Which savings option suits you best?

Fixed-term deposits, Treasury bills and mutual funds are the three main options chosen by households seeking to increase the returns on their savings to fight inflation. Even so, which alternatives offer better returns?

Despite the low remuneration for savings still offered by large banks, according to data published in December by the Bank of Spain, households have moved more than 50,000 million euros to fixed-term deposits since the beginning of 2023, for a cumulative total of more than 115,000 million euros in these products at the end of November.

The Spanish banking sector has shown itself to be one of the slowest in the European Union to reflect the European Central Bank’s interest rate hike with a better return on savings. The Spanish average of 2.45% remuneration on deposits of up to one year is still well below the 3.27% of the eurozone.

While Spanish banks suffered the worst flight of bank deposits in Europe during the first two quarters of the year, the public increased its investment in the Treasury to more than 28 billion euros in 2023, an unprecedented record. The high yield offered by short-term public debt has reached 4% (3.7% in the last auction) compared to the 2.45% average traditional banks offer for deposits.

On the other hand, households have also sought to make the most of their savings through guaranteed fixed-income investment funds, which promise investors, as of the maturity date, the recovery of the initial capital and also a predetermined fixed return. The low risk associated with these funds often comes with a low return, but in the current context, they can still be a good alternative to the fixed-term deposits offered by banks.

The savings options that 11Onze Recommends

Saving with 11Onze is always based on one maxim: they must be safe propositions. That is why we have decidedly opted for gold, because of its historic role as a store of value. With Preciosos 11Onze you can buy gold bars from £3,000 or Vienna Philharmonic gold coins from £225. We offer gold bullion in two formats that have counteracted the effect of inflation over the past two years: Gold Patrimony and Gold Seed.

A Guaranteed Fund with full security and an accrued interest of between 2.5% and 165%. The capital and returns are 100% insured by one of the world’s leading insurers. Therefore, you avoid market fluctuations and know for certain that you will get up to 35% interest on your money in 10 years.

If you want your savings to generate monthly income, 11Onze Recommends Monthly Return, a product that yields 22% in 2 years. It is a high-return, low-risk product, with the funds covered by insurance.

Social justice does not have to be at odds with generating returns on your savings. Thanks to Litigation Funding, you can help others who have been deceived by banks or the government, while earning returns of between 9% and 11% on your money.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze or have a look at the products that 11Onze recommends in our Marketplace.

In the last tender of the year, retail investors have turned to buying government debt. Households are seeking a return on their savings above the low remuneration offered by large banks for deposits, and are increasing their holdings of these assets to record highs. But are there other options that offer higher returns?

The last auction of the year of Treasury bills leaves 30% of government debt in the hands of individuals seeking a better return on their savings than that offered by banks for deposits. Although persistent inflation and rising interest rates have evaporated a large part of the savings accumulated by households during the sanitary crisis, the high yield on short-term government bonds has spurred the purchase of these assets.

While during the first two quarters of the year, Spanish banks suffered the biggest drain of deposits in Europe, the public increased its investment in the Treasury to over 28 billion euros in 2023, an unprecedented record. For the first time, Spanish households have become the main owners of Treasury bills, which account for almost one out of every three euros invested.

The high yield offered by short-term government bonds has reached 4% (3.7% in the last auction) compared to the 2.45% average offered by traditional banks for deposits. As for ten-year debt bonds, the yield surpassed 4% given the forecast that central banks would keep interest rates high for longer than expected.

A better return on your savings

The boom in the purchase of public debt is because, on the one hand, it responds to the needs of consumers at a time when traditional banks are not offering sufficiently attractive returns on savings and, on the other, to an apparent lack of alternatives readily available to the public.

This, however, is not exactly true. A product such as Litigation Funding, which 11Onze recommends, offers a higher fixed annual return than bank deposits and Treasury bills. In the short term, 1 or 2 years depending on the amount, it generates returns of between 9% and 11% with the peace of mind that an insurer covers our clients’ capital.

In this context, we should mention the safe-haven asset par excellence, gold. On 4 December, it reached its highest price ever, 2,100 dollars per ounce, and in the last 12 months, it has gone up by almost 11%, confirming itself as one of the best options for protecting our savings. Preciosos 11Onze makes it easy to buy gold, at the best price and with total security.

If you want to find out how to get returns on your savings with a social justice product, 11Onze recommends Litigation Funding.

Spanish banks are the ones that pay their clients the least for their deposits. Currently, several academics attribute the responsibility for the Great Inflation of the 70s of the 20th century to the fact that citizens stopped seeing their savings remunerated, pushing them to spend and boost inflation.

Spanish banks pay 0.04% for their clients’ demand accounts and 0.64% for deposits. They are, by far, the stingiest in Europe since in the EU they pay, on average, 70% more. This happens while posting record profits. The data not only speaks of crazy greed on the part of the Spanish banking system, it could also be a threat to the economy as a whole. And the reduction in the remuneration of savings was key to causing the Great Inflation of the 1970s in the United States, with a devastating effect on economies around the world.

Fewer returns, more spending

All this is explained in a scientific article by economist Itamar Drecshler, professor at the University of Pennsylvania and author of the aforementioned article, in collaboration with two researchers from New York University. In the article, the academics propose a rereading of the triggers of one of the biggest financial crises in history, which took away the savings of millions of people. Then, the inflationary period lasted from 1965 to 1982 and reached 14%.

At that time, a series of factors came together that terribly affected the economy: the enormous public spending to pay for the Vietnam War with the consequent abandonment of the Gold Standard due to the impossibility of supporting that volume of debt; the oil crisis and also a wage-price spiral that was chasing and pushing each other. All of this could not be brought under control until Federal Reserve Chairman Paul Volcker aggressively raised the price of money, pushing the country into a recession, to restore the Fed’s authority.

But there is one more element on the table that, until now, had not been pointed out as responsible for inflation and that could have had a lot to do with it. In 1965, financial legislation known as Regulation Q was implemented. In practice, it imposed a limitation on the remuneration of savings, which limited citizens from benefiting from possible interest increases. Penalizing savings in this way caused many people to stop seeing any point in saving, so they preferred to spend. As a consequence, the increase in demand caused prices to rise. Inflation evidently had the effect of reducing savings even further, because more money was needed to buy previously cheaper consumer goods. This spiral intensely damaged the United States economy and spread internationally.

“The President of the United States, Richard Nixon, made the country leave the Gold Standard to continue printing dollars to invest in the Vietnam War.”

History repeats itself?

The current scenario has points in common with what was experienced in the 70s or, at least, some errors are being repeated. The main thing could be to penalize citizens’ savings in an inflationary cycle. Because both the Federal Reserve and the ECB have already decidedly raised interest rates, but the banks have not passed this on to their clients. In this context, it is worth remembering that in 2021 inflation in Spain was 3.1%, in 2022 it was 8.4%, and in 2023 it returned to 3.1%. This implies an average price increase of 14.5% in 3 years. But, in addition, we must take into account that for some basic products in the shopping basket, prices have risen by more than 30%. If we add the very high public spending to support the ongoing war conflicts, we have a panorama surprisingly familiar to what happened in the 70s. And, not learning from historical mistakes, banks continue to be driven by greed instead of passing on the benefits to client returns generated by the ECB’s high interest rates.

One of the best options at an individual level to begin to stop this spiral is to find savings formulas that avoid excessive consumerism that further fuels the inflationary whirlwind. At 11Onze we strive to offer options so that our users do not see their savings degraded. We do this through products such as Preciosos 11Onze’s Gold, but also through products such as Litigation Funding that 11Onze recommends and that allow us to achieve profits of more than 9% for the money contributed. What, without a doubt, does not help stop inflation is spending our savings on products overvalued or letting the money dwindle in accounts without returns.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Tot i que qualsevol moment de l’any és bo per començar a estalviar, també és veritat que fàcilment podem trobar una excusa per no fer-ho mai. La pèrdua de poder adquisitiu per la inflació desbocada, els sous baixos, les rebaixes, el Black Friday! No obstant això, hi ha mètodes d’estalvi que requereixen un mínim esforç i estan a l’abast de quasi tothom. Càrol Rafales, de l’equip de producte d’11Onze, ens en presenta un de ben senzill de seguir.

Són moltes les persones que tracten d’estalviar per fer front a imprevistos, preveure futures compres o planificar unes bones vacances. Tantes com les que no saben com fer-ho, o que comencen a estalviar tot animades, però ho deixen córrer al cap de poc temps. Potser la clau està en anar pas a pas i començar a estalviar petites quantitats. Com apunta Rafales, “veritat que si us dic d’estalviar un euro la primera setmana, i dos la segona, no us sembla tan difícil?”.

Doncs en això es basa el repte d’estalvi de les 52 setmanes. Un mètode per estalviar fàcilment que consisteix a posar una quantitat de diners, durant 52 setmanes, en una guardiola, pot o el que t’agradi més, equivalent al número de la setmana que toqui.

El mètode d’estalvi de les 52 setmanes

De mica en mica s’omple la pica

Estalviar un euro la primera setmana, dos la segona, i així successivament, ens pot semblar ridícul, però si tenim en compte que al cap de l’any haurem estalviat 1.387 €, estem parlant d’una xifra que no és gens menyspreable. I que en tot cas, si tens un nivell d’ingressos prou elevat, “pots començar amb una xifra més elevada de” per exemple “21 €, per aconseguir més de 2.300 € al final de l’any”, explica Rafales.

Si no ens en refiem de la nostra constància en seguir aquest mètode, sempre podem programar una transferència setmanal a un compte d’estalvi, que fins i to ens pot donar uns interessos. A més, d’aquesta manera ens assegurem que aquests diners siguin de difícil accés ràpid, evitant temptacions de trencar la guardiola.

Si vols descobrir com beure la millor aigua, estalviar diners i ajudar al planeta, entra a Imprescindibles 11Onze.

Access to housing has become the main obstacle to real economic progress for Catalan families. Although wages have grown nominally, housing prices have risen almost twice as fast over the past decade.

The price-to-income ratio —which measures how many years of gross salary are needed to buy a home— now exceeds 9 years in Catalonia and 11 in Barcelona. This disconnect between income and housing cost explains better than any macroeconomic figure the widespread feeling of impoverishment. We work more, but buy less life.

Governments boast of rising wages, statistics confirm it, and companies echo it. But when the paycheck hits the bank account and faces the cost of living, the story falls apart. The numbers don’t lie: the gap between income and housing price is now so wide that ten years ago it would have seemed exaggerated.

Wages up, purchasing power down

According to Idescat, the average gross annual salary in Catalonia in 2023 was €29,978 (men: €32,721; women: €27,240) —a gender gap that still persists. The Spanish National Statistics Institute (INE) puts the national average slightly lower, at €28,049.

Despite this nominal rise, cumulative inflation above 15% between 2020 and 2024 has eroded purchasing power. Adjusted for CPI, real purchasing power has fallen by around 6% in five years, according to Eurostat. In theory, wages are improving. In practice, not enough: the cost of essentials —energy, food, transport— is rising faster than salaries. The Labour Observatory already warned in 2022 that, despite nominal growth, purchasing power was declining. More euros on paper, less real reach.

As a result, household income rises in nominal terms but falls in real value. Average savings have decreased, while essential consumption absorbs an ever-growing share of family budgets.

Loss of purchasing power: –6% in 5 years (Source: Idescat & INE)

The price wall: unaffordable housing

Market data confirm the tension. Across Catalonia, prices per square meter range between €2,400 and €2,500, while in Barcelona city they approach €5,000/m². The Property Registry Statistics confirm recent records and sustained increases in sales. In historical terms, the current cycle already exceeds the peaks of the pre-2008 housing bubble, even adjusted for inflation. The difference: supply is scarce, and credit is more selective.

A 75 m² flat at €2,500/m² costs about €187,500. With a gross annual salary of €30,000, that equals 6.25 full years of income (before taxes and interest). In Barcelona, with prices between €4,500–€5,000/m², the cost rises to €337,500–€375,000 —over 11 or 12 years of salary.

The Bank of Spain uses the housing price-to-income ratio as a measure of effort. Nationally, it already stands at 6–7, but in Catalonia’s urban areas it easily reaches 9 or 10. That’s a decade of work —for a roof.

When housing swallows a growing share of income, everything else shrinks: food, health, mobility, education, culture. Saving becomes difficult, and each year there’s less room for unexpected expenses. In the rental market, the pressure is no lighter: in Barcelona, a 70 m² flat costs around €1,200–€1,300 per month —a large portion of an average net salary.

When rent or mortgage payments exceed 30% of income, it’s considered housing stress. In Catalonia, a significant part of the population already lives under these conditions. The result: delayed emancipation, prolonged cohabitation, and shared renting as a structural solution.

The Catalan average exceeds 9 years (Source: Bank of Spain).

A market playing in another league

The problem is not just cyclical, but structural. Catalonia drags a chronic housing shortage: for years, construction has fallen short of demographic needs and new household formation. Affordable land is scarce, urban planning is slow, and new developments arrive in drips.

At the same time, the entry of large investors and the treatment of housing as a global financial asset have fuelled price pressures. A house is no longer just a place to live —it’s a store of value, an insurance policy, and a bet. As the market heats up, citizens cool down: they work, save… and still can’t reach it.

The purchase price is just the cover. Inside lie transfer taxes (ITP/IVA), stamp duties, notary and registry fees, and other expenses that can add 10–12% on top. Once financed, interest adds another layer: with higher rates than in previous years, the total mortgage burden can stretch across two generations.

Talking about homeownership as a synonym for stability has become ironic. A house provides shelter, yes, but it also conditions life decisions: having children, changing jobs, moving cities. You own it —but it owns you.

1 in 3 Catalan households lives under housing stress (Source: Idescat and Observatori Metropolità de l’Habitatge, 2024).

The extraction mechanism

This model works as a system of income extraction that falls mainly on the middle class. It’s no coincidence that birth rates are falling, the age of emancipation is rising, and life plans now depend on interest rates.

Housing —which should be the foundation of a dignified life— has become a condition. A “golden cage” where freedom is defined not by walls, but by debt.

Toward a new residential contract

Escaping this loop requires consistent, long-term policies. It demands:

- A sustained push for public, social, and cooperative housing so that access to shelter doesn’t depend on economic cycles.

- Urban planning agility and better land management to accelerate affordable construction.

- Targeted taxation to penalize underuse and incentivize rehabilitation.

- Transparency and rental market governance, with stabilization tools in proven high-pressure areas.

- Energy efficiency measures to cut monthly bills and improve quality of life.

Housing: a right or a lifelong mortgage?

The value of a home shouldn’t be measured in euros per square meter, but in peace of mind —the certainty that you can live without drowning financially. If it takes ten years of salary to buy a home —not counting taxes, fees, and interest— the problem isn’t just the price; it’s the place housing occupies in our social contract. Rebalancing it isn’t optional; it’s a condition for the future.

11Onze is the community fintech of Catalonia. Open an account by downloading the app El Canut for Android or iOS and join the revolution!

The rise in food prices has reached record highs in the last year. Filling the shopping basket has become much more expensive. Despite this, doing without basic foodstuffs is not a savings option that we can contemplate. Likewise, there are other fixed household expenses that we cannot eliminate, but which we can reduce. Here at 11Onze we have a savings proposal that you may not be aware of.

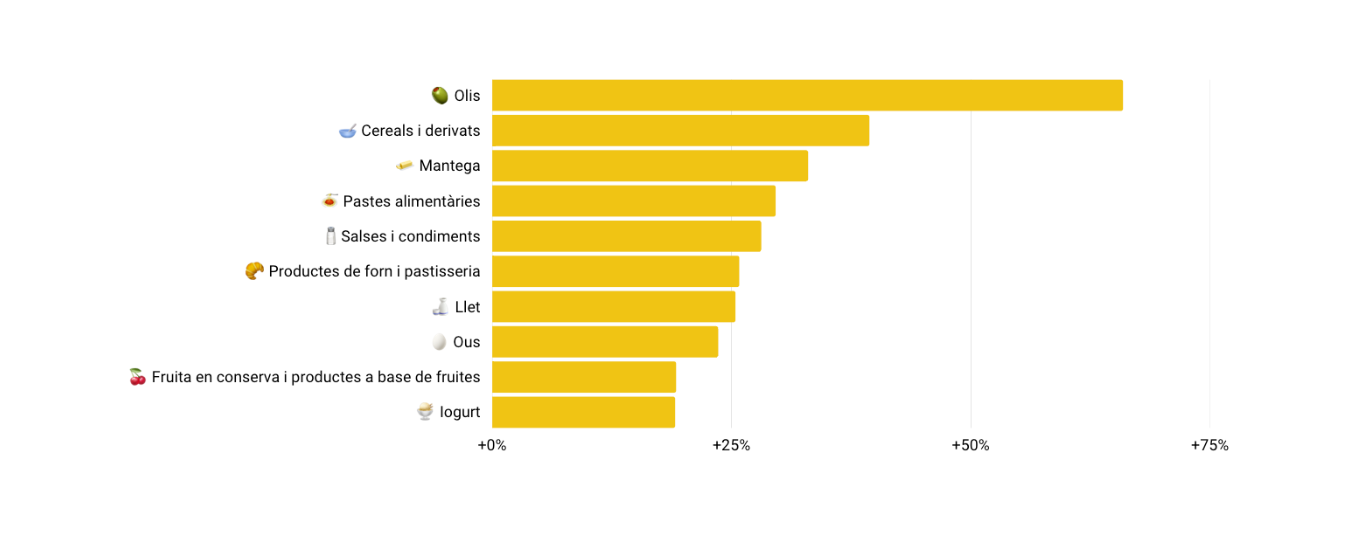

Although inflation seems to have peaked after two consecutive months of decline, prices are still totally out of control and the main foodstuffs that make up the shopping basket continue to get more expensive. According to data from the National Statistics Institute (INE), the year-on-year rate of food and non-alcoholic beverages prices has risen by 14.4% in one year, the highest since 1994, when the statistical series began.

The INE report tells us that the list of foods with the highest price increases is headed by oils, whether sunflower, corn or olive oil, which have shot up by 66%, followed by basic products such as cereals, butter, pasta or sauces and condiments, which have risen by almost 30%.

Source: INE

The causes are many and varied: the increase in production, transport and distribution costs, the rise in the price of raw materials, fuel and energy, but the end result is that no product has fallen in price or even maintained its price. It’s no secret, the cost of living has risen dramatically, and you have to make savings wherever you can.

Optimising fixed costs

Although it is true that we have little room for manoeuvre if we want to reduce essential expenses such as food, it is also true that there are other fixed expenses that, although necessary, can be negotiable, or we can optimise them by contracting suppliers that are more in line with our needs.

This category includes products and services such as household supplies, the mobility option and insurance. The home insurance sector offers us a wide range of providers with coverage and prices that adapt to our particular circumstances. This is where we can reduce costs without having to do without the essentials. Would it surprise you to know that with 11Onze Segurs you can insure your own home for as little as €5 a month?

From £5 a month? Yes, at 11Onze Segurs we do away with paper contracts, physical agencies, management fees, cancellation and contract change fees, which is already a considerable saving, but we also allow you to modify and adapt the coverage to your needs at any time, before and after signing the contract.

In this way we ensure that you don’t overpay for your insurance, offering a monthly or annual fee, without permanence, between 15%-20% cheaper than with traditional insurers. What is the monthly cost of your current home insurance? Do you want to know how much you could save? Try our price simulator by entering some basic data, and you will get your no-obligation quote immediately.

If you want to discover fair insurance for your home and for society, check 11Onze Segurs.

Both gold and cryptocurrencies have gained prominence in investment portfolios. They are very different, almost antagonistic, assets. Gold is much more stable and is considered the safe haven asset par excellence in times of crisis such as the current one. In contrast, the cryptocurrency market is highly volatile and can generate large gains, but also huge losses.

Gold and cryptocurrencies are investment assets with very different characteristics and behaviour. To begin with, gold is a tangible asset, with limited reserves, while cryptocurrencies are intangible assets, whose value depends largely on speculative manoeuvres.

Moreover, the gold market is mature, while the cryptocurrency market is much more recent and dynamic. The proliferation of cryptocurrencies has led to a more than tenfold increase in just two years.

Diversified demand

One characteristic of gold that sets it apart from most financial assets is that demand comes from a variety of sources, from central banks and private investors, who accumulate gold bullion and coins, to the jewellery industry and digital device manufacturers, who use gold in the creation of their products.

After a small decline in 2020, gold demand in 2021 returned to over 4,000 tonnes. Just over half (53%) went into the creation of jewellery, 28% was converted into bullion and coins, 11% was purchased by central banks and similar institutions and the remaining 8% was used in the manufacture of electronic devices.

Gold consumption grew in all four areas, although it was particularly strong in jewellery, where it rose from 1,327 tonnes in 2020 to more than 2,220 tonnes in 2021.

The high demand for gold in this industry is based not only on its aesthetic qualities, but also on its malleability and ductility. But the precious metal is also a key component of electronic devices, from mobile phones to televisions, as it is an excellent conductor of electricity and heat.

Central banks and private investors accumulate gold to protect their wealth. Indeed, countries hold huge reserves of this precious metal because they know that its value will not fluctuate greatly, as a limited amount is mined each year.

Concentrated ownership?

Despite what you might think, gold ownership is highly fragmented. The reserves of the largest gold owner, the US government, account for only 4% of the total. In fact, almost half of the precious metal is in jewellery scattered around the world and just over 20% belongs to investors accumulating gold bullion or gold coins. Nor is gold mining concentrated in just a few hands, with no single continent accounting for more than 30% of global production.

When it comes to bitcoin, the most important cryptocurrency, both ownership and computing power are less widespread. Only 2% of bitcoin holders accumulate 95% of all available bitcoins. And in 2021, entities in five countries controlled 80% of the computing power of the bitcoin network.

Because gold has multiple uses, its price is more resilient to economic swings than that of many other assets. When times are lean, investors buy gold as a safe haven. And when economies are doing well, consumers buy more jewellery and electronics that use gold.

Stability or volatility?

Between September 2021 and September 2022, gold has appreciated by 11%. In contrast, in the same period bitcoin lost half of its value due to speculative manoeuvres. On the other hand, gold can be considered a more liquid asset than many of the cryptocurrencies.

Some studies show that investors view cryptocurrencies as a high-risk, high-yield speculative bet, as their price swings wildly. In contrast, gold is much more stable. Therefore, both assets can have a place in a diversified and balanced portfolio. However, it is not advisable to allocate more capital to cryptocurrencies than you can afford to lose.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Airline tickets can make up a significant percentage of the cost of your holidays when travelling to distant destinations. Keeping the following recommendations in mind can allow you to save a good handful of euros.

As we explained in the article “When there is no money for holidays”, one of the big trends for travel this year is “the search for maximum savings”. With 20% of the budget, transport is one of the main planned expenses, according to a study by the National Observatory of Outbound Tourism, and we must bear in mind that this percentage can skyrocket if we travel far away. That’s why we offer some recommendations for saving on airline tickets.

- Book in advance. Bear in mind that it is essential to book your desired flights in advance in order to get the best prices. The closer you get to the date of travel, the more expensive the tickets tend to be, as airlines increase prices as the plane fills up. If you are flexible with your destination, another alternative is to wait until the last minute in case a flight does not fill up and a last-minute offer comes up.

- Better during the week. Flights on weekends are usually more expensive than during the week, so having flexibility in dates will help you pay less for the same journey.

- Reduce your luggage. Carrying a small amount of luggage will save you from having to pay for checked luggage. In addition, light luggage will make it easier to get around and to use public transport. To minimise your luggage, it is a good idea to take clothes that dry quickly and can be easily combined with each other.

Tips for saving on this summer holidays

In addition to saving money, one recommendation for making the most of your holidays when you are travelling to distant destinations is to take advantage of stopovers: choosing connections that are sufficiently spaced out in time can allow you to visit the city where you are making the stopover.

Do you love to travel? With 11Onze Viatges you can book accommodation at the best price, without stifling the travel industry.

Amb l’actual inflació, els diners al banc no fan més que perdre valor dia rere dia. Però sempre és necessari mantenir una mica de liquiditat per si sorgeix algun imprevist. Per això els experts recomanen tenir un “matalàs” d’efectiu en els teus comptes d’estalvi que cobreixi com a mínim tres mesos de despeses.

La vida està plagada d’imprevistos. També en el pla econòmic. A vegades són positius, com un augment de sou, però a vegades hem d’afrontar sorpreses desagradables que fan mossa en la nostra butxaca. Pot ser des d’una despesa puntual extraordinària, com quan hem de reposar un electrodomèstic vell de casa, fins una cosa més seriosa, com patir una malaltia incapacitant o quedar-nos sense treball.

Per fer front a aquestes eventualitats, és necessari disposar d’un fons d’emergència. L’antic costum de guardar els diners en el matalàs o en qualsevol altre amagatall de la casa et permet disposar d’ells de manera immediata, però és poc recomanable pel risc de robatori i la nul·la rendibilitat.

És preferible recórrer a les entitats bancàries, tot i que has de tenir en compte el límit del Fons de Garantia de Dipòsits d’Entitats de Crèdit per a que els teus diners sempre estiguin protegits.

Assegura els teus estalvis

Com detalla el seu web, aquest organisme “té per objecte garantir els dipòsits en diners i en valors o altres instruments financers constituïts en les entitats de crèdit, amb el límit de 100.000 euros per als dipòsits en diners”.

Això desaconsella tenir més de 100.000 euros en comptes i dipòsits a termini d’una mateixa entitat, ja que el fons només cobrirà fins a 100.000 euros per titular en cas que el teu banc faci fallida.

Si, per exemple, tinguessis 120.000 euros en una entitat que ha fet fallida, encara que fora en diversos comptes o dipòsits, aquest organisme només et retornaria 100.000 i perdries els altres 20.000. D’aquí la conveniència de repartir els diners entre diverses entitats per a que els comptes i dipòsits no superin el límit garantit en cap d’elles.

De quant parlem?

Només en casos molt excepcionals el nostre fons d’emergència hauria d’assolir aquests 100.000 euros, especialment en un moment com aquest, en el qual l’elevada inflació fa que els diners dipositats al banc perdin valor mes rere mes. De totes maneres, l’import òptim dependrà en última instància de les nostres circumstàncies personals: bàsicament, quines són les nostres despeses previstes i amb quins ingressos podríem comptar en cas d’un esdeveniment negatiu.

Els experts solen recomanar que el coixí financer cobreixi com a mínim tres mesos de despeses. Cal tenir en compte que mantenir un saldo massa baix en el nostre compte ens pot fer entrar en números vermells amb facilitat, la qual cosa generaria despeses financeres pel descobert.

L’OCU, per exemple, indica que una quantitat prudent en els comptes corrents “pot ser l’equivalent a tres mesos del teu salari”. No recomana més perquè aquests comptes “no són el millor lloc per a mantenir els nostres estalvis, ja que pràcticament cap entitat les premia amb interessos”.

Quant al màxim, no sol recomanar-se més del necessari per a cobrir sis mesos de despeses. De fet, el portal ‘Finances per a tots’, una iniciativa del Banc d’Espanya, la Comissió Nacional del Mercat de Valors i el Ministeri d’Assumptes Econòmics i Transformació Digital, aconsella “acumular un fons equivalent a entre tres i sis mesos de despeses”. A partir d’aquí es tracta de buscar inversions que garanteixin una bona rendibilitat.

11Onze és la fintech comunitària de Catalunya. Obre un compte descarregant la super app El Canut per Android o iOS. Uneix-te a la revolució!

Although the major international economic organisations try to send a reassuring message about controlling inflation, the UK’s experience in the 1970s raises serious doubts. Gold appears to be an interesting option to protect against the depreciation of money amid a “bear market” cycle that could last longer.

For months now, inflation has been far exceeding the optimistic forecasts of the major international economic organisations. The harsh reality means that time and again these institutions are forced to recalculate their forecasts upwards.

They all coincide in sending out a reassuring message. The mantra is that this year’s out-of-control rates will tend to moderate in 2023 and that by 2024 a rate close to the desired 2 % will be restored. The interest rate hikes by the major central banks should make a decisive contribution to this.

The latest to make this point is the International Monetary Fund, which, in a report, predicts that wage restraint will prevent a dangerous inflationary spiral.

Learning from the past

However, some economists warn that there are parallels between the current situation and the stagflation experienced in the UK half a century ago. Since 1970, the British government had been doping the economy with expansionary budgets and lower interest rates. As a result, inflation soared to 9.1 % in 1973, similar to today’s rate.

As now, interest rates had started to rise. Between June and November 1973 they rose from 7.5 % to 13 %, which led to the bursting of the housing bubble and the ensuing banking crisis. Moreover, between May 1972 and January 1975, the main stock market index lost 74 % of its value. The economic slowdown did not prevent inflation from spiralling out of control: it reached 16% in 1974 and a whopping 24.2% in 1975.

The big concern is that history will repeat itself. The bad news is that the spread between the inflation rate and interest rates is now much wider than it was then, so the monetary policy correction could have a much more devastating effect on the economy. The overall contraction in bank credit will be severe and many firms will become insolvent.

At current inflation rates, interest rates and the cost of government debt would logically soar. And, predictably, central banks will do what they have always done in the past to deal with this type of crisis: print more banknotes, which will further reduce their real value.

Gold, a safe-haven asset

The rise in interest rates in the early 1970s was no obstacle to the appreciation of gold: it went from less than £18 per ounce when interest rates were 6% to more than £40 when they rose to 13% in November 1974. For, as the founder of J.P. Morgan said, “gold is really money, everything else is credit”.

Since the suspension of the Bretton Woods agreements in 1971, which meant abandoning the gold standard, the sum of banknotes and commercial bank credit has increased more than 30-fold, which is equivalent to its devaluation. In fact, middle-class single-earner households were common before 1970 and are now a utopia. Buying a house or even a car without going into debt has become a privilege only within the reach of a few rich people.

Gold, on the other hand, has taken the opposite path to that of the money supply and its value has increased 38-fold. In fact, since December 2015, gold has appreciated by more than 40% against the euro.

Endorsed by the biggest hedge fund

Hence, the recommendation by Bridgewater Associates, the world’s largest hedge fund, to buy physical gold is not surprising, despite the fact that many investors see the current depreciation of many other financial assets as a buying opportunity.

Rebecca Patterson, chief investment strategist at Bridgewater, says the reason for going into gold is the need to protect against a “bear market” phase that is set to continue over time. Consequently, the logic of buying assets in the economic downturn, when prices are low, only to sell when the economy expands and rises again may not hold true this time around.

Moreover, both the Chinese and Indian economies are regaining their historical appetite for gold, which will contribute to gold prices in the short term.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.