Misrepresenting the reality of the labour market

Unemployment rises slightly in Catalonia in July, despite the fact that the employment record has been maintained. But can we trust the reliability of the official data? Are there inactive workers who should be counted as unemployed?

Catalonia has registered an upturn in unemployment after five consecutive months of a downward trend. According to data published by the Ministry of Labour, during July, the Catalan labour market added 1,612 more unemployed people (+0.49%) than in June. Despite this slight increase in unemployment, it remains the lowest unemployment figure since the 2008 crisis.

Currently, there are a total of 331,356 unemployed people, but in the last year, the total number of unemployed has been reduced by 10,035 people, 2.94% less. Compared to 2022, there are 103,185 more contracts, which is equivalent to a 2.8% increase. In total, there are 3.75 million workers in Catalonia and an unemployment rate of 8.44%.

The unemployment figures for Spain as a whole also reflect the best figures for 15 years. The Spanish economy continues to create jobs and reduce unemployment for the fifth consecutive month, although the pace slowed in July to below the historical average. The active population increases to 23.8 million people and the number of employed exceeds 21 million, another record high.

Unemployment stood at 11.6%, a fall of 11.7 points, after 365,300 people found work in the second quarter of the year, adding 595,614 people to Social Security since January. On the other hand, the number of unemployed registered at the offices of the public employment services fell by 10,968 people in July, -0.41% compared with the previous month, to a total of 2.68 million.

Inactive workers who are not registered as unemployed

In March 2022, the latest labour reform came into force, one of the main objectives of which was to change the production model, moving from temporary to permanent contracts in order to reduce temporary employment and precariousness. Therefore, work and service contracts disappeared, while the possibility of temporary contracts was restricted to very specific situations that cannot exceed 90 days worked per year.

In exchange, it was proposed that companies should use fixed-term contracts so that people doing seasonal work would not have to worry about whether their contract would be renewed after a period of inactivity and would have the same rights as workers with a permanent contract.

Despite the benefits for employees that this type of contract brings, it has the counterpart that workers who were previously considered unemployed are no longer counted as unemployed. In other words, when an employee with a fixed-term contract enters a period of inactivity, he or she receives unemployment benefits, but is not counted as unemployed, but is considered a “jobseeker with an employment relationship”.

This is a significant number of people who, in Catalonia alone, last year accounted for 5.7% of all workers affiliated with Social Security in Catalonia under this type of contract. If we take figures for the whole of Spain in December 2022 and January of this year, they were equivalent to 443,078 and 660,000 unaccounted jobseekers.

Obviously, the official data do not include the people who are looking for work but who are not registered with the SOC or the SEPE, either because they are self-employed, because they do not make any profit, or because they are part of the underground economy. Nor is it specified how many people work part-time, not because they want to, but because they cannot find another full-time job.

And it is true that these figures are difficult to account for, but more transparency in the data related to discontinuous permanent workers does not require any effort, but the simple will to reduce the divergence between the reality of the labour market and the official rhetoric, an unavoidable necessity if we really want to evaluate the effectiveness of employment policies.

Do you want to be the first to receive the latest news about 11Onze? Click here to subscribe to our Telegram channel

El primer de maig s’associava històricament amb festivals pagans vinculats a la primavera fins que la Segona Internacional va establir en aquesta data la festa del treball. Ho va fer l’any 1889 per commemorar la sagnant lluita dels obrers nord-americans per la jornada laboral de vuit hores.

El fet que el Dia Internacional dels Treballadors se celebri l’1 de maig té el seu origen en la lluita dels treballadors dels Estats Units per la reducció de la jornada laboral, que en la segona meitat del segle XIX s’allargava en molts casos fins a les 16 hores.

A mesura que el sistema capitalista s’afermava en les grans ciutats industrials dels Estats Units en un entorn d’elevada desocupació, les condicions laborals dels treballadors s’havien anat endurint. Davant aquesta situació, la Federació del Treball va convocar una vaga general que havia de començar l’1 de maig de 1886 per exigir la jornada laboral de vuit hores.

Repressió obrera

El 3 de maig, les protestes a Chicago es van tornar violentes quan la policia va actuar amb extrema duresa contra els treballadors mentre es manifestaven. L’endemà, un míting celebrat en la plaça Haymarket de la ciutat es va tenyir de sang durant la intervenció de la policia. Una bomba va esclatar entre les files dels uniformats, encara que per als historiadors no és clar si l’objectiu eren ells o els obrers, i va matar a set policies. Tot seguit, els agents van obrir foc contra els manifestants, matant a diverses persones i ferint a centenars.

Com a conseqüència, es va celebrar un judici que va condemnar a vuit homes per l’acció. Quatre d’ells van acabar penjats, tot i que no es van presentar proves que els relacionessin amb la bomba. De res va servir tampoc la campanya internacional per salvar les seves vides. Van ser premonitòries les paraules que va pronunciar August Spies, un dels condemnats, just abans de la seva execució: “Arribarà un moment en què el nostre silenci serà més poderós que les veus que avui escanyeu.”

Reconeixement a la lluita obrera

La Segona Internacional va establir l’1 de maig com a festa del treball l’any 1889, donant origen a l’actual celebració del Dia Internacional dels Treballadors. Paradoxalment, els Estats Units, el país on es van produir els fets, va voler desvincular aquesta data dels moviments obrers. Per això el president Grover Cleveland va fer que el Dia del Treball se celebri al setembre.

Amb anterioritat als successos de Chicago, als Estats Units i part d’Europa el primer de maig era una data marcada per celebrar l’exuberància de la primavera en l’àmbit rural. L’origen d’aquesta festivitat es troba en les antigues pràctiques romanes de celebració de la floració primaveral.

11Onze és la fintech comunitària de Catalunya. Obre un compte descarregant l’app El Canut per Android o iOS. Uneix-te a la revolució!

To find a job in the digital age, one needs more than just technical skills. Interpersonal qualities are critical to success in an increasingly complex and diverse work environment. Professionals who can master these competencies will be better prepared to thrive and face the challenges and opportunities presented by the labour market of the future.

The new technological revolution we are experiencing has brought about an accelerated digitisation and automation of many tasks, driven by artificial intelligence, which is radically transforming the labour market. This radical evolution of the nature of work requires new skills and personal competencies that will be critical for future jobs.

It is a paradigm shift that is enabling a reduction in workload without reducing productivity and could also make it feasible to reduce working hours to facilitate work-life balance, reducing stress and improving workers’ health and well-being. Even so, it may have a negative impact on people by replacing some jobs with automation or reducing available working hours.

In this context, while some jobs will become obsolete, others will emerge to replace those that will disappear. We expect this to happen in terms of both quantity and quality of employment, but at the very least it will require effort and investment in education and training.

Problem-solving, creativity and adaptability

Although there will continue to be many skilled jobs that will see little change, the labour market will increasingly require more dynamic and creative professionals who have a strong ability to adapt to change.

In fact, according to a study by the Skills and Occupations Barometer of Catalonia, promoted by the Universitat Oberta de Catalunya (UOC) and PIMEC, this skill is most highly valued by companies when hiring future professionals. Specifically, it was found that 51% of job offers published in Catalonia in 2023 required this skill, which is also in demand in most sectors (96%) and occupations (68%).

Likewise, the most valued qualities are the ability to assume responsibility, manage time, and accept criticism. These data are especially relevant in ICT occupations, which also concentrate the demand for people with the ability to “think creatively” and “solve problems” which, on the other hand, is significantly requested in 70% of the sectors and 40% of the occupations,

On the other hand, the barometer found that the importance of “teamwork” is particularly concentrated in professional, scientific and technical activities, where 24% of vacancies require this skill. In any case, and as Antoni Cañete, president of Pimec, emphasised, we are talking about “soft skills”, which can be applied to all professions and refer to “very human, transferable and transversal” skills.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

Sembla obvi, però, per aprendre a administrar els nostres diners, és primordial, primer, que ens els hàgim guanyat. Aconseguir diversificar els nostres guanys és una estratègia que ens pot blindar enfront d’una possible recessió o d’un imprevist. A 11Onze recopilem tres consells bàsics per fer-ho.

En moments d’incertesa és clau saber respondre a: com estalviar, com fer créixer els estalvis i com controlar les despeses. Difícilment serem experts a trobar respostes per totes tres preguntes alhora, però, si entenem els conceptes que s’amaguen rere cadascuna d’elles, tenim moltes més possibilitats de gestionar els nostres diners adequadament. No només aprendrem a cobrir les necessitats bàsiques, sinó que sabrem gaudir-ne i tindrem molt clar quan hem de prescindir d’aquelles que no ho són tant com ens pensàvem.

Estalvi: almenys un 10% dels ingressos

Sovint es diu que l’estalvi és la base principal de l’èxit financer. Tenir diners estalviats és el que ens dona la capacitat de respondre a situacions imprevistes —bé sigui una incapacitat per malaltia o càrrecs inesperats—, començar un negoci o tornar a estudiar. Però és important no confondre l’estalvi amb la inversió: mentre que el primer ens dona tranquil·litat, fins i tot en moments de crisi econòmica global, la inversió pot fer que els nostres estalvis es multipliquin, però també pot ser una font de maldecaps i la causa que perdem la nostra liquiditat.

Un dilema que ens podem trobar és si liquidar el deute o estalviar. Tot dependrà del tipus d’interès que tingui aquest deute. En casos d’interessos alts, com poden ser els de les targetes de crèdit, és generalment preferible deixar aquest deute a zero abans de plantejar-se l’estalvi. Però, en casos en què l’interès del deute sigui baix, com pot passar amb una hipoteca o, fins i tot, un crèdit personal, és raonable estalviar i alhora liquidar el deute lentament.

Creixement lent, risc baix, i a la inversa

Un compte d’estalvi ha estat la manera més tradicional que creixin els nostres diners, sobretot per a la gent més conservadora i poc aficionada al risc. Però, amb interessos relativament baixos i una inflació que ens visita molt més sovint del que seria desitjable, altres formes d’inversió van guanyant terreny, especialment davant d’una clientela cada dia més erudita en temes financers i amb un poder adquisitiu relativament superior a les generacions precedents.

En aquest punt, l’oferta de productes d’inversió és extensa i variada, amb diferents nivells de risc. Cadascú ha de ser conscient dels seus coneixements financers i, sobretot, de la quantitat de diners que s’està disposat a arriscar i perdre, especialment si l’expectativa de creixement és elevada i a curt termini. Cal tenir en compte que un gestor d’inversió pot ser una molt bona opció a l’hora d’escollir un producte financer que millori la rendibilitat dels nostres estalvis d’una manera substancial.

Despeses: necessitat vs. desig

Evidentment, no estalviarem tot el que guanyem, però hem de distingir entre dos tipus de despeses:

- Despeses de primera necessitat. Aquí hi comptem les despeses en el que és bàsic que necessitem per viure, com poden ser el menjar, l’allotjament, els subministraments d’electricitat, l’aigua, el transport públic, entre d’altres.

- Desitjos i productes més superflus. Per eliminació, hi incloem tot el que no és estrictament necessari. Hi trobaríem les compres impulsives, articles de luxe, viatges de lleure, etc.

Fer aquesta distinció no implica que no puguem gastar diners en coses que desitgem, però que no necessàriament ens calen. El desig i les accions que no tenen una finalitat merament pràctica són part de la condició humana. Això és un fet. Per tant, també ens hem de permetre aquestes despeses, sempre que ens adherim a un pressupost preestablert, bé sigui setmanal o mensual.

11Onze és la fintech comunitària de Catalunya. Obre un compte descarregant l’app El Canut per Android o iOS. Uneix-te a la revolució!

The reasoning is both simple and powerful: the most important and profitable asset of any company is its employees. So what could be better than keeping the organisation’s most important asset in its natural state, where its full potential manifests itself?

However, this reasoning does not apply exclusively to the workplace. Its connotations are paramount, since all people are workers, at least potentially, whether in active work, post-work, academia, or any other situation. It is evident, then, that happiness transcends any of these reasoning, to go to the common denominator: the human being.

Scientific research into happiness

Talking about happiness is nothing new, Aristotle was already making profound dissertations in the 4th century B.C. However, in recent years, the concept of positive psychology, which is a current of psychology that studies the bases of psychological well-being and happiness, as well as human strengths and virtues, has gained momentum. It differs from other psychology currents and its historical precedents in that it is based on the scientific method. Psychologist Martin Seligman laid its foundations at the end of the 1990s, and other authors, such as Mihály Csíkszentmihályi, have added to it with their contributions.

At first glance, the purpose of positive psychology may sound too arrogant: ‘now science wants to tell us what happiness is? But there are many dissenting voices who believe that happiness goes far beyond the processing of a simple set of measurable values in the realm of psychology.

Debates aside, we all know, without needing to learn it, when we feel good and, above all, when we feel bad. It is innate. The fact is that our organism goes smoothly with wellbeing, while it starts to give warning signals when we experience discomfort.

What do the experts say?

Given that companies are above all groups of people, it may seem basic to ensure the well-being and satisfaction of workers at work. However, in the business logic linked to the Industrial Revolution (still very present everywhere), the general paradigm has been quite the opposite: to make them work to the maximum in order to obtain higher profits. A vision in which their personal well-being is far from the company’s concern.

Studies on the subject conclude that the experience of workers who feel at ease in their organisation is far more precious than even the material goods they may receive as gratification. This is because this experience has no shelf life; it can always be recalled and enjoyed again.

Health techniques for coping with telework

Employee happiness as a barometer of business health

So now it is no longer just about focusing on the famous customer experience (CX), but the employee experience also plays a key role in the success of the organisation. Both from the company’s point of view, because a happy, creative or empathetic employee is synonymous with a more productive worker, and from the worker’s point of view, because we spend almost a third of our lives at work.

A good sign of the consolidation of this trend is the emergence of several indices, such as the Global Workplace Happiness Index, which measure happiness in the workplace. Likewise, the figure known as Chief Happiness Officer or director of well-being is consolidating in those organisations that are committed to the value of people and the profitability of a happy employee.

What a strange mix and, at the same time, what a fruitful synergy when the focus of the organisation is on people!

At 11Onze we have believed in this fundamental value from the beginning, which is shared by all the people who make up our community. And it works!

If you want your business to take a big leap forward, use 11Onze Business. Our business and freelance account is now available, find out more!

La pujada generalitzada de preus està complicant les finances de moltes llars. Cada vegada és més difícil quadrar els comptes per a arribar a final de mes i encara més dedicar una part dels nostres ingressos a l’estalvi. Davant aquesta situació, recollim onze consells per a millorar l’economia familiar.

- Aplicar la fòrmula del 50/30/20. Es tracta d’intentar distribuir els nostres ingressos de forma que el 50 % es dediqui a les despeses (llum, aigua, lloguer, hipoteca, telèfon, menjar, estudis…), el 30 % al nostre oci (les nostres sortides en esmorzars o dinars fora de casa, vacances, regals…) i el 20% restant a l’estalvi.

- Retallar subscripcions innecessàries. A quantes plataformes digitals estem subscrits? Les fem servir totes? Cal que les continuem pagant? I aquella subscripció a aquella revista que mai acabem llegint? Totes les subscripcions automàtiques s’han de revisar per valorar si són necessàries. Avui en dia existeixen diferents plataformes amb contingut en línia que són legals i gratuïtes, només cal fer una ullada per Internet per trobar-les. I recordem que les biblioteques també són una gran font de llibres i contingut audiovisual.

- Revisar els nostres contractes de llum, gas i telèfon. Cal revisar amb molta cura els contractes que tenim amb les diferents companyies de serveis. És una de les partides on més diners se’ns en van sense adonar-nos al cap de l’any. No podem prescindir d’aquestes despeses, però sí reduir-les.

- Fer més àpats a casa. Reduir les vegades que sortim a menjar fora de casa o que comprem menjar per emportar-nos pot arribar a ser una molt bona font d’estalvi. No cal deixar d’anar als restaurants, però sí reduir la quantitat d’àpats que fem fora de casa, i més si som una casa de família nombrosa.

- Reutilitzar. Quan una cosa se’ns faci malbé, mirem si podem reparar-la i allargar-ne la vida abans de llençar-la a les escombraries. També és una bona eina d’estalvi comprar roba de segona mà, llibres, mobles i fins i tot electrodomèstics.

- No comprar impulsivament. Una de les raons principals per les quals no fem un bon ús dels nostres diners són les compres compulsives. A partir d’ara, quan vulguem una cosa, donem-nos un marge de temps per saber si de veritat la necessitem. Ens sorprendrà comprovar que podem prescindir de gran part de les coses que volem comprar a cop de targeta.

- Comparar preus. Quantes vegades ens ha passat que comprem un telèfon mòbil, per dir un exemple, i l’endemà veiem una oferta del mateix producte en una altra botiga? Això ens passa per no comparar. Hem d’aprendre a comparar tot el que comprem, fins i tot el menjar.

- Fer servir menys el cotxe. Tot i que molta gent no pot prescindir del transport privat, sí que en podem reduir l’ús. Mirem d’utilitzar el transport públic o compartir cotxe si és possible. I fem ús també de la bicicleta, i sobretot, de les nostres cames, que caminar és sa i gratuït.

- Escollir una bona entitat financera. Són necessàries totes les nostres targetes de crèdit? Quines comissions ens cobra la nostra entitat financera? Revisem si aquesta entitat financera ens ajuda a tenir una bona economia personal, o si, per contra, cal que fem un canvi. Actualment, hi ha moltes entitats financeres amb eines que ajuden a controlar les teves despeses i que alhora et donen un cop de mà per estalviar: escollim una bona entitat financera pel nostre futur.

- Adaptar-nos a la nostra butxaca. Si ingressem una certa quantitat de diners, no fem més del que la nostra economia es pot permetre. No cal “estirar més el braç que la màniga”, com diem els catalans. Fem un ús responsable dels nostres diners segons els nostres guanys.

- Ser previsors. Hem d’analitzar l’evolució de les nostres despeses en els últims mesos per comprovar en què se’ns va els diners i on podem retallar. Davant l’actual situació inflacionària, en alguns casos serà necessari aplicar una “economia de guerra” segons com estimem que evolucionaran els nostres ingressos i despeses.

Ja fa dies que sabem que els diners no fan la felicita. Però podem aportar estabilitat a la nostra economia personal per evitar-nos disgustos. A més, en aquests temps d’incerteses econòmiques, val la pena recordar la frase que ens va deixar el filòsof Sèneca: “No és pobre qui té poc, sinó qui molt desitja”.

Si vols descobrir la millor opció per protegir els teus estalvis, entra a Preciosos 11Onze. T’ajudarem a comprar al millor preu el valor refugi per excel·lència: l’or físic.

Women hold only 34% of managerial positions in Spain. An insufficient number that has brought to light a new leadership, in female key, which breaks and weakens more and more social barriers.

Spain establishes, by law, that people of the same sex should not exceed 60% in private management positions. It seeks what, in the words of the philosopher and economist John Stuart Mill, would be a “perfect equality that does not admit power and privilege for some or incapacity for others”. In practice, however, the figure is blurred and this purpose remains a challenge. Since women entered universities in 1910, they have encountered the paradox that, despite having the same education, they cannot access the same positions.

Female leadership: reinvent the future

A working life marked for generations by male bosses and which, little by little, as the figures show, opens the door to the other half of society. And while the difficulty of accessing certain positions remains, family life reconciliation remains a challenge and the pay gap a reality, more and more women are taking the reins of their professional lives and, therefore, of their life. Female leadership brings to light this revolutionary spirit which, far from the patterns hitherto marked, claims that power can also be conscious, transformative, and sustainable.

Entrepreneurship and sorority: leadership takes new forms

Talking about female leadership is often talking about entrepreneurship. The observatory conducted by the company Extraordinaria in 2020 found that 58% of entrepreneur women did it out of necessity. This figure can make us think of circumstances such as the difficulty of promoting within companies, the impact of family life reconciliation or motherhood on working life, or the exclusion from the market that many women of a certain age suffer. The causes are many, and the answer is clear: if they cannot follow the path marked by society, they will make their own path.

This is the case of Gemma Fillol, who has shown from her experience that entrepreneurship becomes leadership. She is currently the CEO of Extraordinaria, the entrepreneurship and feminine leadership network that connects more than 50,000 women in Spain. Based on the figures in the study, she points out that “women work for different reasons than men. In fact, one of the main fears of entrepreneur women is not billing but not being able to handle everything. In the end, it is the here and the now that moves us. At Extraordinaria we observe what these behaviours are and how we can help them. How to create sorority”.

Society remains deeply unequal and Fillol claims access to the same opportunities and rights “from the most absolute difference, because the difference is enriching”. According to her, one tries to lead from a feminine point of view, but the system is masculine, and this causes the clash of these two worlds, two ways of acting and seeing the world. This is why many women who access high positions do so from these male patterns that have traditionally been associated with power.

What are the keys to female leadership?

More cooperation and less competition. More teamwork and less hierarchy. More empathy, collaboration, and intuition, and less passivity, control, and impulsiveness. Many authors have described the characteristics of this leadership, and precisely this need to transform concepts that until now we associated with power: it is the first step to understand that female leadership is not only about a woman assuming a position, but a woman who wants to provide a new vision of working, communicating, and even understanding the company and its goals.

As Fillol points out, “we seek not only to create sustainable businesses economically, but also in the human sphere. Making a social impact, changing the status quo. The purpose is very clear, companies are being built from somewhere else and this is very revolutionary. The capital is not the most important thing, and the Covid-19 crisis has shown that the companies that have survived are the ones that have made an effort in activating empathy and active listening”.

Precisely this feminine vision in terms of decisive sensitivity and empathy was referred to by ECB President Christine Lagarde in 2008, when she said that “if it had been Lehman Sisters instead of Lehman Brothers, the world would look different”.

From exclusive leadership to participatory leadership

“Resilience, the ability to emerge stronger from an impact, is a characteristic of leadership”, and this is precisely the key for the leaders of the future. Move away from the image of power and possession, and link themselves to contribution and cooperation. A leadership that goes from being within the reach of a few to becoming popular: “For me, a leader is a responsible person committed to their success and the impact they want to leave in this world”.

True female leadership is what generates a positive impact, not just from senior positions, but across the board. From the bottom to the top. As Gemma Fillol concludes, “we all make an impact. Activism can be practised from as close aspects as the children’s school, the stores where you shop, or who you vote for. We should all be conscious people, question everything, and be committed to our deepest longings and the imprint we want to leave on the world. We should all be leaders”.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

Els diners formen part de la nostra vida des de ben petits. Amb les primeres monedes que posem a la guardiola, els diners que ens donen els avis per l’aniversari, la primera feina d’estiu, l’ajuda dels pares per comprar-nos els primers capricis… I de sobte, arriba la majoria d’edat i, entre molts d’altres canvis, per primera vegada tenim el control sobre els nostres diners. Però realment ens han ensenyat a gestionar-los? Serem capaços d’independitzar-nos, d’arribar a final de mes? La resposta és que, sens dubte, sí, controlar tot això està a les nostres mans, i només necessitem una mica d’organització per treure’n el màxim rendiment.

Per què necessito els diners?

El primer estereotip que hem de trencar respecte als diners és comparar-nos amb els altres. Calcular el que tenim o guanyem en funció del que té la gent del nostre entorn no és ni ser objectiu ni realista. Cadascú neix i creix dins un entorn determinat, en unes condicions sobre les quals rarament ha pogut influir. Si estàs estudiant i tot just comences a encaminar el que serà la teva vida, treu-te la pressió de sobre, perquè res està escrit, i l’important no és on comences sinó on pots arribar. Així doncs, el primer que ens cal fer és analitzar la situació actual i determinar el nostre objectiu a mitjà termini. No serà el mateix viure a casa dels pares i centrar-nos en els estudis que tenir la voluntat d’independitzar-nos, encara que per aconseguir-ho hàgim d’invertir part del nostre temps en treballar. Determinar això ens portarà a la següent pregunta: quants diners necessito per viure?

En aquest punt ja hem de començar a jugar amb les nostres finances i diferenciar les despeses fixes de les variables, tal com fan les empreses. Les fixes seran totes aquelles que tenim tant sí com no cada mes, com ara el lloguer del pis, el gimnàs, el preu de la targeta de transport o una subscripció a Spotify. En el cas de les variables, seran totes aquelles en què l’import pot variar d’un mes a l’altre en funció de les nostres necessitats. Per exemple, tot i que el menjar és imprescindible, no gastarem el mateix un mes que l’altre, i justament és un dels punts on podem retallar despesa. Amb això no ens referim a deixar de menjar o comprar els productes més econòmics del mercat, independentment de la seva qualitat. Més aviat ens referim a tot el contrari: apostar per un consum més responsable.

Com puc reduir la meva despesa mensual?

Només cal mirar l’entorn actual per veure que les tendències de consum, és a dir, el tipus de compra que fa la major part de la societat, està canviant, i cada vegada són més les persones que en comptes de comprar en grans superfícies industrialitzades busquen el producte de proximitat, més qualitat i menys quantitat. Aquests petits canvis ens permetran fer una compra amb consciència, prioritzant només els productes que necessitem i cuidant al mateix temps la nostra salut i economia. Algun exemple que podem aplicar a la nostra vida diària podria ser beure aigua en envasos reutilitzables (ampolles de vidre o metàl·liques) i evitar així la compra diària d’ampolles d’aigua, tot substituint-les per garrafes que són més econòmiques i ens duraran més temps.

El mateix podem fer a l’hora de la compra, portant la nostra bossa per evitar comprar bosses de plàstic. Un altre truc útil pot ser organitzar el nostre menú setmanal, per saber què menjarem cada dia i, per tant, què ens cal comprar. Ni més ni menys. Pel que fa a productes d’higiene, podem optar per paquets familiars, on hi ha més quantitat per menys preu, o bé alternatives com les pastilles de sabó o les copes menstruals que, més enllà de ser econòmiques, no generen residus. També existeixen botigues a granel on pots comprar només la quantitat que necessites, sigui de productes alimentaris o de neteja de la llar. Investiga la teva zona i busca l’opció que més s’adapti a la teva butxaca, recordant sempre que allò que s’ha fet sempre, o allò que fa la majoria, no sempre és la millor opció per tu.

Pel que fa al transport, també cal buscar aquest equilibri i valorar alternatives al transport privat, que suposa un cost més elevat si sumem gasolina, impostos, assegurança i reparacions. El transport públic o la bicicleta són dues opcions econòmiques que ens poden ajudar a controlar les nostres despeses al mateix temps que cuidem el medi ambient. Fins i tot en el moment de sortir de festa podem retallar despeses si actuem amb consciència. Reservar amb antelació, aprofitar ofertes i descomptes o marcar-nos la quantitat que volem gastar abans de començar la nit ens ajudarà a mantenir un cert control. Si aquesta última part és la més difícil, un truc pot ser portar en efectiu l’import que volem gastar. D’aquesta manera, no hi haurà marge de passar-nos de pressupost i això ens permetrà gestionar millor les sortides, sense gastar ni un euro més del que toca.

Controla la teva situació econòmica des del mòbil

Aquestes són algunes de les recomanacions que ens ajudaran a mantenir el control dels nostres estalvis, però la tasca important és analitzar la nostra situació particular i fer-nos les següents preguntes: de quins ingressos disposo? Quina quantitat he de destinar a despeses fixes? Què em queda per destinar a l’oci? Necessito estalviar de cara al futur?

Si una cosa tenim a favor, és que actualment existeixen aplicacions per gairebé tot. Controlar les nostres finances mai ha sigut tan fàcil. La majoria d’entitats financeres s’estan posant les piles des de fa anys perquè l’experiència del nou client digital sigui intuïtiva i àgil, de manera que en un sol clic tinguem a la nostra disposició tota la informació que desitgem, des del saldo total del compte (els diners de què disposem), fins a les despeses que hem realitzat amb la targeta, veient de manera gràfica on estem destinant la major part dels nostres diners. Això ens permetrà fer-nos una idea de la nostra situació actual i cap a on hem de dirigir els esforços futurs.

Treballar i estalviar, els dos grans aliats per tenir diners

Una eina clau per gestionar els nostres estalvis són les guardioles digitals, un espai del compte on posarem els diners que volem destinar a una activitat concreta. El funcionament n’és senzill: ens hem de proposar un objectiu, sigui un viatge o alguna cosa que volem comprar, i a partir d’aquí calculem quin import hauríem d’ingressar cada mes per aconseguir-lo. Cal buscar l’equilibri entre allò que desitgem i els nostres recursos actuals. Si volem més diners, haurem de treballar més. Si no podem treballar més, els haurem de gestionar de forma més eficient. Però, sigui quina sigui la nostra situació, prendre el control de les nostres finances i saber en tot moment què està passant al nostre compte corrent és indispensable.

L’últim consell és no perdre de vista que mai caminem sols. Tenim pares, familiars i molta gent al voltant que ens pot ajudar a entendre què significa tot allò que té a veure amb els diners, que, en definitiva, és entendre com funciona el món actual. Tenir el seu suport i seguir els seus consells serà un pilar indispensable perquè aquest primer contacte amb el món de les finances sigui clar i comprensible. Quan prenem el control dels nostres diners, estem prenent el control de la nostra vida.

11Onze és la comunitat fintech de Catalunya. Obre un compte descarregant la super app El Canut per Android o iOS. Uneix-te a la revolució!

One of the most important details when taking out home insurance is to calculate the value of the contents, that is, all the things we have at home. This will allow the insurer to compensate us in the event of a claim or theft.

A home insurance policy should include the value of the contents of the home, which includes furniture, household goods, valuables and jewellery. Calculating their value is easier than we think, as Sara Casals, junior product manager at 11Onze, explains.

The most advisable way to estimate the value of our belongings is to do it room by room, drawing up a list of all the goods and assigning a replacement value to each one of them, which is what it would cost us at the moment to buy the object on the market. We should bear in mind that the valuation of the contents will determine the price of the insurance, so it is not in our interest to value it above the real price, as this would increase the cost of the insurance.

Jewellery and valuable objects such as works of art have a special treatment and must be declared in their corresponding section. Furthermore, regarding this type of objects, “the level of cover that the insurer will offer us will be related to the security measures that we have in the home”, says Casals.

How much is what I have at home worth?

If you want to discover fair insurance for your home and for society, check 11Onze Segurs.

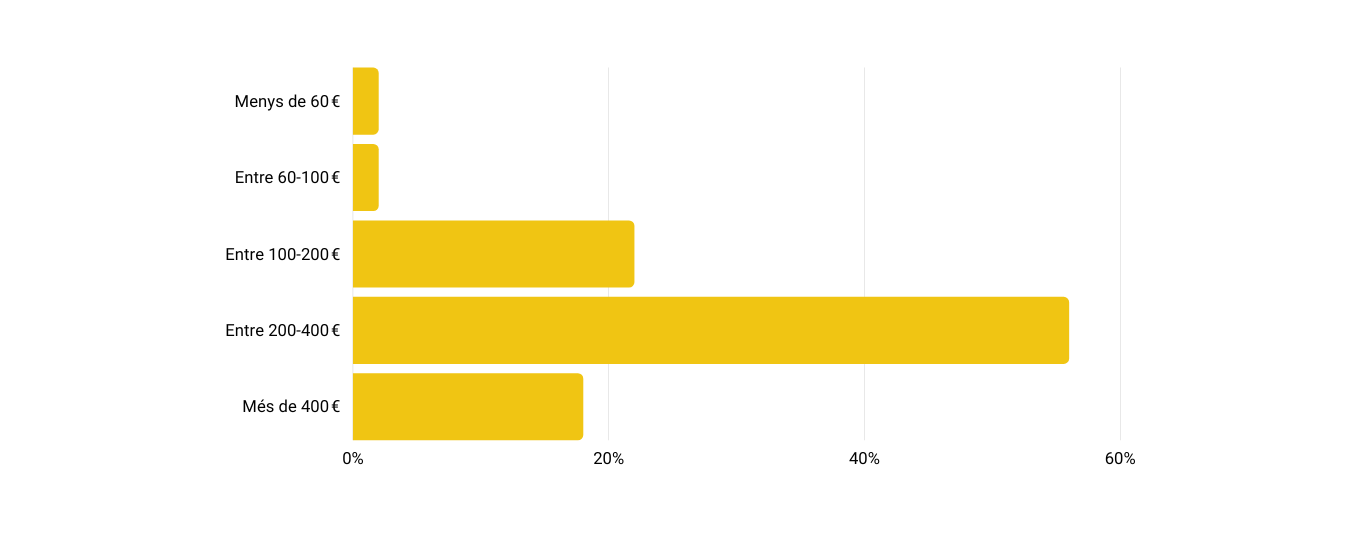

We have carried out a study of the costs of home insurance through a survey on the members of our community who are homeowners, with the aim of analysing the competitiveness of the product that we offer through 11Onze Segurs.

The survey was conducted by 11Onze through our Telegram channel with the participation of 279 users who responded to the question: “How much do you pay for your home insurance each year? They were given the option to choose from a range of prices ranging from €60 per year to more than €400.

The final data shows that 56% of users pay between €200 and €400 per year for their home insurance, while 22% spend between €100 and €200 per year. In addition, 18% pay more than €400 per year. These results are in line with the average annual price of home insurance in Spain, which is around €301 per year.

How much do you pay for your home insurance?

A more competitive alternative

At 11Onze Segurs we believe that you can reduce the cost of home insurance by optimising processes and personalising coverage. That’s why we have a completely digitalised platform, where we do away with paper contracts, physical agencies, management fees, cancellation and contract change fees, which is already a considerable saving, but we also let you modify and adapt the coverages to your needs at any time, before and after signing the contract.

In this way, we can offer you home insurance from €5 per month. Our policy is designed so that you do not pay more for your insurance, offering a monthly or annual fee, without permanence, between 15%-20% cheaper than with traditional insurers. What is the monthly cost of your current home insurance? Do you want to know how much you could save? Try our price simulator by entering some basic data, and you’ll get your no-obligation quote instantly.

If you want to discover fair insurance for your home and for society, check 11Onze Segurs.