The impact of the pandemic on Catalan companies

The Covid-19 pandemic has done great harm to Catalan companies. To top it off, the ones that have suffered the most have been the smaller companies. Those that have not had to close have suffered a significant drop in sales and, in many cases, have been forced to include workers in an ERTO or even sack them. This first quarter of 2021, however, shows a certain recovery in economic activity.

According to Idescat, on January 1, 2020 a total of 637,772 companies were established in Catalonia (excluding agricultural production, fishing, and domestic services).

If we consider only the criterion of number of employees, the sum of self-employed (companies without employees), microenterprises (less than 10 workers), and small businesses (less than 50 workers) is 629,332, more than 98% of the entire Catalan business sector. In fact, the sum of self-employed and microenterprises only exceeds 94% of the total in Catalonia.

The smaller the company, the more it has suffered

The size of companies has turned out to be strongly related to their degree of vulnerability to the economic and social crisis resulting from the pandemic.

At the end of February this year, the Bank of Spain Survey on Business Activity (EBAE) read that small businesses were the ones that suffered most from the effects of the crisis during 2020, as they lost, on average, 19% of their turnover, whereas big businesses only lost 12.4%.

The drop in sales softened as the size of the company grew. This same trend has been observed in effective employment – once the ERTO (layoffs) have been deducted.

All sectors have been more or less affected

In Catalonia, 74% of GDP corresponds to the services sector, an economic activity strongly dependent on tourism. Thus, the president of the Guild of Restorers of Barcelona, Roger Pallarols -without precise data yet-, believes that in Catalonia the proportion of businesses that have closed to never reopen can reach 25%.

Other sectors, such as trade and industry, have also suffered a significant impact. According to the survey by PIMEC, Evolution of the Catalan industrial SME in 2020 and prospects for 2021, 54% of Catalan industrial SMEs have closed the year of COVID-19 with results below those achieved in 2019. Up to 29% have destroyed employment, whereas only 22% have increased their workforce.

This strong relationship between the “health” of companies and employment levels ends up having a direct impact on the well-being of people.

Prospects: a glimmer of hope

These first months of 2021, however, are beginning to send us a message of hope.

According to data from the Department of Business and Labour of the Generalitat de Catalunya in its Bulletin of the labour situation and productive sectors. 1st term 2021, in the 1st quarter of 2021 there is a remarkable recovery of economic activity and this is reflected in the evolution of the labour market. The month of May 2021 shows a -3.1% drop in unemployment. The number of people affiliated to Social Security has risen in +1.1% compared to the previous month, and recruitment has grown by 11%.

Another reason for hope can be found in the first Scanner Startups Ecosystem, organised by Barcelona Tech City and Closa Investment Bankers, based on operations closed in 2020. It states that last year the Spanish technological companies almost got to €2,100 million in financing, an increase of 4.3% -despite the fact that Spain’s GDP fell by 11% due to the impact of Covid-19- and that in the first four months of 2021 the sector has already raised nearly €1,800 million, almost as much as in the whole of last year. 41% of respondents say they have increased their workforce in the last year, compared to 31% which has reduced it. The survey reaffirms that Barcelona is the focus of investment in emerging companies in Spain.

Another positive fact is that the digitisation of companies – which until the pandemic could be more or less optional – has become almost mandatory. M. Rosa Agustí, president of the Girona Association of Businesswomen (AGE), explains: “The pandemic has caused 90% of Girona’s companies run by women to be digitised and sold via the Internet.”

If you want your business to make a giant leap, use 11Onze Business. Our business and freelancer account is now available. Find out more!

Catalonia is one of the regions of the “Four Motors for Europe” network, founded in the late 1980s to promote cooperation between them. It is made up of four of the most industrialised areas of the European Union.

On 9 September 1988, Auvergne-Rhône-Alpes, Baden-Württemberg, Catalonia and Lombardy signed a cooperation agreement to form the “Four Motors for Europe” network. As Sandra Molas, sales manager at 11Onze, explains, these four regions currently comprise “36 million inhabitants” and represent approximately “9% of the European economy”.

The initial objectives of this interregional cooperation partnership were mainly related to economics and research, as well as art and culture. Over the following decades, however, the objectives and level of cooperation have increased significantly.

Current areas of cooperation include economic development, research and innovation, training and higher education, climate and environment, transport and mobility, health, agriculture, civil society and arts.

Sandra Molas talks about the "Four Motors for Europe".

In the framework of European integration

The founding of the network coincided with major European integration processes. For example, as Sandra Molas recalls, in 1992 the Maastricht Treaty was signed, which “came into force in November 1993” and led to the creation of the European Union.

The Four Motors for Europe has always supported the important role played by the regions in the continent and has served as an example of the strong international affiliation of European regions.

“The group actively contributes to European affairs, in particular by publishing common positions on EU policy,” as Molas explains. In fact, they try to “act as a lobby on the issues that are of most interest to them.”

In some cases, regions join as partners to participate in initiatives, especially in economic cooperation. This has been the case in Flanders, Wales and Quebec. However, most activities involve only the four signatory territories.

Flexibility is one of the defining characteristics of the network, which has no institutions or budget of its own. The partnership is governed by a Coordination Committee made up of the general coordinators of the executive offices of the presidents. And the thematic work is carried out in various working groups.

Rotating presidency

The presidency changes every year following a fixed rotation. Catalonia assumed its last presidency in September 2020 and passed the baton to Auvergne-Rhône-Alpes in December 2021.

The programme of the Catalan presidency focused on the 17 Sustainable Development Goals of the 2030 Agenda, as well as the European Green Pact, to strengthen the transformative resilience of our societies. Inspired by the three dimensions of the 2030 Agenda, the programme was organised into three resilience dimensions: economic, social and environmental.

To give the programme substance, all departments of the Government of Catalonia were consulted, resulting in more than 30 specific initiatives that were developed over the 14 months of the Catalan presidency.

Present and future of the network

As Sandra Molas warns, the ravages of the pandemic and the current economic situation mean that the four regions that make up the group must “read just their recovery policies and activities” towards new models that “adapt to the needs of the moment.” And this will have to be done “with a regional, European, but also global vision.”

The 11Onze sales manager concludes that this will not be easy because of “the threat of an impending global crisis caused by national debt, rampant inflation and skyrocketing fossil mineral prices”.

If you want your business to make a giant leap, use 11Onze Business. Our business and freelancer account is now available. Find out more!

Despite Brexit, the City of London remains one of the world’s most important financial centres, accounting for a third of global financial transactions, and the world’s capital of the foreign exchange market.

The City of London, also known as the ‘Square Mile’ because of its one-square-mile size, is a separate borough within the City of London or ‘Greater London’. It is roughly the area of the original walled city, called ‘Londinium’ during the Roman occupation, and where its surrounding areas grew to become incorporated into the general term of London.

Although under the jurisdiction of Greater London, the City has a special status with its own mayor and independent police force. Despite the City having only 10,000 residents – 12.3% of whom have non-domiciled status to avoid paying UK tax – 400,000 commuters and over 10 million tourists a year.

London

More than 500 banking institutions have headquarters or offices in the city, and it is estimated that they directly employ more than 550,000 financial sector workers, accounting for one in five financial services jobs in Britain, generating almost 80 billion euros in annual revenue.

The importance of having access to this financial district has not diminished with Brexit, keeping the UK as the world’s most global financial centre that continues to attract talent, business and investment. That’s why 11Onze Business offers you a UK IBAN, so that your business has a foot in the City.

If you want your business to make a giant leap, use 11Onze Business. Our business and freelancer account is now available. Find out more!

If you liked this article, we recommend you read:

11Onze

11Onze11Onze Business is now in the testing phase

2 min readThe first available IBAN is from the UK and, for the first two

Why is it a good time to buy gold? How can we do it? Is there a certain fetishism in having gold bars and coins at home? All this and more is answered by the Financial Director of 11Onze, Oriol Tafanell, in a new episode of Territori 17.

“When we talk about gold, it is better to talk about buying than investing. Some people invest in gold as an asset on the stock market, but we refer to the fact of buying it, of making it tangible, of being able to touch it. Gold is bought precisely because it is a physical material,” Tafanell clarifies at the start of the conversation. And he explains why it is a good idea to buy it in an inflationary context such as the one we are living in.

Tafanell confirms that it is a good time to buy gold, because “the financial market is very, very shaken.” “There is no data that leads us to believe that the economic context will improve. Gold is normally described as a safe haven because it protects us from the adverse economic cycle,” the Financial Director summarises. In short, in gold we can protect our money, because it does not participate in the changes and instability of the market.

La Plaça – Territori 17: The golden refuge

A tangible safe haven: breaking clichés

At this point, some fetishist clichés about gold bullion and gold coins need to be dismantled. “It should be borne in mind that gold bullion is often minimal in number of grams. Of course, there are gold bars of 12.4 kilos, but they are worth a fortune and are only available to the big banks and fortunes,” Tafanell illustrates. A bar of 12.4 kilos, says the CFO, is worth approximately 650,000 euros. The price of gold, Tafanell explains, is marked in ounces and, today, the price of one ounce of gold, which is 33 grams, is close to 1,700 euros.

Keeping gold at home is only one of the options that Preciosos 11Onze allows. It is also possible to buy gold and leave it in vaults under the custody of a specialised company. “At 11Onze we offer the possibility of buying gold starting at 3,000 euros, and at the time the purchase is made we will know exactly how many grams it amounts to. As we will place an order collectively, we will be able to do so at a better price,” Tafanell summarises.

The custody of the gold, at home or under the supervision of a specialised company, will be for at least a year and, after that period, the person can decide whether to continue to keep it or sell it. “Today it is unthinkable that in a year’s time gold will not make any capital gain. Historically, gold has never lost value. In the last three years it has risen by 40%, the CFO concludes. Because the beauty of gold is precisely its stability.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

The stock prices of the leading fintechs specialising in deferred payments, BNPL (Buy Now, Pay Later), have experienced historic declines. Concerns about a continued slowdown are growing as consumers cut back on spending in the face of rising prices and the likelihood of a recession, which, together with new players entering the market, will test this business model.

Valued at up to $50 billion and with more than 13 million customers, San Francisco-based Affirm is a leader among companies that rely on the deferred payment method to attract, sell to and retain customers, who can get instalment loans when they buy products online.

As has been seen with many other technology companies, the loss-making nature of this fintech was not an impediment to investors giving it a market capitalisation of billions of dollars after its IPO in 2021. Even so, the lack of profitability and shares that are on a downward trajectory – they have lost 60% over the last year – are just one example of a trend extended to other companies in the sector, which calls into question the future of this business model.

As Isaac Sène, product manager at 11Onze, explains, “the BNPL business is a risky model with negative interest rates, much of the risk is caused by the credit granted by the current players, which could be considered ‘subprime’. With potential interest rate hikes in the coming months, the business model as it stands today is challenged, and the repayment of the debt even more so.

“The entry of consolidated companies with large capital reserves and brand weight like Apple, can be a lethal competition for current BNPL startups like Klarna.”

Banks and tech giants want a slice of the pie

The digital revolution and the maturity of e-commerce spurred the rise of alternative payment methods to those offered by traditional banks. New generations of digital natives wanted more agility, lower fees, and a fully online experience.

Fractional payment shopping via e-commerce platforms was the logical evolution of a trend that was already established in large physical retail outlets. Demand for this type of service exploded during the confinement caused by the health crisis, when a time of economic stability was coupled with consumers who were bored at home, and could only shop online.

Still, it was only a matter of time before traditional banking and financially well-resourced technology giants, such as Apple, took advantage of the popularity of their platforms and large customer bases to integrate their own instalment payment applications, capturing much of the market that had previously been the preserve of BNPLs. “The entry of established companies with large capital reserves and brand weight, such as Apple, can be lethal competition for existing BNPL startups such as Klarna,” notes Sène.

Unregulated financing and uncontrolled indebtedness

Young people and low-income households are the most vulnerable to the risks associated with the use of these services, especially because of the danger of accumulating excessive debt. The ease of lending and the lack of checking credit profiles before granting loans can lead many families into over-indebtedness.

The sector is therefore facing a possible upturn in non-performing loans. The lack of diversification of companies dedicated exclusively to the BNPL model means that they often serve consumers with lower credit scores. A potential increase in defaults, coupled with declining demand due to consumer fear of a new crisis, generates a lack of confidence among investors that is evident in falling share prices.

Increasing policy and regulatory pressure from governments, coupled with consumers with increasingly tight budgets, point to diminishing returns from a business model based on impulse and impulse purchases. The sector could consolidate with more diversified companies that combine B2C with B2B – less prone to the volatility of ephemeral consumerism – or that understand the service of instalment payments only as an added value to their business.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

If you liked this article, we recommend you read:

Finances

FinancesBuy Now, Pay Later

5 min readThere are applications on the market that allow you to pay, by instalment, online purchases and

Spain has only executed a third of the European funds destined for the recovery of the economy, making it the country in the European Union that has returned the most funds. We publish an excellent article from VIA Empresa, where David Garrofé analyses the state of European funds allocation.

Most people think that Spain is a net recipient of European funds, the reality is that it has gone from being a recipient state of solidarity funds of some 8 billion euros to being a net contributor of more than 5 billion.

Next Generation: Recovery fund? No, a return fund

The poor management of European investments by the state is making the possibility of a transformation of the Spanish economic model a distant prospect.

David Garrofé – Entrepreneur

Something is not being done right when, despite the fact that most people think that Spain is a net recipient of European funds, the reality is that it has gone from being a recipient of solidarity funds to the tune of 8 billion euros to being a net contributor of more than 5 billion in the last operational period from 2014 to 2020. The mystery? Well, Spain has only spent 35% of the funds approved by Brussels and has failed to execute 65% of the available funds, as acknowledged in September 2020. In fact, Spain is the country that returns the most funds in the EU. Totally nonsensical, considering the high official unemployment rates and the endemic backwardness in both public and private investment in innovation.

If we want to find out the causes, I think they are quite obvious, and at the same time sad: convoluted legal and operational frameworks, highly bureaucratised and too complex to manage for most mortals. It is also necessary to add to the European complexity that of our administrations, which also place an extra layer of unnecessary requirements with a level of control by the intervention bodies that also scares the public administrators. It is quite clear that the growing distrust of the public and the desire of civil servants to protect themselves has necrotised a large part of the public administration. To top it all off, apart from the territorial areas recognised as Objective 1 zones because of their low economic development, the rest of the territories, with Catalonia at the forefront, can only access 50% of the co-financing of the programmes.

With this historical panorama of defaults and refunds, let us now add the famous and long-awaited EU-designed Next Generation recovery funds

I could tell a lot of anecdotes about autonomous communities and some ministries that directly give up presenting projects due to a lack of ideas or, even worse, due to laziness and/or lack of knowledge when it comes to managing them. Literally, the saying “don’t go there”, but instead of referring to politics, we are talking about the essential levers for the development of our economy and collective well-being.

With this historical panorama of non-compliances and refunds, let us now add the famous and long-awaited recovery or Next Generation funds designed by the EU so that Europe can make a leap forward in the field of innovation, sustainability and digitalisation and stop losing positions to China and the USA in the context of the COVID pandemic. We are talking about an initial 141 billion for Spain alone, of which some 70 billion would be in the form of credit, to be implemented over 4 years. Now, we said to ourselves, Europe is reacting and wants to do it quickly and well, as it did with the Marshall Plan in 1947. Well, the reality is very different, it is not being done quickly or well, and I will explain myself below.

Initially, reading the Next Generation programme’s explanatory statement, it seemed clear that these funds were to be focused on programmes to transform regional economies, with a strong role for companies to motivate them to collaborate with each other and with research and innovation organisations. It was also proclaimed that they would be launched imminently at the beginning of 2020 and that the criteria for action would be in place in time and form. The reality has been different. Dozens of consultancy firms, basically based in Madrid and with good personal and professional connections with politicians and technicians in the central administration, were the only way to obtain precious knowledge of how to access the funds. The greater the confusion, the higher the turnover, they dared to say in private. This functional mess also affected Catalonia, and the Catalan government created CORECO, a selection committee for strategic projects that would end up presenting all Catalan projects in a single package. This was a good initiative to encourage companies to identify collaborative projects with an impact and where more than 542 very interesting projects were presented, involving thousands of companies that had to mobilise some 42,000 million euros. Of these, the Catalan government on 2 February 2021, seeing that the Ministry of Industry wanted to select a few but very large ones called PERTE, opted to select, reduce and compact all those it had received to leave only 27. It was therefore necessary to wait until the criteria for the state calls were clear before presenting them to Madrid.

The first big warning to sailors: the Secretary General of Industry, Raúl Blanco, the following day, on 3 February 2021, made a public statement saying that the package presented by the Generalitat was “politicised” and therefore disqualifying all the work done by many entrepreneurs, universities and research centres. The message was clear. The Sánchez government would not leave this economic cornucopia in the hands of the autonomous communities, nor would it allow itself to lose the political benefits of its distribution. The Next Generation programme would be 90% centralised and would leave the territories to decide on a meagre 10%. However, as the capillarity of these was essential to reach companies and achieve the expenditure expected by Brussels, it guaranteed ERC that it would “territorialise” 50% of the funds in exchange for the approval of the general state budgets. The reality is that the central government designs and validates the calls for proposals according to its own criteria, and Catalonia has to hire more than 400 technicians to manage the paperwork and justification of this 50%. While the other 40% of the funds go to projects the Ministry sees fit. Drinking the Kool-Aid.

The money-making machine is running amok and still, someone blames our inflation mainly on Russia. And there are none so blind as those who do not want to see

On 26 May 2022, Brussels, after receiving many complaints from different organisations, employers’ associations and autonomous communities, and seeing the evolution of the few calls for proposals and the limited budget available for Next Generation, demands that the Spanish government actively involve the territories in designing policies and programmes. At the same time, seeing that the Spanish economic recovery is smaller and slower than expected, it increases the 141,000 million euros to 22,000 million more. The money-making machine is running amok and still, someone blames mainly Russia for our inflation. And there are none so blind as those who do not want to see.

The Minister of Economic Affairs Nadia Calviño on 19 July 2022, under great pressure from Brussels and having received an economic addendum that she does not know how to spend, opened up to the autonomous communities the possibility of presenting their own projects, of which Catalonia has presented more than 2,000 million euros, without having received any response to date.

Everything suggests that we are facing a new Plan E of President Zapatero, who in 2009 dedicated himself to generating public spending, without any sense, to stimulate the economy. An example of this is the call on 28 May 2021 aimed at local councils to renovate housing and change public lighting. These are clear examples of innovative and transformative objectives for our economy.

You don’t have to be a prophet to see how the party will end: an accumulation of returns of classic European funds to which the Next Generation funds will be added, with little impact on the country’s GDP growth, as the Bank of Spain and the Airef are now showing, and with an imperceptible transformation of our economic model. Just look at what the Treasury did in August 2021 by ceasing to publish data on the transfer of the fund’s resources to companies. No transparency for fear of criticism and political discredit. I advise anyone who likes to follow this issue not to hesitate to go and look for the good monitoring reports on the application of the resources that the CEOE is doing in its observatory, where it states that the current level of execution is 25%. No comment.

If we in this country talked less about budgets and more about accountability, we probably wouldn’t have so many problems

Some readers might reproach me for denouncing the actions of others without making proposals for amendments, but as it would not cost much to do so, at least minimally better, I will end this article with three concrete, swift and impactful proposals

- To truly and urgently territorialise the funds. Catalonia has major projects and the capacity to implement them.

- Use fiscal policy and allow tax deductions for companies that carry out innovative and transformative projects. It would be faster, more efficient and less bureaucratic. Countries such as France, Denmark and Italy are already doing this.

- Do not use the funds as a tool for electoral politics, using them for purposes improper to their original design. Necessary actions in the social sphere must be financed by the PGE or the European funds expressly foreseen.

If we, in this country, talked less about budgets and more about accountability and, accordingly, kept an eye on our rulers and their policies, we would probably not suffer so much from these problems.

You can read the original article here

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

Valuing a flat or a house correctly is essential to determine the price of the property, but first, we must be clear about the purpose of the valuation since the value of the property can differ greatly between the market value, cadastral value and the reconstruction value. We explain the differences.

Determining the value of a property, whether it is a house, flat or garage, can be necessary for various reasons. Whether we want to finance the purchase of a house, take out insurance, or know what taxes we will have to pay to the Treasury or the Town Hall, we will have to certify the value of the property. Even so, in each of these cases, the valuation of the property will be specific to the use made of the valuation.

Below we explain the types of valuations there are, and the factors to take into account when valuing a property:

Selling or buying a property

If you are considering selling or buying a property, it is essential that you actively participate in the valuation, and do not leave everything in the hands of the real estate agent. On the other hand, the heterogeneity of the real estate market makes it impossible to obtain a unified register that clearly reflects the sale and purchase, especially if we are referring to the second-hand market, therefore, there is no reliable data that can be used at a generalised level.

A valuation done by an approved professional guarantees, both to the buyer and the seller, that what is being asked for this property is within the market value at the time of the valuation. This is important because the value of the property can change significantly in a few months and may not be in line with the price that was being asked for the property when it was put up for sale.

Likewise, if we are buyers and require financing through a mortgage, the financial entity must ensure, through a real estate appraisal carried out by an approved appraiser, the real market value of the property in order to guarantee that, in the event of non-payment, it will be able to cover the debt. The cost of the appraisal is borne by the client regardless of whether the loan is formalised, and will also serve to establish the maximum percentage that the bank will be able to finance.

The cadastral value of the property

The cadastral value is an administrative value that is given to each property based on the data that appears in the real estate register, depending on the valuation criteria chosen by each local council. It is a fixed amount, but is updated in accordance with the annual coefficients approved by the General State Budget Law.

On the basis of the cadastral value, the amount of different municipal taxes is established, such as personal income tax, property tax, wealth tax and transfer tax, etc. This has a direct impact when calculating the amount we have to pay for the municipal capital gains tax, which calculates the increase in value of a property, if we want to sell the property. And when selling our property, we have to bear in mind that, as a general rule, the sale price can never be lower than the price reflected in the land registry.

If you want to know the cadastral value of a property, you can request this information from the electronic headquarters of the Register, from the Register Office, or by phoning your local Register office. However, the scope of the data that can be consulted will depend on whether you are the owner of the property.

Value of the cost of reconstruction

Making an estimate of the value of your property is an essential requirement if you want to take out a home insurance policy, but in this case, the value of the property is not equivalent to its market price. The insurance companies calculate the price of the policy according to the amount of money necessary to rebuild the property, in case of loss or total destruction.

Keep in mind that the Estimated Reconstruction Value (ECR) includes only the physical structure of the building, but does not include the land or contents, such as furniture or appliances. Even so, it is important to make sure that the amount of the coverage of the home is equal to the estimated reconstruction cost, to avoid having to add the difference out of your pocket in the event of a claim.

If you want to discover fair insurance for your home and for society, check 11Onze Segurs.

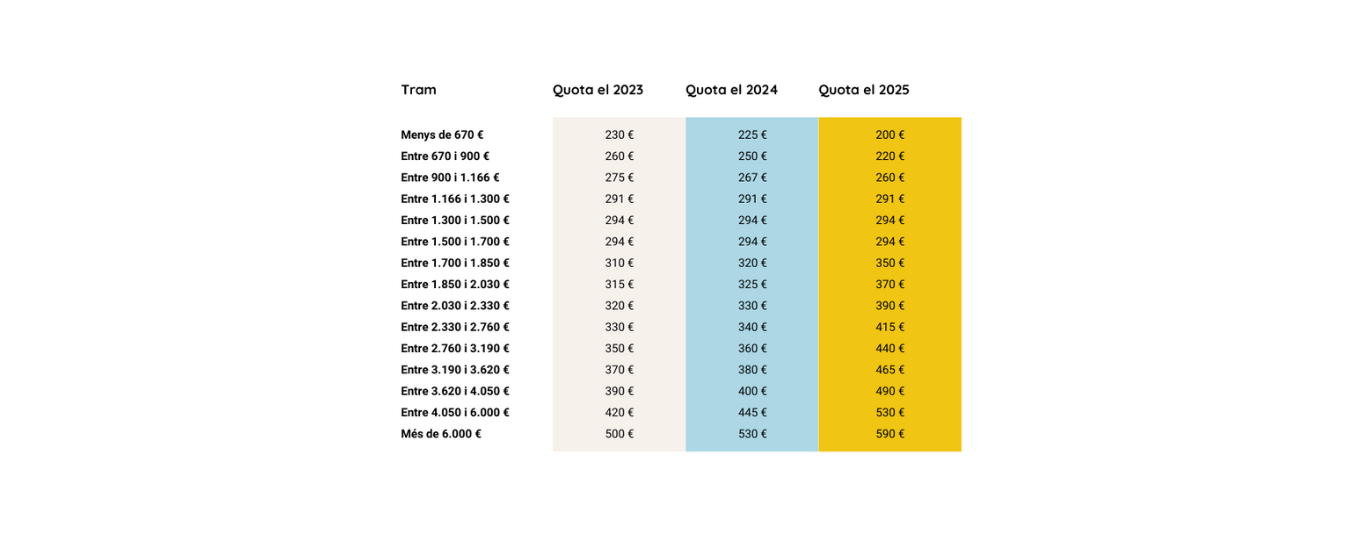

From 2023, the minimum fixed contribution of 294 euros for the self-employed will give way to a progressive system of 13 tranches depending on earnings, whose quotas will vary each year until 2025. This has been agreed between the Spanish Government and the main self-employed associations ATA, UPTA and UATAE.

The self-employed contribution in 2023 in Spain will range from 230 to 500 euros, depending on the annual income of each self-employed person. The range will be extended in the following two years. The biggest beneficiaries of the reform will be the self-employed with the lowest incomes.

The agreement envisages that the self-employed who earn less than 670 euros per month will pay 230 euros per month in 2023, which will save them 767 euros a year; 225 euros in 2024, which will save them 827 euros; and 200 euros in 2025, which will save them 1,127 euros.

The self-employed with earnings of more than 6,000 euros per month, the ones with the highest contribution, are at the opposite end of the table. In this case, the contribution will be 500 euros a month in 2023, 530 euros in 2024 and 590 euros in 2025.

Source: Ministerio de Inclusión.

A simple calculation

To determine the contribution, the self-employed must calculate the net annual income, subtracting deductible expenses from net income, and then add the Social Security contribution and subtract 7%, which is the estimated percentage for expenses that are impossible to justify. From there, divide it by the 12 months of the year to check the amount to be paid to the social security authorities. The amount may be modified up to six times a year depending on the evolution of income.

The reform of the self-employed quota was one of the commitments made by the Spanish government to receive the next tranche of Next Generation funds and still has to go through the parliamentary process. With the new Special Regime for Self-Employed Workers, self-employed workers will now pay contributions on the basis of what they earn, just like salaried workers.

The self-employed associations have welcomed the change from a system with a minimum contribution of 294 euros, which until now could be increased voluntarily to improve benefits, to this progressive system, which establishes contributions according to net income. Currently, nine out of ten self-employed currently pay the minimum contribution.

One of the few drawbacks of the new system is that it could encourage the underground economy, as some self-employed workers could hide part of their income in order not to jump from one bracket to another.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

Digital Banking is a term that refers to the digitisation of all traditional activities and services of analogue banking, which in the past were only accessible to customers when they moved to a branch. A process of change that has been going on for years, but which has accelerated enormously in recent years, mainly due to the generational change that the market is undergoing.

Every year the millennial generation is achieving higher levels of consumption of financial products, and today they are already the generation that consumes the most. Therefore, the market has had to adapt progressively to the differentiated needs and preferences of millennials, who demand agility, speed and accessibility. The achievement of this digitalization process is creating new opportunities for financial institutions and, above all, for society, allowing to directly reach people living in all kinds of different realities and situations.

Digital banking and online banking: are they the same?

As a starting point, there is a fundamental difference between the terms digital banking and online banking that should be distinguished. Online banking refers to the evolution that many traditional financial institutions have made towards the online world: it is a digitisation process that focuses on offering online certain basic services and products from their catalogue, such as money transfers or the basic management of current accounts. For other matters, however, it is still necessary to go to the branch.

Digital banking, on the other hand, refers to the intention of offering all the activities and services of traditional banking, but transferring them to the digital environment in order to reach the consumer directly, reducing intermediaries to a minimum and streamlining the entire process. Thus, apart from being able to make transfers or control the movements of our account, we can also apply for a loan or apply for a mortgage without having to go to the bank offices.

Customer experience in digital transformation.

The transition from analogue to digital banking

In the beginning, banking was entirely analogue. It offered such basic services as transfers, management of current accounts, checks and promissory notes, credit or debit cards, cash withdrawals and deposits, loans and mortgages. It was, however, necessary to go to the branch to carry out most of the transactions.

Later, especially from the 2000s onwards, new ways of managing financial transactions without having to go to a bank branch in person began to appear: online banking was born. This gradually allowed greater use of online commerce, although at that time it was still somewhat rudimentary, and had not yet become fully popular among the general population. It was at this time that payment methods such as PayPal were born, in response to a new consumer need that had not existed until then: being able to securely pay an unknown trader for an online product.

In 2010, however, the unexpected success of the first iPhone and smartphone models pushed society towards a new innovation: mobile banking. The currently well-known applications or apps began to be designed by traditional banks, with the aim of being able to have access to the banking services of our lifelong bank from the palm of the hand. This new technological revolution also allowed the appearance of contactless payments, making life easier for millions of people.

Finally, the massive use and popularization in broad segments of society, not only in millennials and young people but in the vast majority of adults and older people, has recently led to the creation and popularization of digital banking, with the most visible face being neobanks. Thus, with these new Fintech and applications that have nothing to do with those of the past, you can navigate and request any of the traditional financial services quickly and intuitively, reducing information barriers for consumers.

The rise of neobanks

In recent years, neobanks have led the digitization of financial services, taking full advantage of their digital capabilities: leveraging online platforms and data analytics to generate social interaction, providing cards instantly, offering personalized information and assistance to customers, etc.

At the beginning, they were aimed primarily at a digital native audience, such as generation Z and millennials, but little by little they have been attracting many other more diverse segments of the population and from different fields. This has been thanks to two main factors. Firstly, the cost reduction they have been able to offer in their services thanks to the lack of offices, as opposed to traditional banking, which has to pay very high rents and usually suffers from many cost overruns.

On the other hand, it is also due to the effect that the Covid-19 pandemic has had on many older consumers, as they have wanted to find a way to be able to continue carrying out their usual financial activities without having to leave home, and it is precisely in this area where neobanks have a comparative advantage over other financial institutions, since they move like fish in water in the digital area and have much more experience.

Direct banking: reaching the whole society

The popularization of these digital services has led to the emergence of the concept of direct banking: the possibility and the will to reach all customers, wherever they are and whatever their segment. New products and services can be offered to specific customer segments without suffering from geographical limitations. It is possible to reach consumers of different educational levels, of different economic incomes, personalized attention can be given to millions of people who otherwise would have no one to turn to, or to whom the traditional entities might not serve in the desired way due to physical limitations.

It is, in short, in an increasingly fast and interconnected world where the combination of current technology with new preferences for agility and accessibility allows neobanks and digital banking to put customers at the center.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

The Spanish government has finally approved the reform of the National Security Law, but the great power granted to the public authorities to deal with very ill-defined crisis situations raises serious concerns about how it could affect our fundamental rights. Miriam Frias, financial assistant at 11Onze, analyses the news.

Officially, the National Security Law of 2015 aims to ensure that the State can have the strategic resources necessary to deal with crisis situations, risks and threats that affect national security. The new text does not affect the essential content of the law, even so, it centralises more competences and specifies some actions to be carried out in crisis situations to guarantee that in such scenarios the country will have the basic resources.

The concept is nothing new, and both Spain and other countries have laws designed to guarantee critical resources, urging business and state collaboration, during a context of extreme crisis, as we suffered during the Covid-19 pandemic. Even so, and as Miriam Frias explains, “modifications have been made that have not reached the public and are still an unknown quantity“.

National Security Act.

The balance between rights and duties

The ambiguity and lack of specificity of the text allow for an overly broad legal interpretation that generates mistrust among the population. “It is an ace up the government’s sleeve that it can use when it deems necessary,” says Frias. This means that the state “could force any person of legal age to perform personal services and to comply with orders given by the authorities”.

The reform of the law has also set off alarm bells among businesses concerned that the state could seize their assets, stop their activity or even occupy them temporarily. As Frias explains, “businesses and legal entities would also have to provide personal or material services. The state would have the right to confiscate, requisition or expropriate all kinds of assets”.

After the experience of the abuse and scope in the application of article 155, it is worrying, to say the least, that a national security law, which a priori has to be more effective and quicker in its application than this article of the Constitution, does not guarantee that there will be no abuse of authority by representatives of the executive branch of the state. “We hope that these situations and examples will never materialise, but it is important to be aware of them, because nothing is impossible,” Frias concludes.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.