QFS: entre la promesa i la realitat operativa

Quantum computing is no longer science fiction. Governments, banks, and large corporations are investing billions with the promise of revolutionizing industry, digital security, and also the financial system. But to what extent can it truly transform money? And what is actually true behind concepts such as the “quantum financial system”?

For decades, the financial system has advanced in parallel with the development of classical computing. Each leap in computing power has made it possible to process more information in less time, accelerating markets, making financial products more sophisticated, and exponentially multiplying the volume of available data. This progress, however, has a structural limit.

The problem is not only the amount of data, but the nature of the challenges facing modern finance. The management of systemic risk, the optimization of global portfolios with thousands of interdependent variables, real-time fraud detection, or the simulation of crisis scenarios do not grow linearly, but exponentially. Each new variable does not add complexity: it multiplies it.

In this scenario, traditional computers are forced to simplify models, accept approximations, or discard possible scenarios because calculating them all becomes computationally unfeasible. This is where the system begins to show signs of exhaustion: not because information is lacking, but because there is a lack of real capacity to understand it as a whole.

It is precisely at this point of saturation that quantum computing appears as a possible paradigm shift. Not so much to perform the same calculations faster, but to address problems that, until now, were practically unsolvable using classical computational logic.

What is quantum computing, really?

Quantum computing is not a faster version of today’s computers, but a radically different way of processing information. While classical computing is based on bits that can only take two possible states —0 or 1— quantum computing uses qubits, units of information that can exist simultaneously in multiple states thanks to the physical phenomenon of quantum superposition.

This property does not mean that a quantum computer “knows everything at once,” as is often simplistically presented, but rather that it is capable of exploring a much broader solution space in a single computational process. Instead of advancing step by step, as a conventional computer does, it can analyze multiple possible paths in parallel.

However, this advantage is not universal. Quantum computing does not replace classical computing; it complements it. It is especially powerful in problems where complexity grows explosively and where traditional methods are forced to simplify, discard variables, or assume approximations.

This is the case for:

- Complex optimizations, such as the efficient allocation of financial resources with thousands of interdependent constraints.

- Massive simulations, which make it possible to model economic or market scenarios with a number of variables that is impossible to exhaustively address with classical computers.

- Analysis of large volumes of data, especially when subtle patterns must be identified in highly noisy environments.

- Advanced cryptography, both in the potential ability to break current systems and in the development of new security mechanisms resistant to quantum attacks.

This potential explains why global financial institutions such as JPMorgan Chase, Goldman Sachs, or BBVA are already collaborating with technology companies such as IBM or Google on experimental projects. Not to reinvent money, but to understand to what extent this new computing capability can improve risk management, operational efficiency, and the security of the financial system.

Can a “quantum financial system” exist?

Alongside the real progress of quantum computing, a much more diffuse concept has gained visibility in recent years: that of the quantum financial system, or QFS. It is often presented as a future global monetary network, fully secure, decentralized, immune to corruption, and in some versions even backed by gold.

As of today, there is no operational quantum financial system, nor one in the process of being implemented. No central bank, no multilateral organization, and no top-tier financial institution has announced the creation of a new monetary architecture based on quantum technology. Nor is there any official roadmap aimed at replacing key infrastructures of the international financial system, such as SWIFT, with quantum computers.

This institutional vacuum is crucial. Monetary systems do not change due to an isolated technological innovation, but through complex political, regulatory, and geopolitical processes. Monetary history shows that technology can facilitate change —as computing did with electronic payments— but it is never the main driver. The power to issue money, regulate it, and control its flows remains in the hands of states and central banks.

This does not mean that quantum computing is irrelevant to finance. On the contrary: it can profoundly transform how risks are calculated, how data is protected, or how processes are optimized. What it will not do, however, is redefine the rules of the monetary game on its own. Thinking that a new computing capability can replace institutions, sovereignties, or power balances is to confuse a tool with a system.

In this sense, the QFS narrative responds more to the need to find technological solutions to structural problems of the financial system —distrust, opacity, or instability— than to a realistic project. Technology can improve the system, but it cannot depoliticize it.

Where it can actually transform the financial system

The real potential of quantum technology applied to finance is far less spectacular than some narratives promise, but also far more solid and plausible. It does not point to a sudden rupture of the system, but to a gradual improvement in those areas where complexity has clearly exceeded the capacity of traditional models, such as:

- Risk management and systemic stability. Current risk models often fail in extreme scenarios, as was demonstrated in 2008. The quantum ability to simulate thousands of complex scenarios could improve the detection of vulnerabilities before they turn into crises.

- Fraud prevention. With millions of transactions per second, identifying fraudulent patterns is increasingly difficult. Quantum algorithms could detect anomalies far more efficiently.

- Cryptography and security. The dark side of quantum computing is that it could break current encryption systems. This is why central banks and governments are already working on post-quantum cryptography, not to create new money, but to protect existing money.

- Efficiency in global markets. Better calculations can reduce costs, errors, and intermediaries, especially in international payments.

What quantum computing will not do

It is important to say this without ambiguity. Quantum computing can improve tools, processes, and computational capabilities, but it cannot solve problems that are not technical, but structural and political. Confusing a technological innovation with a systemic solution is a recurring mistake in times of change. For this reason, it should be kept in mind that:

- Quantum technology will not eliminate inflation, because inflation is not a computational problem, but one of monetary policy, money supply, debt, and confidence. No computer, no matter how powerful, can prevent central banks from printing money or states from mismanaging their finances.

- Nor will it guarantee political transparency. Transparency depends on rules, institutions, and democratic will, not on data-processing capacity. An opaque system can remain opaque even if it runs on the most advanced technology in the world.

- Quantum computing will not eliminate corruption, because corruption does not arise from programming errors, but from power relations, perverse incentives, and lack of oversight. History shows that technology is often neutral: it can be used both to monitor abuses and to perfect them.

- And finally, it will not automatically democratize wealth creation. Access to technology, as with all major innovations, tends to concentrate first in the hands of those who already have capital, knowledge, and influence. Without institutional changes, the gap may even widen.

In essence, money will continue to be a tool of power, regulated by states, central banks, and geopolitical interests. Quantum computing can make the system faster, more efficient, or more sophisticated, but changing the processor does not change the system. The rules of the game are not written by technology, but by politics.

Before the quantum future, a monitored digital present

The real debate is already here and is deeply digital. Central bank digital currencies are advancing as an imminent reality and raise immediate questions about privacy, control, and economic freedom. In this context, the supposed quantum financial system is relegated to a distant horizon, while the total digitalization of money —with all its political and social implications— is being deployed with little public debate.

Faced with this scenario, the role of the citizen is not to adhere to technological promises, but to understand how the monetary system really works, diversify risks, and reduce dependence on salvational narratives. History shows that, in times of experimentation and financial uncertainty, the protection of wealth tends to seek refuge in what does not depend on algorithms or issuers: real, scarce, and auditable assets. Because, in the end, technology may change the tools, but the future of money will not be magical or automatic: it will continue to be, above all, a political decision.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

The need for speed, traceability and transparency in cross-border payments expressed by corporates was one of the banking industry’s unfinished businesses. The widespread adoption of the SWIFT gpi service has transformed the cross-border payments experience.

The SWIFT bank-to-bank communication protocol, an acronym for Society for Worldwide Interbank Financial Telecommunications, is a messaging network that financial institutions use to transmit information and payment instructions globally. They do so using a secure and standardised system. Although there are alternative systems, such as the Russian SPFS or the Chinese CIPS, these are still in the minority.

Despite the popularity of the SWIFT protocol, the increasing globalisation and digitisation of international trade revealed some of the system’s shortcomings. Slowness, delays, errors, lack of transparency and high transfer fees were common customer complaints.

To address these shortcomings, SWIFT introduced the Global Payment Innovation (gpi) service in early 2017. Within the first year of its launch, 30% of international cross-border payments were sent via SWIFT gpi, and by 2020 this had risen to 70%.

SWIFT gpi

Speed, traceability and transparency

It is a protocol that adds a tracking process through a unique reference code, similar to that applied when sending or receiving a parcel by courier. It, therefore, provides a real-time view of the transfer, from sending to receiving the funds. Initially, only banks have direct access to this information, but it can be passed on to customers on request.

The ability to share this additional information with customers not only improves the customer experience but, according to SWIFT, eliminates manual intervention and saves on resource costs by reducing customer enquiries. Even so, the costs, fees and deductions applied by intermediaries are known in detail to all parties.

On the other hand, the real-time payments system – half of SWIFT’s gpi payments are paid in less than 30 minutes and all in less than 24 hours – makes it less likely that banks will ‘hold’ customer money for hours or days until it is credited to the recipient’s account, and makes it easier for a large proportion of payments to be made on the same day.

This is the key to the success and potential evolution of this technology. The rapid adoption of SWIFT gpi by financial institutions should translate into a win-win situation, providing users with direct, real-time access to gpi information without requiring a call to the bank, thus empowering the customer.

If you want your business to make a giant leap, use 11Onze Business. Our business and freelancer account is now available. Find out more!

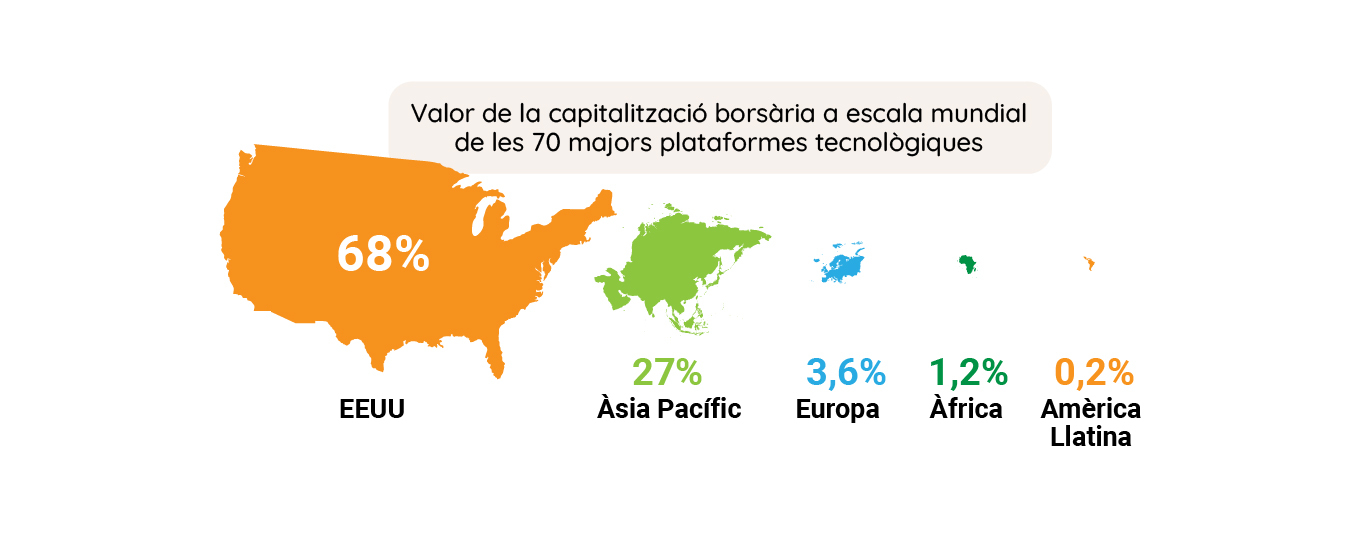

En l’àmbit de les tecnologies i la revolució digital, Europa està subordinada a les dues grans superpotències, els Estats Units i la Xina. L’última constatació ha estat la crisi dels microxips i dels semiconductors. A 11Onze analitzem com es distribueix el poder tecnològic al món i com la Unió Europea lluita per construir la seva sobirania digital. Ho aconseguirà?

Europa va surfejar tan superficialment la primera onada tecnològica que no va aconseguir contrarestar l’hegemonia dels Estats Units a internet, però ha d’aprofitar la següent. La Comissió Europea reconeix que la transformació digital d’Europa i la sobirania són una qüestió d’importància cabdal, i ha establert un pla estratègic per desenvolupar les seves pròpies capacitats i tecnologies digitals.

La nova guerra freda i les creixents tensions entre els Estats Units i la Xina són un incentiu addicional perquè Europa assoleixi una independència tecnològica si vol evitar el risc de convertir-se en un camp de batalla en la lluita per la supremacia tecnològica i industrial entre aquests dos països. La implantació de les xarxes 5G i les sancions econòmiques dels Estats Units contra la Xina, amb l’excusa de l’espionatge, en són un perfecte exemple.

Font: CIDOB. Informe sobre l’Economia Digital de les Nacions Unides, a partir de les dades d’UNCTAD i de la International Data Corporation.

La decisió unilateral de l’administració del president Trump de treure als Estats Units de l’acord nuclear amb l’Iran i implementar noves sancions econòmiques va posar de manifest la incapacitat de la Unió Europea a l’hora de mantenir una mínima sobirania geopolítica. Els tímids intents, per part dels Estats europeus, de crear un sistema de transaccions bancàries alternatiu al SWIFT, per tal d’eludir les amenaces de Washington i preservar l’acord amb l’Iran, van quedar en paper mullat.

Tanmateix, si alguna cosa hem après de la pandèmia de la Covid-19, és que la infraestructura digital ha esdevingut fonamental per al benestar social i pel funcionament de l’economia. La connectivitat digital ens ha permès mantenir una certa normalitat en l’accés de la població als serveis dels centres educatius i mèdics durant el confinament, que difícilment hauria sigut possible sense aquesta metamorfosi tecnològica.

Mantenir la competitivitat d’Europa

El mercat únic és el nucli per a fer de l’economia digital europea un líder mundial, i en aquest sentit la Comissió Europea va proposar un pla estratègic per adaptar el mateix concepte a l’àmbit digital. Un ambiciós projecte que s’ha anat ampliant al llarg dels anys i que pretén reforçar l’economia digital de la Unió Europea mitjançant la millora dels requisits de responsabilitat i seguretat de plataformes i proveïdors de serveis digitals.

En aquest sentit, aquest passat desembre, es va anunciar una inversió de 1.000 milions d’euros per donar suport al programa Connecting Europe Facility (CEF), o Mecanisme per Connectar Europa, que defineix l’àmbit d’aplicació de les mesures a les quals dona suport la Unió Europea, necessàries per a la creació d’infraestructures i projectes de connectivitat d’interès comú dels estats membres.

Les noves normes, anunciades recentment, per a la distribució de programari de codi obert són una altra mesura pensada per a fer accessible al públic el codi font dels seus programes informàtics en benefici dels serveis públics, les empreses i la ciutadania, i així esperonar la innovació.

Totes aquestes propostes i mesures busquen assegurar que la Unió Europea no només sigui líder en l’àmbit regulador, sinó que també pugui competir o mantenir un mínim de sobirania en un sector geoestratègic que cada vegada esdevé més essencial.

11Onze és la fintech comunitària de Catalunya. Obre un compte descarregant l’app El Canut per Android o iOS. Uneix-te a la revolució!

Els economistes fan previsions de cap on portarà l’economia l’automatització del treball, però si d’una cosa podem estar segurs és que la tendència no fa més que guanyar força. Analitzem els canvis que venen i com ens hi podem adaptar per assegurar el nostre futur laboral.

La tecnologia continua avançant a un ritme vertiginós i, com vam aprendre de l’última Revolució Industrial, l’automatització de processos en el món laboral comporta la destrucció de llocs treball. Segons l’estudi de Randstad ‘Flexibility at work, Abrazando el cambio’, a l’Estat espanyol el 52% dels llocs de treball actuals corre el risc d’automatitzar-se, parcialment o totalment, en la pròxima dècada. Però també poden sorgir noves oportunitats pels que saben aprofitar aquesta inevitable metamorfosi ocupacional.

L’arribada de l’anomenada Quarta Revolució Industrial ens ha d’esperonar a pensar en noves maneres d’aportar valor en el nostre lloc de treball abans que aquesta automatització o intel·ligència artificial assumeixi les nostres tasques. L’efecte final de l’automatització pot ser i ha de ser una cosa molt positiva per la gran majoria de la població. Sobretot si com a societat entenem que, mentre molts treballadors senten com una amenaça real la inseguretat econòmica, també ens permet adaptar-nos a aquesta transició i a la nova realitat tecnològica.

Eficiència i rendibilitat

Transferir les tasques de producció de mans humanes a un conjunt tecnològic optimitza la producció en massa, redueix els costos de producció i l’ús de recursos i, alhora, incrementa la rendibilitat. No només el teixit industrial augmentarà les tasques que destina a l’automatització, sinó que també se’n beneficiaran sectors tecnològics de l’administració, les finances o la logística.

I això és clau, perquè, quan parlem de pèrdua de llocs de treball, els experts afirmen que són les tasques, i no les professions en si mateixes, les que la tecnologia està automatitzant. És a dir, aquestes tecnologies no tenen per què substituir a les persones, però sí a les tasques que són menys valorades o que requereixen menys habilitats, competències o coneixements professionals.

Educació i formació continuada

La importància d’adquirir competències digitals és, òbviament, una necessitat que no podem desestimar si ens hem d’adaptar a aquest nou escenari laboral dominat per les noves tecnologies, però no podem oblidar que això implica una formació continuada i en constant actualització.

Una de les coses que hem après arran de la pandèmia de la Covid-19 és la importància de moltes professions de serveis essencials, sanitàries o de l’àmbit de l’educació, on el factor humà no és fàcilment substituïble per la tecnologia, com tampoc ho són feines que requereixen habilitats com la creativitat o la capacitat de comunicació. Aquests són sectors de l’economia que difícilment es veuran afectats d’una manera significant per l’automatització, almenys en un futur pròxim.

Resta per veure com la tecnologia, la intel·ligència artificial i l’automatització transformen l’economia en general, i, sobretot, com serà el procés d’adaptació de les generacions que no han nascut en un món digital. Però el que és segur és que l’automatització de processos i tasques que, fins fa ben poc, semblava inversemblant que no les poguéssim fer els humans, no només ja ha arribat, sinó que es quedarà per formar part del nostre dia a dia.

11Onze s’està convertint en un fenomen com a primera comunitat fintech de Catalunya. Ara, llança la primera versió d’El Canut, la super app d’11Onze, per a Android i Apple. Des d’El Canut es pot obrir el primer compte universal al territori català.

Gold’s physical properties give it great versatility in many industrial applications, such as the substantial electronic infrastructure needed to power the fast-growing artificial intelligence (AI) sector.

Throughout history, gold has been regarded as the quintessential store of value, making it an essential asset for people who want to protect their savings and investors who want to diversify their portfolios when facing economic uncertainty.

But beyond its popularity as a safe-haven asset and its use in the jewellery sector, gold’s physical properties, such as its high electrical conductivity and resistance to corrosion, make it ideal for its use in many industrial applications.

From the medicine sector where it is used in prosthetics and implantable medical devices, thanks to the fact that it is non-reactive and non-toxic, to electronics applied to the automotive and aerospace industries, an estimated 300 tonnes of gold a year is used by electronic components and 7% of the world’s gold is found in these types of devices.

AI drives demand for gold

Although demand for gold used in electronics peaked in 2010 at 328 tonnes, falling to 249 tonnes in 2023, the sector has seen a modest recovery in recent quarters and, according to a report by the World Gold Council (WGC), AI applications will bolster demand in the near term.

The adoption of AI is increasing the need for advanced technological devices that use gold. Technology companies are investing large amounts of money in creating new multimodal artificial intelligence models and algorithms that can learn, reason and make decisions autonomously after collecting and analysing data. With the expansion of AI applications in fields such as healthcare, security and finance, this trend is expected to continue.

Although as technologies evolve, some traditional uses of gold may disappear – as we are seeing the production of LED lights without gold-containing components – as companies invest in data centres, chips and specialised sensors, the demand for gold for industrial uses is expected to continue to experience steady growth, cementing it as an indispensable asset in both industry and financial markets.

To discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

The Digital Identity Regulation recently adopted by the European Parliament and the Council of the European Union gives the green light for EU citizens to have a virtual wallet linked to their identity. It will allow official documents to be stored digitally and formalities to be carried out with a high degree of security.

The European Parliament and the Council of the European Union have reached an agreement on the creation of a Digital Identity Wallet that will be legally valid and operational in any EU country. This electronic identification should make it possible for citizens to carry out transactions in public and private online services in a reliable and secure way that guarantees the protection of their personal data.

These apps will allow citizens to store and manage their identity data and official documents in digital format. Documents such as ID cards, driving licences, electronic signatures or educational certificates will be stored virtually in a mobile application, to be used directly and without the need to share data with third parties.

This would speed up many bureaucratic procedures in our country and when travelling to other EU member states. It would facilitate the process of registering as a resident, opening a bank account, taking out a loan, taking out a mortgage or paying with a digital wallet. It would also provide an alternative to the technological monopoly held by US and Chinese companies, the dominance of which is of concern to the EU and has been one of the triggers behind this initiative.

When will it be available?

By 2024, all EU member states will have to make a digital identity wallet available to all citizens who want it. This will not be an easy task considering that currently, only 14% of major public services in all EU member states allow cross-border authentication with electronic identification.

In this context, EU regulators intend to convene 140 public and private entities from 19 EU states to resolve technical, business and regulatory issues around the provision of a digital identity.

Pilot tests of four large-scale projects across 25 member states were launched on 1 April 2023, with the aim of exploring the practicality of digital identity portfolios in real-life scenarios that reach across different sectors. The aim is for at least 80% of citizens in member states to have access to an interoperable digital identity by 2030.

Data protection and the right to anonymity

The widespread implementation of a new system of digital identification of citizens may raise issues of security and anonymity. Who will have access to our data? What use can be made of this data?

In a joint statement on the new EU regulation on digital identity, scientists and researchers from 39 countries warn that “The current proposal radically expands the ability of governments to monitor both their own citizens and residents across the EU by providing them with the technical means to intercept encrypted web traffic, as well as undermining existing oversight mechanisms that European citizens rely on.

On the other hand, European authorities claim this tool will fully respect the user’s choice of whether to share personal data – independently certified – and that it will offer better protection against misuse, tracking or interception. Adding that “the revised law preserves the current well-established security norms and standards in the industry”.

With privacy as one of the main concerns surrounding the introduction of a digital euro, the adoption of new regulation on the digital identity of the citizenry potentially making it even easier for governments to monitor and mass surveillance of the population, a debate between all parties involved is not only necessary but essential.

11Onze Recommends Bitvavo, cryptocurrency trading made easy, safe and at a reasonable cost.

Una iniciativa conjunta entre el BIS Innovation Hub de Londres, el Banc d’Anglaterra (BoE) i Quant Network, obre les portes a utilitzar interfícies de programació d’aplicacions (API) per als sistemes de moneda digital dels bancs centrals (CBDC).

El Projecte Rosalind, dirigit pel BIS Innovation Hub i el Banc d’Anglaterra (BoE), ha estat explorant com adaptar interfícies de programació d’aplicacions (API) per als sistemes de moneda digital dels bancs centrals (CBDC). El projecte tenia com a finalitat desenvolupar prototips d’API per a investigar com es podien facilitar els pagaments en el comerç al detall, maximitzant la interoperabilitat entre el sector públic i privat, de manera que es fomenti l’adopció d’aquestes monedes digitals.

La iniciativa també ha servit per demostrar que les API jugaran un paper clau en possibilitar que els sistemes de CBDC ofereixin una sèrie d’avantatges en termes de funcionalitat i seguretat dels pagaments, així com per estudiar la millor manera d’establir les bases per a construir un ecosistema sòlid i pràctic. En aquest sentit, s’han desenvolupat 33 funcionalitats d’API i s’han posat en pràctica més de 30 casos d’ús de CBDC en el comerç al detall.

Si bé algunes d’aquestes funcionalitats ja són possibles amb els sistemes de pagament existents, com les targetes i l’efectiu, el Projecte Rosalind s’ha centrat en la possible “programabilitat” de les monedes digitals, establint característiques similars als contractes intel·ligents emmagatzemats en una cadena de blocs.

Col·laboració amb Quant Network

Quant Network és una empresa de tecnologia de cadena de blocs que busca aconseguir la interoperabilitat universal entre cadenes de blocs utilitzant el seu sistema operatiu Overledger US. És a dir, permetre que els usuaris d’Overledger interactuïn amb diferents cadenes de blocs simultàniament.

Amb la seva participació en el Projecte Rosalind, Quant Network ha proporcionat la infraestructura subjacent, la plataforma de cadena de blocs, els contractes intel·ligents i la interoperabilitat entre els llibres de comptabilitat dels bancs centrals. En definitiva, una solució de gestió de claus a escala de banc central per a les transaccions de blockchain.

A més, el Quant Network té una criptomoneda (QNT) dins de la cadena de blocs d’Ethereum, que es fa servir per impulsar Overledger i que es pot comprar i vendre des de les principals plataformes d’intercanvi de criptomonedes, com ara Bitvavo que 11Onze Recomana.

Un pas més a prop del “Britcoin”?

Tot i la participació del Banc del Canadà, Barclays Bank, Amazon i Mastercard, el Projecte Rosalind s’ha centrat en la possible introducció d’una CBDC del banc central del Regne Unit. En aquest sentit, el projecte ha revivat la polèmica sobre les CBDC després del rebuig públic als plans del primer ministre Rishi Sunak per introduir el “Britcoin” com una alternativa virtual als diners en efectiu, i a les declaracions de Sir Jon Cunliffe, governador del Banc d’Anglaterra, afirmant que la creació d’una moneda digital del banc central del Regne Unit “és més probable que no”.

Un grup de treball governamental ha estat estudiant la possibilitat de crear una moneda digital que pugui utilitzar-se al marge de l’efectiu i les targetes per a les transaccions quotidianes, com a part dels esforços per a digitalitzar l’economia. D’aquesta manera el departament del Tresor i el Banc d’Anglaterra examinaven la viabilitat d’una “lliura digital” per a empreses i particulars per impulsar la innovació del sector financer britànic després del Brexit.

Les conclusions del Projecte Rosalind que una CBDC podria abaratir i fer més eficients els pagaments entre particulars, al mateix temps que permetria a les empreses crear nous productes financers destinats a reduir l’activitat financera fraudulenta, es podrien entendre com un pas més a favor del llançament del “Britcoin”.

11Onze Recomana Bitvavo, les criptomonedes de manera fàcil, segura i a baix preu.

Traditional banking is likely to disappear sooner rather than later. And security tools such as biometrics and cryptography will help protect us from fraud.

The world of finance is changing fast. Fintechs are overtaking traditional financial institutions, above all because they are committed to combining technology and customer service. All with the aim that new technological advances will allow increasingly simple, but more secure, operations. We see it!

- Services in the cloud. Financial institutions will increasingly organise their services via the internet. This is why financial applications are constantly innovating: they are looking for more and more transactions to be carried out in the cloud.

- Artificial intelligence, an essential tool. This technology is much more sophisticated and has a significant influence on the internet of things, on the management of ‘big data’, on facial and optical recognition and on the ‘blockchain’, which is the structure with which the new financial institutions will work.

- Mobile finance made easier. The so-called ‘mobile banking’ system is not new. Still, it will be increasingly easier to use: it will provide greater accessibility and incorporate one-click payments from customer to customer. In addition, customer-to-business ‘digital banking’ will no longer rely on passwords.

- More blockchain. Blockchain software vendors will attract the interest of organisations that want to accelerate their performance. With blockchain, they will achieve more cost-effective operations.

- Next-generation cashpoints. It is expected that, in the not-too-distant future, we will be operating cashpoints without having to use a card, directly with our mobile phones. Some cashpoints around the world, in fact, already incorporate biometric authentication or iris recognition.

- Security, security, security. This is a constant concern for financial institutions, which will be looking to include new protection services for their customers. Biometrics will be commonly used to access financial data.

- Links between financial institutions. Experts have realised that financial institutions can reduce costs and facilitate customer services by partnering with each other. Working collectively advances innovation and establishes healthier cooperation.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

The cryptocurrency market continues to grow despite its extreme volatility. After years of speculative booms and sudden crashes, governments around the world have placed regulation at the centre of the debate. Some present it as a necessary protection for small investors; others as a strategy to protect the traditional financial system from an uncomfortable competitor.

After more than a decade of existence, cryptocurrencies have demonstrated their disruptive potential on monetary policy and state control of money. Thanks to blockchain technology, they offer a more transparent, decentralised and inflation-resistant system, as most limit the issuance of new units. However, their Achilles heel remains volatility: an obstacle that makes it difficult for tokens to serve as a stable medium of exchange.

Today, crypto assets are no longer a marginal product. They have become investment instruments, hedges against weak currencies and, in some countries, even legal tender, such as Bitcoin in El Salvador or USDT in emerging countries. However, this expansion has also opened the door to fraud, manipulation and money laundering, which has accelerated the response from regulators.

A difficult market to control

Supervising the crypto world is, quite simply, a colossal challenge. The term crypto asset encompasses thousands of projects, tokens, and protocols with very different uses: from payment systems to decentralised applications, stablecoins, and NFTs. Most operate in global environments, without clear boundaries and with anonymous or decentralised actors.

For regulators, this means monitoring a global ecosystem with no central headquarters, in which miners, developers and intermediaries often escape traditional financial regulation. While countries such as Switzerland and Japan already have specific legal frameworks in place, others, such as the United States and the European Union, are still debating what limits to impose without stifling innovation.

The European and Catalan legal framework

In Europe, the major step forward has been the approval of the MiCA (Markets in Crypto-Assets) Regulation, in force since June 2023, which establishes for the first time a single legal framework for crypto-assets within the EU. MiCA requires all service providers — exchanges, custodians or token issuers — to obtain a regulated licence and provide transparent information to customers.

In Spain, its implementation is being coordinated with the Bank of Spain and the National Securities Market Commission (CNMV). At the same time, Law 11/2021 on the prevention of tax fraud already requires platforms to report their customers’ transactions to the Tax Agency, and Royal Decree 7/2021 establishes an official register for exchange and custody service providers.

These measures pave the way, but they also raise questions: to what extent do they protect investors or reinforce state control over digital money?

Risks for small investors

Despite their growing popularity, cryptocurrencies remain a high-risk investment. Market volatility, technological complexity and a lack of transparency in some projects have led to millions in losses. In addition, many platforms operate from tax havens or jurisdictions without legal safeguards, making it difficult to protect users from scams or loss of access to digital wallets.

Classifying cryptocurrencies as investment products subject to consumer protection rules — as proposed by the CNMV — could provide greater security. But it could also limit access and the decentralised nature that has made the crypto world a laboratory for financial freedom.

Disparate regulations and side effects

The International Monetary Fund (IMF) warns that regulatory priorities differ from country to country: while some emphasise investor protection, others focus on the integrity of the financial system. China, for example, has directly banned mining and cryptocurrency transactions, while countries such as Singapore and the United Arab Emirates seek to attract capital with favourable regulations.

These differences lead to what experts call regulatory arbitrage: companies and platforms migrating to where laws are more lax, while maintaining a global reach thanks to the Internet. The result? Unequal competition and a constant risk of global technological relocation.

Towards a global framework?

Faced with this fragmentation, the IMF, and the Bank for International Settlements (BIS) are calling for coordinated global regulation that guarantees legal certainty without stifling innovation. The aim is to establish clear limits and common standards to prevent abuse, but without undermining the open and decentralised nature of blockchain technology.

However, many experts warn that overly strict regulation could turn cryptocurrencies into an extension of the financial system they sought to challenge, transforming a tool for economic freedom into yet another instrument of monetary surveillance and control.

Between control and freedom

The big question is whether regulation will serve to empower citizens or limit their financial sovereignty. At a time when central banks are preparing their own digital currencies (CBDCs), the line between protection and control is thinner than ever.

Cryptocurrencies were created to challenge a system that concentrates the power of money. Regulating them can bring security and confidence, but it can also erase their original spirit. As always, the key is not whether it is necessary to regulate them, but how: with criteria of transparency and accountability, or with the desire to control what cannot be stopped.

11Onze Recommends Bitvavo, cryptocurrency trading made easy, safe and at a reasonable cost.

L’accés a Internet i la digitalització dels serveis ens faciliten moltes tasques quotidianes que abans requerien una presència física. La contrapartida d’aquesta revolució tecnològica és el perill de ser víctima de la ciberdelinqüència. Et presentem algunes males pràctiques que hauries d’evitar per a protegir-te contra el frau a la Xarxa.

No donar importància a les contrasenyes

Una mala gestió de les contrasenyes pot facilitar molt la feina als delinqüents informàtics. Tot i això, molta gent no els hi dona gaire importància i fa sevir claus molt senzilles per accedir a serveis tan importants com la banca en línia. És important emprar contrasenyes robustes de més de vuit caràcters que continguin una combinació de majúscules, minúscules, números i caràcters especials. A més, cal evitar fer servir la mateixa contrasenya per accedir a diferents serveis i activar l’autenticació en dos factors quan sigui possible. Un gestor de contrasenyes ens ajudarà a administrar i a recordar totes les claus.

Fer servir una xarxa de Wi-Fi pública

Les connexions de Wi-Fi públiques no sempre estan xifrades adequadament, per tant, les dades enviades i rebudes poden estar desprotegides. Si no pots evitar fer-les servir, assegura’t de tenir instal·lat una VPN (Virtual Private Network) en el teu dispositiu, una xarxa privada virtual que t’ajudarà a encriptar les teves comunicacions.

Ignorar les actualitzacions del sistema

Les actualitzacions de seguretat dels nostres dispositius i aplicacions poden ser inconvenients, però són essencials per evitar que els ciberdelinqüents aprofitin les vulnerabilitats dels sistemes per accedir als nostres dispositius i robar les nostres dades personals. Mantenir tots els dispositius actualitzats amb les últimes versions de programari ens protegirà contra les últimes vulnerabilitats conegudes.

Fer clic a qualsevol enllaç

Clicar en enllaços sospitosos pot instal·lar programari maliciós en el teu dispositiu o portar-te a pàgines de phishing dissenyades per enganyar-te i obtenir la teva informació personal o credencials d’inici de sessió. Aquestes pàgines poden semblar autèntiques, però en realitat són falses i tenen la intenció de robar la teva informació. Evita proporcionar informació personal, com ara números de compte bancari o contrasenyes a través de correus electrònics. Una empresa legítima mai et demanarà informació personal o contrasenyes per correu electrònic o missatge de text.

No fer còpies de seguretat regularment

Molts dispositius fan còpies de seguretat al núvol automàticament. Això és important perquè pots arribar a perdre o no tenir accés a la teva informació i arxius per motius diversos: infeccions del sistema, programaris maliciosos, pèrdua del dispositiu… Tanmateix, per mandra o per la falta de capacitat de memòria en els dispositius, sovint no fem les còpies de seguretat necessàries. Esborrar arxius innecessaris o fer servir una memòria externa ens pot ajudar a assegurar que sempre tenim una còpia de la nostra informació més important.

Si vols conèixer una assegurança justa per a la teva llar i per a la societat, descobreix 11Onze Segurs.