i de furs— estigui obligat a alimentar a trenta no-productors.

Per tant, l’estratègia que seguirà la Corona de Castella —a través dels ‘validos’ del rei, els famosos duc de Lerma, el comte-duc d’Olivares o el pare Nithard— serà la d’exercir una forta pressió fiscal mitjançant l’increment o creació de nous impostos sobre les fràgils economies camperoles, o sobre les classes urbanes per mitjà de constants pujades de preus i baixades de salaris. Aquest programa econòmic buscarà obtenir els màxims recursos per a continuar sustentant la idea d’Imperi, atès que fins aleshores els havia permès gaudir d’una balança comercial positiva. En contraposició, se situaran la noblesa i el clergat, els quals quedaran totalment exemptes de totes aquestes càrregues fiscals, a part de permetre’ls incrementar el cobrament de les seves rentes. Al capdavall, tot desembocarà en un important empobriment de la societat castellana, amb conseqüències tan desastroses sobre la natalitat i el despoblament de grans territoris de la Meseta, i que no es recuperarà totalment fins a principis del segle XX. I per reblar el clau, la societat serà segrestada pel Tribunal del Santo Oficio de la Inquisición, la qual vetllarà —a través de la censura, la crema de llibres “prohibits” i un integrisme misogin— perquè no germini cap pensament crític que defugi de la línia oficialista.

Per altra banda, trobem la resposta dels territoris del nord d’Europa —com són la Corona anglesa i les disset Províncies Unides— la qual suposarà introduir amb fermesa les idees il·lustrades dins la societat, la política i l’economia. Mentre Anglaterra acabarà constituint-se en una monarquia parlamentària, a través d’un procés polític que limitarà el poder del monarca i la separació de poders, la unió militar d’Utrecht —constituïda per les disset Províncies Unides— combatrà enèrgicament fins a la Pau de Münster l’ocupació de la Corona de Castella per esdevenir la república de les Províncies Unides del Nord. Ambdós territoris adoptaran una nova mirada sobre el comerç que provocarà la mutació del sistema econòmic i adoptarà una lògica de lliure mercat sense restriccions ni proteccions estatals. La generació de riquesa ja no es farà a través de la sang, sinó que serà per mitjà de l’habilitat que tingui l’individu en l’acumulació de capitals cosa que farà aparèixer la plusvàlua, origen de la nova conflictivitat. I en aquest nou paradigma econòmic, l’Estat ja no hi tindrà cabuda atès que els elements bàsics i irreductibles que impulsaran aquesta nova mentalitat serà —tant per empreses com per individus— sota l’imperatiu econòmic de maximitzar els guanys i minimitzar les pèrdues.

“En contraposició, se situaran la noblesa i el clergat, els quals quedaran totalment exemptes de totes aquestes càrregues fiscals, a part de permetre’ls incrementar el cobrament de les seves rentes.”

Canvi de paradigma econòmic

La universalitat cultural que havia imperat fins aleshores serà substituïda per nous raonaments basats en “si es pot demostrar que el rendiment econòmic que tota la producció industrial del món ha d’estar concentrada a Madagascar o a les illes Fiji o que tota la població d’Àfrica negra s’ha de traslladar al Nou Món per a treballar en les plantacions de cotó o de la canya de sucre, no existeix cap argument econòmic que pugui aturar aquestes iniciatives.” I d’aquesta manera, el capitalisme imposarà una globalització cada vegada més extensa i arribarà a regions cada vegada més remotes, les quals seran transformades de manera més profunda.

El món es dividirà en parcel·les productives seguint criteris globals com “no té cap sentit produir plàtans a Noruega perquè la seva producció és molt més barata a Hondures”. Per tant, quan els terratinents argentins només produeixin carn o els grangers australians només esdevinguin experts productors de llana, serà el moment en què hauran abandonat la seva pròpia producció agrícola, ja que els resultarà més beneficiós comprar les produccions cereals per l’autoconsum a l’exterior. D’aquesta manera, aquestes transaccions els permetrà especular i treure més rendiment econòmic a les seves inversions.

I en aquest sentit, tant Anglaterra com Holanda esdevindran els únics exportadors de capitals i serveis financers a les colònies americanes o asiàtiques amb la finalitat de desestabilitzar els antics imperis —Castella i Portugal— i d’aquesta manera assegurar-se les matèries primeres per a la incipient revolució industrial. Les borses de Londres o Anvers —fundades a finals del XVII— esdevindran les capitals comercials de la nova economia que es basarà sobre les expectatives d’un dinamisme especulatiu, les quals seran participades principalment pels descendents d’aquells jueus sefardites expulsats per la Monarquia Hispànica a finals dels XV.

Des del principi, tant Anglaterra com Holanda van tenir la certesa que per desenvolupar el nou paradigma econòmic calia engegar un procés de concentració de l’activitat econòmica per mitjà de la urbanització de les zones costaneres, cosa que els possibilità l’impuls de la construcció naval i el desenvolupament de manufactures properes als ports. Això els va permetre convertir els seus litorals en espais econòmicament molt dinàmics i potents. Un fet similar succeirà a la costa peninsular mediterrània, la qual passarà a ser un dels territoris amb un creixement econòmic similar al dels territoris del nord d’Europa. Serà aleshores quan Catalunya adquirirà la cohesió territorial sobre les bases d’un sistema urbà estretament entrellaçat amb Barcelona —com a centre comercial i polític— alhora que es desenvoluparà la indústria pels pobles propers —Sants i Sant Martí de Provençals— i l’activitat mercantil es reorientarà cap a l’Atlàntic i l’interior peninsular.

11Onze és la fintech comunitària de Catalunya. Obre un compte descarregant la super app El Canut per Android o iOS. Uneix-te a la revolució!

It is no secret that the linear production model we have applied so far, based on extracting, producing, consuming and throwing away, is unsustainable for life on our planet. The industry has long been suffering from the effects of natural resource scarcity and is exponentially increasing its investment in circular economy initiatives.

At our current rate of living, humanity needs 1.75 Earths per year. In other words, we use 75% more resources than our planet can regenerate, thus, for decades, we have been consuming more natural resources than the planet can replenish annually.

In the last 50 years, global use of material resources has almost quadrupled, outpacing population growth. Humans consume about 100 billion tonnes of raw materials per year, such as oil, gas and metals. Yet we reuse barely 9%, with the European Union alone generating more than 2.1 billion tonnes of waste yearly.

The current socio-economic system based on consumerism and a linear production model has its days numbered and can only guarantee its sustainability, both environmentally and economically, by establishing a circular economy system. A responsible and more sustainable production and consumption model must be established so that raw materials remain in the production cycles longer and can be used repeatedly while generating much less waste.

A change of mentality is needed to facilitate a transition towards a model based on reducing, reusing and recycling, instead of producing, using and throwing away. The aim is to achieve maximum development using as few resources as possible and generating minimum costs through a circular economy model.

The industry is taking action

According to a study by the German Federal Environment Ministry and consultancy Roland Berger, the global circular economy market volume generated €148 billion in 2021 and is forecast to grow to €263 billion by 2030, an increase of 78%.

A recently published ABB report entitled ‘Circularity, no time to waste’ reveals that in Spain, 94% of companies in the industrial sector are feeling the effects of the scarcity of natural resources, which has led 58% of them to increase their investment in circular economy initiatives.

Although the perception persists that the adoption of circular production practices entails additional costs, the study points out that their implementation can result in significant cost savings in the long term.

This reluctance to change is mainly because many companies still tend to focus exclusively on upfront capital and operating expenses, without taking into account that the simplified processes inherent in these practices increase efficiency and optimise resources. Thus, reducing waste and operating expenses in the long run.

Even so, the data show that most companies support circularity regulations and that, despite the lack of a standardised approach and the slow adoption of some practices, they will increase their investment over the next three years.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

Tenint en compte que vivim en un planeta amb recursos finits, el model econòmic actual basat en un creixement il·limitat sembla destinat al col·lapse. Però hi ha una alternativa viable? Estem preparats per assumir les conseqüències d’una reducció deliberada de la producció i del consum?

El creixement econòmic mundial es va veure esperonat per la revolució industrial i es va disparar a la fi de la Segona Guerra Mundial amb l’eclosió del consumisme. A partir dels anys 50 va començar un ràpid procés de creixement econòmic sense precedents que, tot i les recessions, s’ha mostrat imparable.

El consum d’energia per càpita va seguir un camí paral·lel després d’haver-se mantingut relativament estable durant dècades. I el mateix podem dir sobre l’ús de fertilitzants, consum d’aigua, producció de paper, etc. De la mateixa manera, les emissions de gasos d’efecte hivernacle i la pèrdua de biodiversitat van augmentar exponencialment.

És evident que aquest procés de desenvolupament va lligat a un augment de l’ús de recursos naturals, la contaminació i el canvi climàtic. Per tant, cal plantejar una transformació conscient i planificada de l’estructura econòmica i social per fer-la més sostenible.

Per a avançar cap aquesta transició ecològica es necessiten pactes que facin possible una reducció dels negocis ambientalment nocius en benefici d’altres més sostenibles i que formin part d’una economia circular. Potser més important, cal un canvi de mentalitat de la societat i, encara més difícil, d’una classe política ara supeditada als interessos corporatius.

Fugint d’una falsa dicotomia

A diferència del creixement econòmic, que es mesura per l’augment del producte interior brut (PIB), el concepte del decreixement econòmic és un moviment social i polític que fomenta la reducció deliberada de la productivitat i el consum i que promou la redistribució de la riquesa per assolir una vida més sostenible i equilibrada.

Els debats sobre l’actitud a prendre enfront del canvi climàtic o el model de creixement econòmic imperant sovint es redueixen a la confrontació entre aquests dos extrems. Per una banda, els partidaris de no canviar res per mantenir l’statu quo, per l’altra, els que ho volen canviar tot per desmantellar el sistema actual i substituir-lo per un model de decreixement.

Es tracta d’un fals dilema que divideix a la societat i no representa al públic en general. No té per què ser així. Per exemple, d’igual manera que tots podem estar d’acord a dir que és preferible millorar el benestar social en comptes d’empitjorar-lo, o el funcionament de les institucions públiques, o evitar els conflictes bèl·lics, segurament també ens posaríem d’acord si parléssim en termes de creixement sostenible o decreixement de les indústries contaminants.

Per altra part, no es pot aplicar la mateixa solució en l’àmbit global. El creixement econòmic ve acompanyat de la prosperitat i és molt fàcil i, fins i tot d’hipòcrita, advocar per un model de decreixement econòmic mundial des d’una posició de privilegi envers els països en vies de desenvolupament. Un dilema que no és nou i que ja ha generat tensions quant a les quotes de reducció de gasos d’efecte hivernacle.

De la mateixa manera, un decreixement econòmic imposat requeriria una intervenció estatal i una pèrdua de llibertats sense precedents, almenys en una societat democràtica. Estem preparats per assumir aquest major control governamental després del que s’ha vist amb les protestes dels pagesos en contra d’aquest tipus de mesures que s’han produït al llarg d’Europa? Podem assumir més impostos i més restriccions en el que podem o no podem fer?

No hi ha cap dubte que aquesta transició cap a un model de societat més sostenible és necessària, tanmateix, tant si s’opta per mantenir, incrementar o reduir el creixement econòmic, la solució passarà necessàriament per adoptar un model híbrid que sigui viable i capaç de cohesionar al conjunt de la societat.

11Onze és la fintech comunitària de Catalunya. Obre un compte descarregant l’app El Canut per Android o iOS. Uneix-te a la revolució!

The latest eurozone PMIs show worse-than-expected figures and support the case for a rate cut by the ECB in September. The private sector virtually stagnated in July, and the German economy suffered a further contraction in industrial production.

With the stock market meltdown of the last few days behind us, investors are now focused on the final Purchasing Managers’ Indices (PMI) data that several countries start to release later this week and which may signal a recovery of the eurozone economy.

Still, preliminary survey data from S&P Global shows weaker-than-expected numbers, indicating a negative outlook for eurozone manufacturers. On the one hand, the manufacturing PMI declined from 46.1 in June to 45.3 in July. On the other hand, the services PMI fell from 52.8 to 51.9. While the PMI for total activity fell to 50.1 from 50.9 in June.

According to S&P Global, new orders recorded a second consecutive month of decline, while business confidence fell to a six-month low, prompting companies to halt hiring that began earlier in the year. Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that “Preliminary PMI survey data point to a near stagnation in the euro area private sector economy in July as the single currency bloc’s economic recovery has continued to fade”.

Eurozone recovery in doubt

There are no signs of the significant recovery in the eurozone that was expected during the second half of the year. The new orders sub-index remained at its lowest level in three months. This has resulted in an acceleration of the decline in output and an increase in job cuts.

As a result, employment in the eurozone experienced its largest decline since December 2023, with job losses continuing for the past 14 months. “This data dampens hopes of a recovery,” Commerzbank analysts said, expressing concern that “this rebound looks set to be later and weaker than expected”.

“The widespread belief that the eurozone recovery would accelerate significantly in the second half of the year has not materialised. At the beginning of the year, it seemed that the sector would recover from the recession, but doubts that emerged in June have been exacerbated by a further downturn in July,” explained de la Rubia.

The German problem

While macroeconomic data released today shows that industrial production in Germany rose by 1.4% compared to the previous month, year-on-year industrial production fell by 4%. At the same time, exports continue to fall, dropping by 3.4% month-on-month in June, compared to a 3.1% month-on-month decline in May.

On the other hand, according to the S&P reading, July’s PMI index was 0.3 points lower than June’s, remaining at 43.2. Therefore, it is clearly below the 50-point threshold, which would signify an increase in economic activity, and also below 44 points, which indicates a contraction in industrial production.

The Hamburg Commercial Bank warns that “this data illustrates a serious problem. The German economy has suffered a further contraction, dragged down by a dramatic decline in industrial production.”

Protect yourself from economic crises with the ultimate safe-haven asset: gold. If you want your savings to keep or increase their value, Gold Patrimony.

The eurozone debt crisis widened the economic gap between northern and Southern Europe. The worst affected countries, Portugal, Italy, Greece and Spain, were pejoratively dubbed “PIGS” by northern countries which now see the southern economies leading European growth while their own are sinking.

The 2008 financial crisis had a devastating impact worldwide, especially in southern European countries. The bursting of the housing bubble in Spain, the debt burden in Italy, financial mismanagement in Greece and structural economic problems in Portugal led to drastic austerity measures following the intervention of the Troika, the triumvirate formed by the European Commission (EC), the European Central Bank (ECB) and the International Monetary Fund (IMF).

These countries were known as the “PIGS”, a pejorative term used by northern European countries when criticising southern countries’ debt and deficit management. Ireland was later added to the group of undesirables, even though Greece was the most prominent case because it had one of the highest debt levels.

The EU’s response was to approve plans for an economic ‘bailout’ that came with draconian austerity measures that bailed out mainly German and British banks at the expense of condemning generations of the populations of the supposedly rescued countries to pay this debt. These measures were extremely unpopular and provoked many social protests, well-known to the IMF executives.

Leading economic growth

A decade and a half after this financial defeat, the European economic scenario turned 180 degrees. Although the ‘PIGS’ continue to work their way out of the EU’s economic periphery, they have become its new engine of growth, while the northern countries are a drag.

During the last 12 months, the eurozone has dodged a technical recession by a miracle, however, Spain and the rest of the PIGS have managed to lead economic growth and be mainly responsible for preventing this technical recession from occurring.

It is true that the structural reforms implemented in industry, the labour market and the financial sector, together with advances in monetary and fiscal unity, contributed to improving the competitiveness of the southern countries, but other factors have influenced the economic recovery and leadership of recent years.

The better performance of southern European economies relative to the rest of the EU can be explained by developments in the energy sector and tourism, in particular the way these sectors have been affected by the war in Ukraine and the health pandemic. The greater weight of the tourism sector in the southern countries has been felt, as well as their lower dependence on Russian gas compared to other countries such as Germany, which has been hit by a severe self-imposed industrial crisis with the sanctions on Russia.

Aside from this recent economic revival in southern European countries, it remains to be seen whether they will be able to create a more sustainable economic model that is less dependent on tourism, control public debt and improve their productivity. In any case, it seems that being a ‘pig’ is not such a bad thing these days.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Europe is talking more and more about “strategic autonomy”. But what exactly does that mean? Energy, technological or military independence? Or is it just a political slogan in an increasingly fragmented world? Amid global geopolitical tension, the European Union is trying to redefine its role between the United States and China. And in this scenario, territories such as Catalonia may find a window of opportunity… or become trapped in a new dependency.

For decades, Europe has built its economic model on a basis that appeared efficient but was deeply dependent: cheap energy from Russia, competitive manufacturing from China and military security under the umbrella of the United States. This balance, which seemed functional, has broken down. The war in Ukraine, global trade tensions and the growing use of sanctions as a tool of geopolitical pressure have exposed an uncomfortable reality: Europe does not control its strategic levers.

The global economic system is not neutral, but rather responds to power structures that have generated technological, financial and commercial dependencies on a worldwide scale. This architecture limits the real sovereignty of territories and conditions their decisions. For this reason, the question is no longer whether Europe wants to be independent, but to clearly identify what it wants —and can— stop depending on.

Reindustrialisation: producing again… at what price?

One of Brussels’ answers is clear: reindustrialise Europe. The pandemic and the supply crisis revealed the extent to which dependence on China was critical, from microchips to pharmaceutical products. For years, Europe has outsourced its productive capacity, prioritising low costs over industrial sovereignty. Now, the shift is clear, with incentives to manufacture semiconductors, plans to recover strategic sectors and investments in renewable energy and raw materials.

But this process is not free. Producing in Europe is more expensive, and this has a direct impact on the economy: it puts pressure on corporate margins, may translate into higher prices for consumers and requires the deployment of massive public subsidies. Here emerges a central tension that will mark the future of the continent: to what extent autonomy can be gained without losing competitiveness in a globalised market.

At the same time, Europe is trying to reduce its dependence on the United States in key areas such as technology, payment systems and defence. However, the risk is replacing one dependency with another: critical minerals from third countries, new technological dependencies or the growing weight of large subsidised corporations. The challenge, therefore, is not only to change suppliers, but to fundamentally rethink an economic model that until now has been based on structural dependencies.

Catalonia: periphery or strategic node?

In this new scenario, Catalonia’s role is not obvious, but neither is it minor. It has a solid industrial base and a strategic geographical position in southern Europe that make it a natural candidate to become a relevant logistics and production node. Ports, infrastructure and a diversified business fabric can work in its favour in a process of reindustrialisation that seeks proximity and resilience.

However, this opportunity coexists with important structural limitations. High fiscal pressure and the lack of full economic decision-making capacity can act as a brake at a time when attracting investment is key. Added to this is a deeper problem: the imbalance between wages and the cost of living. When purchasing power is eroded, the domestic market weakens, and without robust internal demand, any industrial strategy loses solidity.

For this reason, the question is not only whether Catalonia can take advantage of this new stage, but under what conditions it will do so. It can be an opportunity if high value-added industry is attracted and the productive fabric is strengthened with greater decision-making capacity. But it can also be a risk if only costs are assumed and structural dependency is maintained. Ultimately, it is not enough to be part of the European map: there must be real room to define one’s own rules of the game.

Real autonomy or political narrative?

Europe wants to regain control over key areas such as energy, technology, defence and finance, but all these sectors are deeply intertwined with global interests. In this context, the risk of capture by large corporations or lobbies is not minor, especially within a system that often responds to dynamics of crony capitalism that distort political decisions. Recent history confirms it: major economic changes do not always liberate; they often redefine dependencies.

For this reason, the real question is not only to produce more or diversify suppliers, but to guarantee real sovereignty. This implies effective control over financial flows, tangible energy independence, technological autonomy and political capacity to define one’s own strategies. Without these pillars, autonomy is incomplete and may end up being only a well-constructed narrative. For Catalonia, the challenge is especially delicate: to take advantage of this new window of opportunity without becoming trapped in a new architecture of dependency.

The world is changing, and with it the rules of the game. Europe is moving, but the key question is whether we will move with judgement or be dragged along. Understanding these changes is not optional: it is essential to protect our savings, make informed decisions and build an economic future with more control and less dependency. Because true autonomy begins when we understand the system… and decide how we want to play within it.

11Onze is the community fintech of Catalonia. Open an account by downloading the app El Canut for Android or iOS and join the revolution!

If you would like to learn more about this topic, we recommend:

Economy

EconomyCatalonia in the face of the new globalization

5 min readAmid a full reconfiguration of world trade and with...

Social exclusion, job insecurity and difficult access to housing are some of the factors that generate anxiety and depression in a large part of the population. This deterioration in quality of life is related to one of the highest consumptions of anxiolytics in Europe and calls into question the sustainability of the current socio-economic model.

Despite losing positions in the ranking in recent years, according to foreign organisations, Spain remains among the nations with the highest quality of life index among developed countries. Not only this, but all the expats- an euphemism for immigrants from ‘first world’ countries – who live and work in Spain continue to choose it as the country with the highest quality of life.

This optimism, however, does not seem to be shared by the country’s autochthonous residents. This conclusion is drawn from a recent eco-social study by the FUHEM Foundation on Quality of Life in Spain. In fact, after analysing Spanish society focusing on three areas – expenditure, resources and work – it concludes that the quality of life of Spaniards has worsened significantly in recent years.

Specifically, the report points out that almost half of Spaniards feel lonely and that 27% of the population, or one in four people, are at risk of poverty or social exclusion. The social researchers who drafted the report state that this social isolation generates anxiety and depression, and connect this with the increase in the consumption of anxiolytics in Spain, one of the highest rates in Europe.

Decent work, access to housing and social protection

The prevalence of job insecurity is reflected in the fact that around 15% of the employed population in Spain is also at risk of poverty or social exclusion and that child poverty affects one in three children under the age of 16. In this context, two out of ten Spaniards live in substandard housing conditions, unable to maintain an adequate temperature in either winter or summer.

On the other hand, while 58.1% of young people had access to home ownership in 2007, today this figure has dropped to 25%. Today, it takes seven years of income to buy a home, a far cry from the 2.8 years required three decades ago. Furthermore, although the cost of renting a home should not exceed 30% of income, four out of 10 people spend 40% of their salary and one-fifth more than 60%, 6 points higher than in 2018 and 12 points higher than in 2014.

The cuts in public spending have been reflected in the lack of supply of social rental housing, which in 2020 represented only 1.1% of the total, a clearly insufficient percentage to cover the 4.5 million people who are in a situation of residential exclusion. This is a real estate model that not only makes it difficult for citizens to access housing but also gives preference to large investment funds and banking corporations.

The urgency of changing towards a more sustainable model

The study also questions our model of production and consumption that “has placed life under the tyranny of efficiency and performance”. Living an unhealthy life leads to higher levels of “permanent fatigue”, especially for poorer households that cannot afford a more varied and quality diet.

This is a problem that has been exacerbated by the rising cost of basic foodstuffs and the growing tendency to shop in large supermarkets, which the report links to the rise in obesity in Spain, one of the European countries where it has increased the most in recent years.

The NGO also stresses the need to stop the territorial fragmentation that causes social and ecological deterioration, pointing out that the mobility model based on private vehicles and roads is “highly inefficient”. In this sense, they warn that the public investments that have been made for the construction of large infrastructures respond more to private interests than to the public interest. In short, it is an unsustainable production, investment and society model that facilitates inequalities, castrating social cohesion and environmental balance.

One of 11Onze’s objectives is to transform realities that we do not like. We have an active, conscious and responsible community. Enter 11Onze Rolls Up its Sleeves to find out how you can contribute to helping other people around the world.

The US Federal Reserve will launch this summer a real-time payments system designed to streamline transactions between bank accounts. This is a development that some critics see as a further step towards a digital dollar to counter cryptocurrencies and eliminate cash.

In an increasingly digital and interconnected world, payment systems are evolving to meet the needs of businesses and consumers who demand access to fast payment services to make transactions more efficient and better control their cash flow. The private sector has been at the forefront of this evolution, but governments also want to play a role.

To meet these needs, the US Federal Reserve plans to introduce a new payment system known as FedNow in July this year. This new instant payment platform is designed to enable secure and efficient payments in real-time, 24 hours a day, 365 days a year.

This is a great advantage for businesses and consumers, as they will not have to rely on traditional processing times, which can now be several business days. The new system will allow funds to be transferred instantly between participating bank accounts, and as a non-profit governmental organisation, it will be able to offer more competitive prices.

On the other hand, the adoption of FedNow by US banks, corporations and major financial institutions could result in other foreign entities being forced to use the service. This is significant because it could help the dollar, also in digital form, to perpetuate its reign in international cross-border transactions. This is a possibility that cannot be ruled out in the face of increasing de-dollarisation and the announcement of the launch of a new currency by the BRICS group.

A new payment system linked to the digital dollar?

In parallel with the launch of FedNow, the Federal Reserve is considering the possibility of introducing the digital dollar. As other countries have done already, this would involve putting into circulation a Central Bank Digital Currency (CBDC). This proposal has been criticised on the grounds that it could affect the fundamental freedoms of citizens, increasing the ability of governments to track and control the population.

In this regard, Florida Governor Ron DeSantis and presidential candidate Robert Kennedy Jr, questioned the motives behind the possible introduction of the digital dollar and the new FedNow payment system. Specifically, Robert Kennedy Jr stated that the issuance of a digital dollar will serve as a mechanism to control US citizens, just like the FedNow payment system, declaring that “the distinction between FedNow and a CBDC is important from a technical point of view, but not from a civil liberties point of view”.

As a result of these statements that seek to link the two proposals, yet another controversy has been unleashed on social networks, in which content is circulating that claims that the Federal Reserve will launch a central bank digital currency called FedNow this July, which will give more power to the government to ratify financial slavery and political tyranny.

This misinformation has gone viral to the point that the Fed has deemed it necessary to officially deny it, stating that “FedNow is not related to a digital currency. FedNow is a payment service that the Federal Reserve makes available to banks and credit unions to transfer funds. The FedNow service is neither a form of currency nor a step toward the elimination of any form of payment, including cash.”

Additionally, federal officials – including Fed chair Jerome Powell and former vice chair Lael Brainard – noted that a digital dollar could still be years away from becoming a reality, but that FedNow could emerge as a better alternative to a CBDC. Be that as it may, the controversy is served, and is likely to further boost the case for cryptocurrencies as decentralised digital currencies that can be used as a defence against CBDCs or other state-backed monetary alternatives.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

La Unió Europea s’enfronta al seu declivi polític, econòmic i militar en el món. Els interessos particulars dels diferents Estats li priven d’una veu forta en el context internacional, on habitualment actua supeditada als desitjos dels Estats Units. En aquest context, la sobirania real d’Europa és gairebé una utopia.

S’apropen temps convulsos a Europa. La guerra d’Ucraïna ha disparat la tensió amb Rússia, que cada vegada estreta més els seus llaços amb la Xina. El conflicte ha portat els governs europeus a reforçar la seva aliança amb els Estats Units i replantejar-se les seves polítiques de defensa i energia. A més, la guerra ha provocat tensions en el propi si de la Unió Europea, que probablement aniran en augment.

On podem arribar? És difícil de dir. Europa ha recorregut un llarg camí des del pla Schuman de 1950 i el Tractat de Roma de 1957, que l’ha convertit en la segona major democràcia i la tercera major economia del món. Però, després del somni d’unió i prosperitat europea que va generar la caiguda del bloc comunista l’any 1989, l’idealisme europeu s’ha anat fonent com un terròs de sucre. Ho ha fet en un “desordre internacional” tutelat pels Estats Units i marcat per crisis econòmiques, pandèmies, un procés de desglobalització parcial i conflictes entre les grans potències.

Mai com ara la Unió Europea havia hagut de fer front a una situació internacional que avança cap a la multipolaritat i està plagada de crisi que plantegen nombroses amenaces i reptes. I ni tan sols ha estat capaç de desenvolupar la tan anhelada Política Exterior i de Seguretat Comuna (PESC).

Una certesa: la política exterior continua encara és un dels elements menys integrats de la UE. Així ho va demostrar, per exemple, el canceller alemany Olaf Scholz en un viatge a la Xina a principis de novembre de 2022. Aquesta visita va rebre una pluja de crítiques per part dels socis europeus perquè denotava un unilateralisme descarnat, ja que els interessos d’Alemanya xocaven amb els de la resta dels membres de la Unió Europea.

La desunió europea

No és cap secret que cada país defensa els seus interessos. Com advertia recentment Martin Wolf, responsable d’economia del ‘Financial Times’, alguns dels principals problemes als quals s’enfronta la UE tenen el seu origen en el fet que no es tracta d’un Estat, sinó d’una confederació d’Estats. D’aquí es deriven les dificultats de gestionar economies divergents dins d’una unió monetària en la qual el Banc Central Europeu exerceix un paper essencialment polític per evitar desequilibris insalvables entre les diferents economies.

Falta una veritable integració. La realitat és que el mercat únic europeu no està integrat com ho està el dels Estats Units, per exemple. La falta de dinamisme en un sector crucial en l’actualitat, com ho és el de les tecnologies de la informació i la comunicació, s’explica en gran manera per aquest fet. És simptomàtic que només una empresa europea, ASML, figuri entre les deu empreses tecnològiques més valuoses del món.

Res convida a l’optimisme. En un context internacional més fragmentat i amb majors pulsions nacionalistes, fins i tot Alemanya, que és l’autèntic motor d’Europa, cada vegada té més dificultats per trobar mercats que absorbeixin la seva producció. Els elevats costos energètics són una amenaça per a la seva indústria pesant. I s’afegeix l’embranzida de la Xina i els avenços dels Estats Units cap a una política intervencionista i proteccionista.

Aquesta situació fa que es trobi a faltar una veritable política europea comuna, llastrada pels interessos nacionals particulars, que fins i tot amenacen l’existència del mercat únic.

El rol d’Europa en el món

Una qüestió vital per a Europa, com assenyala Wolf, és definir el paper que vol exercir en el món, si desitja continuar sent un aliat “servil” dels Estats Units, convertir-se en un pont entre blocs o recuperar l’estatus de potència. La primera opció sembla la més plausible, ja que per tornar a convertir-se en una potència necessitaria una unió política i fiscal molt més profunda, a més de superar les desconfiances internes.

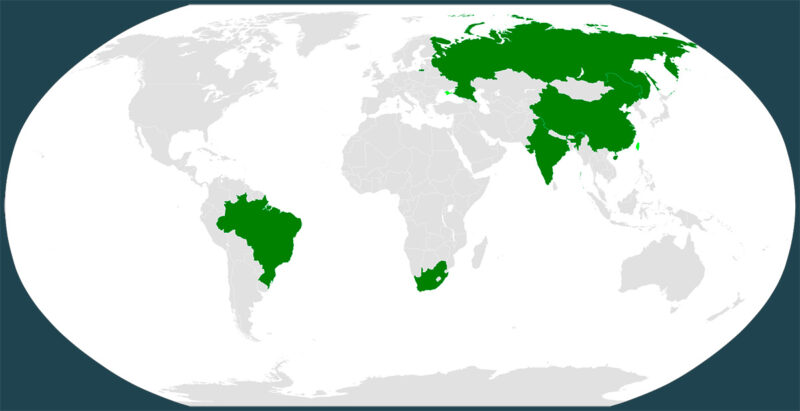

L’ascens de la Xina, l’Índia, Rússia i altres països com a potències econòmiques i militars obliga la Unió Europea a ser un actor amb una única veu en assumptes d’importància global si aspira a ser un dels “pols” rellevants en el futur multipolar. Però, com més activa i independent vulgui ser la Unió Europea, més crucial serà aprofundir en el seu federalisme, un procés plagat d’espines per les reticències nacionalistes.

L’auge populista

L’avanç dels moviments populistes a Europa des de la crisi financera de 2008 i la crisi migratòria de 2016 suposa una amenaça en aquest sentit. La majoria es caracteritzen pel seu euroescepticisme, ja que consideren que l’arrel dels problemes socioeconòmics a Europa és la integració europea i la presa de decisions de Brussel·les.

No estem davant un moviment marginal: un estudi del Pew Research Center mostra que els partits euroescèptics ja ocupen el 29% dels escons del Parlament Europeu, la xifra més alta de la història. Per tant, una part important dels qui prenen les grans decisions sobre el futur de la Unió Europea són també els qui s’oposen a una major integració. I, sense aquesta integració, és difícil que Europa recuperi un paper protagonista en el panorama internacional.

Escassos avenços

La Unió Europea va establir diverses prioritats per al període 2019-2024, entre elles la protecció i la llibertat dels ciutadans, el desenvolupament d’una economia forta, la sostenibilitat a Europa i la promoció dels valors i interessos europeus a escala mundial. Per desgràcia, els avenços en aquests àmbits han estat escassos.

Vivim en un món caracteritzat pel desordre, el creixent proteccionisme i els conflictes entre grans potències. Sens dubte, no és el món amb el qual somiaven els fundadors de la Unió Europea. Però si els seus dirigents actuals desitgen preservar alguna cosa de l’esperit original, haurien d’enfortir les bases del projecte i avançar cap a una sobirania real d’Europa. Per a això seria imprescindible frenar la desindustrialització, impulsar la transformació digital, aprofundir en la integració i establir una veu única en el món.

11Onze és la fintech comunitària de Catalunya. Obre un compte descarregant l’app El Canut per Android o iOS. Uneix-te a la revolució!

Catalonia is improving in productivity, but this improvement does not automatically translate into a real perception of well-being for the majority of the population. In 2024, total factor productivity contributed 1.8 points to the growth of Catalan GDP, which grew by 3.5% according to Idescat. In other words: a relevant part of growth no longer comes only from working more hours or accumulating more capital, but from producing better.

The problem is that this macroeconomic improvement coexists with a much less brilliant reality: living remains expensive, especially in the metropolitan area of Barcelona. We work with more technology, more efficiency and greater productive capacity, but, paradoxically, it is becoming increasingly difficult to make ends meet. Wages are rising, yes, but they do not always rise at the same pace as housing, food, energy or basic services. And when the cost of living rises faster than the available margin, productivity ceases to be perceived as an improvement and starts to be seen as a broken promise.

For decades, we have been repeatedly told an almost sacred idea: if the economy grows, society improves. If we produce more, we live better. This narrative has been the pillar of dominant economic thought, assumed as an unquestionable truth by both governments and institutions. But everyday reality is beginning to crack this narrative.

Catalonia —and Europe in general— has increased its productive capacity over recent decades. Companies are more efficient, technology makes it possible to do more with less, and GDP continues to grow in overall terms. However, this improvement is not reflected with the same intensity in the daily life of most of the population. Citizens do not live off GDP: they live off the salary they have left after paying rent, food, electricity, transport, taxes and debts.

This is where the data hurt. The average gross annual salary in Catalonia was 29,978.69 euros in 2023, 4.2% more than the previous year. But the median salary —more representative of the ordinary worker, because it is not so distorted by high salaries— was 25,826.11 euros per year. This is equivalent to around 2,152 euros gross per month in twelve payments, before taxes and social contributions.

The contrast with the cost of living is stark. According to the Metropolitan Area of Barcelona, the metropolitan reference salary —that is, the salary needed to cover a basic basket and live with dignity— stood in 2024 at an average of 1,527.83 euros net per month per adult. But for a single person in the city of Barcelona, the threshold rises to 1,886.14 euros per month, and for a single person with children it reaches 2,719.28 euros.

This means that a significant part of the population does not need “luxuries” to struggle financially: it only needs to pay for normal life. And this is the key point of the article. The problem is not that people live beyond their means; often, it is that real means have fallen below the ordinary cost of living.

Housing is the great black hole. In the city of Barcelona, the annual average rent of regular contracts was 1,134.61 euros per month in 2025. By district, Eixample reached an average of 1,283.96 euros per month, Gràcia 1,082.33 euros, Sant Martí 1,094 euros and Sarrià-Sant Gervasi 1,603.74 euros. Even Nou Barris, the district with the lowest average, stood at 796.21 euros per month.

These figures explain why so many people feel that their salary evaporates. If a person earns close to the Catalan median salary and has to live alone in rented accommodation in Barcelona, housing can absorb a disproportionate part of their net salary. And if we add food, utilities, transport, phone bills, insurance and taxes, savings are reduced to the bare minimum. It is not a feeling: it is arithmetic.

Inflation adds a second layer of pressure. In 2025, the annual average CPI in Catalonia grew by 2.4%, but the group covering housing, water, electricity, gas and other fuels increased by an annual average of 4.8%. In December 2025, Catalan year-on-year CPI was 2.5%, with housing and restaurants/hotels among the most inflationary groups, both at 4.1%.

Therefore, the problem is not only how much wages rise, but what happens to the items you cannot stop paying for. If the basic elements that sustain everyday life rise more, real disposable income falls even if nominal wages increase. It is the difference between “earning more” and “living better”. And today this difference is at the heart of the discomfort.

The fiscal trap: paying more without earning more

A factor that is often invisible, but decisive, is added to this reality: taxation. With inflation, income may increase in nominal terms, but this does not imply a real improvement in purchasing power. Even so, taxes can increase. This is what is known as “fiscal drag”: a silent rise in the tax burden when tax brackets and allowances are not fully adjusted to inflation.

In Spain, this dynamic coexists with tax revenues at record highs. In 2025, tax revenues reached 325.356 billion euros, 10.4% more than in 2024, according to the Tax Agency. The agency attributes the increase to the rise in tax bases and to the impact of regulatory and management measures.

The problem is that, for ordinary citizens, this macroeconomic explanation translates into a very specific experience: paying more VAT because prices are higher, paying more personal income tax if wages rise nominally, and seeing how part of any salary improvement is absorbed before it reaches the current account. The tax system acts like a sponge: it retains part of the increase before it can become well-being.

The result is an apparent paradox: wages may rise, but the available margin shrinks. And when this happens, citizens do not perceive progress, but tightening. They do not see “growth”; they see that every month they need more money to maintain the same standard of living.

In parallel, the current economic model tends to concentrate the value generated in the hands of actors with a greater capacity to capture rents: large corporations, financial sectors, asset owners and structures with influence over decision-making centres. This phenomenon has less to do with producing more than with better controlling economic flows. This is where productivity can become a trap: if the additional value is not distributed better, society produces more, but the majority does not live proportionally better.

Productivity without well-being: the great mistake

The great conceptual mistake is to confuse productivity with well-being. Productivity measures how much we produce with the resources available. Well-being measures how we live. And today these two indicators no longer necessarily move forward together.

We can have more efficient companies, rising GDP, more technology and more automation, but this does not guarantee that a family can pay reasonable rent, save money, have children or face an unexpected expense without going into debt. Productive improvement only becomes social progress when it reaches wages, available time, the cost of housing, the capacity to save and economic security.

In fact, this disconnect becomes evident in everyday life: growing difficulties in accessing housing, less capacity to save, dependence on credit and a widespread feeling of economic uncertainty. Wealth is created, but it is not always distributed in a balanced way. When citizens perceive that they live worse, it is not an illusion or an error of perception: it is a clear symptom that the system prioritises quantitative growth, penalises labour income and rewards capital, asset ownership and speculation.

The uncomfortable question is inevitable: what is the point of producing more if the majority cannot live better? What sense does it make to celebrate productivity if housing swallows up wages? What kind of prosperity is it that increases tax revenues, profits and GDP, but leaves citizens with less real margin?

The answer involves rethinking the foundations of the system: how wealth is distributed, what role wages play within the economy, how the abusive weight of housing on labour income is limited, what level of tax pressure is sustainable and, above all, what we understand by prosperity in the twenty-first century. Because productivity, by itself, does not fill the fridge, does not pay the rent and does not guarantee a dignified life. It can be a formidable tool for progress. But if it does not translate into sufficient wages, affordable prices and life stability, it ceases to be a promise of well-being and becomes a perfectly measurable trap.

11Onze is the community fintech of Catalonia. Open an account by downloading the app El Canut for Android or iOS and join the revolution!