11Onze Recommends: Monthly Return, 22% in 2 years

We continue to expand the savings options for the community. After the good reception of Litigation Funding, the same provider proposes Monthly Return, how to make your savings generate an income every month.

A few months ago, 11Onze Recommends offered a savings product from a British provider, Litigation Funding. With an initial contribution of 10,000 euros, you could earn 9% at the end of the contract, i.e. 1 or 2 years depending on the case and the amount.

Since then, the community has demanded a product that would provide a monthly income from savings and, for this reason, we have worked on a new product exclusively for the 11Onze community. This is Monthly Return, designed for large savers and companies that contribute a minimum of 100,000 euros. Customers will see their savings grow by 22.5% over the duration of the contract (24 months). However, it is important to bear in mind that the monthly income begins to arrive after the seventh month.

*Taxes will have to be levied on the income. Income starts after the sixth month.

Farhaan Mir, 11Onze’s Chief Financial Officer, says: “We listened to our community and tried to bring in what fits their needs. People had asked for monthly returns, so we talked to our supplier to get them on board”.

In this sense, the 11Onze Recommends slogan will have to be updated. Until now, we used to say If it doesn’t exist, we create it. If it exists, 11Onze Recommends. In this case, 11Onze has asked for this exclusive product to be created for our community.

There is no other product that offers these returns, combining security and liquidity.

So, in a context where banking remunerates savings very poorly and where inflation continues to depreciate money, Monthly Return is shaping up as an excellent option for those who want to make their savings profitable. And the returns are very high, 22.5% accumulated in 2 years is a figure unparalleled in the market. According to Mir, “As far as I know, there is no other product that offers these returns, combining security and liquidity”. All this while remembering that the initial capital is covered by insurance, so it is a low-risk product.

How is it possible?

For more information about Monthly Return you can visit the 11Onze Recommends webpage and if you are interested, you can contact the provider. To receive all the information you need to complete the self-certification as a qualified investor. It should be noted that completing the self-certification does not commit you to carry out the operation, as explained in this article.

Savings for all pockets

With this new 11Onze Recommends product, 11Onze offers saving products for all budgets. From 3,000 euros you can participate in Gold Seed or Gold Patrimony, from 10,000 euros with Litigation Funding and now Monthly Return is aimed at savers and businesses with capital from 100,000 euros. As we at 11Onze have been warning for some time, all to avoid losing purchasing power in a context of inflation that has become structural.

If you want to find out how to get returns on your savings with a social justice product, 11Onze recommends Litigation Funding.

Households have drawn on savings and consumer loans to go on holiday and offset inflation, while banks have made short-term loans as expensive as credit cards.

Households’ financial situation has improved, with a gradual recovery of the purchasing power progressive recovery of lost purchasing power since 2021. Even so, more and more families are taking out quick loans to go on holiday or to finance fixed monthly expenses. The increase in consumption and the rise in prices due to inflation are eroding the savings accumulated by households during the pandemic.

The Bank of Spain’s (BdE) report on data from the end of July shows that financing through consumer loans has increased significantly between June and July. Specifically, it has increased by 2,000 million euros, reaching an all-time high not seen since 2009.

In this context, the banking sector expects that the end of the summer will lead many families to request more financing, among other things, due to the return to school, colleges and universities, further boosting the consumer loan business. And all this despite the fact that this type of financing has become significantly more expensive in recent months.

Banks continue to make consumer loans more expensive

The contractionary monetary policy applied in recent months by banks aims to reduce inflationary pressures in the economy. This translates into higher mortgages and credit to companies, but also affects credit to households, which are affected by the rise in interest rates on consumer loans.

Despite the sharp fall in mortgage lending – between January and June 2023, 14% fewer home loans were signed than in the same period last year – banks have granted loans worth 15,289 million euros in the first half of the year, making consumer loans the golden goose of the credit business.

The Association of Financial Users, Asufin, warned that consumer loans are not slowing down and are becoming more expensive in Spain with an average increase in interest rates that exceeded 13% in July. This type of financing has become much more expensive in recent months, reaching an average interest rate on short-term loans of 17.42% in August. However, the popularity of consumer loans is following a similar trend to that of the past, also due to high inflation.

If you want to find out how to get returns on your savings with a social justice product, 11Onze recommends Litigation Funding.

What are futures trading and what are the advantages and disadvantages for buyers and sellers in a context of inflation? We explain how futures market operations work, a type of trading that was already in use in Ancient Egypt.

In the financial sector, a futures transaction is nothing more than “a purchase and sale that will take place in the future, but for which we agree the price today”, as Mireia Cano, 11Onze’s head of agents, explains. Ancient civilisations such as the Egyptians and the Romans already used this type of agreement to buy raw materials or agricultural products before the harvest. Today, many types of products, from commodities to currencies, can be bought and sold on futures markets.

Futures transactions are traded in an organised and controlled market. To minimise the risk of the transaction, the two parties “provide a deposit that commits them to carry out the transaction, or to assume the penalty otherwise,” according to Cano.

In financial terms, the selling party is said to have a short position and the buying party a long position. The agreement between the two parties must specify the asset, i.e. the product or commodity being traded; the quantity of this asset; the price and the way in which the contract will be settled; the place and conditions of delivery, as well as the maturity date of the operation.

Pay now, buy later

The benefits of futures trading

Obviously, the market price of the agreed product can go up or down between the moment we formalise the operation with a closed price and the maturity date. Depending on the evolution of prices, it may be the buyer or the seller who benefits financially from the transaction. “Therefore, forward purchases are a question of time and risk,” says Mireia Cano.

In any case, both parties benefit from this type of operation in the sense that they are protected against market volatility and are guaranteed a purchase or sale that is necessary for them. These certainties are especially important for individuals or companies that buy or sell a large volume of products, as prices can change a lot, especially in such an inflationary context.

Another point in favour of buyers is that the execution cost, i.e. the margin they negotiate and advance to the seller at the trading stage, is usually low and fairly standardised, except when the underlying asset is highly volatile. In addition, the futures market offers “great liquidity because, as it operates on a daily basis, there are many facilities for placing orders every day and quite quickly,” explains the 11Onze’s head of agents.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

One of the advantages that many clients find in certain fintechs is the freedom to choose IBAN, which allows diversifying risks and deciding which Central Bank you want to supervise your accounts. In a controversial decision, Revolut has announced to its users in Spain that they will not be able to continue using the Lithuanian IBAN as before and that they will have to switch to the Spanish IBAN.

Revolut is an English-based neobank, driven by Russian managers and offering accounts with Lithuanian IBANs. But on May 9, 2023, the BOE announced the registration of the entity in the Registry of Credit Institutions of the Bank of Spain. This means that they can start offering accounts with Spanish IBANs, which will be under the supervision of the Bank of Spain. Two and a half months later, Revolut has got down to business.

The entity has sent a message to its users in Spain advising them that they will have to change their account in the Spanish IBAN or close it. They are therefore not given the option of keeping the Lithuanian account. A few years ago, another reference entity, N26, also began to offer the Spanish IBAN but, in this case, they allowed users who wished to keep their German IBAN.

Revolut no, take it or leave it. Either you accept the Spanish IBAN or close the account. This can be a problem for many people, because IBAN diversity is a way to diversify risks in terms of savings. The measure does not mean, in a practical way, any tangible improvement for users because Revolut has confirmed that depositors’ funds will be guaranteed not by the guarantee fund of the Bank of Spain but by the Central Bank of Lithuania, which is where the parent bank is based. The only possible point in favor is avoiding IBAN discrimination, that is, that in Spain you cannot domicile payments with an IBAN from another country, something controversial because it contravenes SEPA regulations and can be denounced.

The advantages of the Bulgarian IBAN

For this reason, it is expected that some users will look for new options to transfer their savings to accounts with an IBAN that is not Spanish. In this sense, 11Onze offers IBAN of Bulgaria, mainly due to its solvency and because it allows normal operations in the SEPA area. From El Canut de 11Onze you can make instant transfers, manage various accounts of other entities, request debit cards and access all the services and content offered by La Plaça. From the purchase of gold to insurance, through information and training content. Everything can be done from El Canut.

Cryptocurrencies come to La Plaça from the hand of the leading exchange house in the Netherlands. An easy and secure proposal with a €20 gift for 11Onze people to start getting into the world of the crypto-economy.

Cryptocurrencies are a very interesting alternative to regulated currencies, whether they are the current fiat currencies or the CBDCs that several countries are starting to implement. They are primarily a space for freedom in the digital world. And, despite often trying to fuel the idea that anonymity facilitates criminality, cryptocurrencies are much more traceable than physical money. They are, therefore, becoming a real and attractive alternative as a store of value and as a digital currency.

Bitvavo in La Plaça

You can already find all the information about Bitvavo at 11Onze Recommends. It is an exchange house registered with the Central Bank of the Netherlands and offers an easy and intuitive platform. There are more than 190 currencies available and the process is very simple: register on the platform via the 11Onze Recommends link.

“Our goal is that everyone can access cryptocurrencies,” explains Oriol Blanch, affiliate manager for the Spanish and French markets at Bitvavo. Oriol acknowledges that young people are more interested in crypto economics, but that they have tried to make the platform accessible to everyone. “My parents use it,” Oriol confirms. However, no one hides the volatility of cryptocurrencies.

At a time when the sector is maturing, there are cases of coins that gain a lot of value very quickly, but which are not really solid. In this sense, Oriol recommends being informed and buying reliable cryptocurrencies: “Bitcoin, because it is the first and because of the way it is mined, and Ethereum, because of what it provides with smart contracts, are probably the most reliable. For the rest, you have to be informed and look at what is behind them”.

Online exchange house

Bitvavo allows you to exchange euros for any other digital currency. And it is cybercrime-proof because users’ money is kept in “cold wallets”. “This means,” Oriol explains, “that what you deposit is stored in a physical device that is disconnected from the network. Therefore, in the event of an attack by cybercriminals, Bitvavo could restore the deposits. Moreover, in the event that a user is impersonated and funds are lost, being registered with the Dutch Central Bank offers access to the Deposit Guarantee Fund, so that up to €100,000 could be recovered. It represents a very safe option in an environment that sometimes creates a sense of insecurity for users.

Will cryptocurrencies end up being a substitute for current currencies? We asked Oriol Blanch and he is convinced that “they will be a very important alternative”. They will be if users want them to be. An alternative to the central banks’ digital currencies (CBDC), which will make it possible to monitor and manipulate the economy according to the interests of regulators. “Cryptocurrencies and CBDCs will coexist,” says Blanch, “because there is no doubt that states will force us to use CBDCs and they have the power to do so. But there will also be cryptocurrencies. We will have to see how regulation progresses”.

In the meantime, you can find out more about cryptocurrencies and Bitvavo at 11Onze Recommends and by listening to this conversation with Bitvavo’s representative in our country.

11Onze Recommends Bitvavo, cryptocurrency trading made easy, safe and at a good value.

The Spanish state will create a new body to manage complaints between customers and providers of all kinds of financial products that will be financed by the entities in proportion to the complaints received.

The law was approved on 18 May 2023 by the Plenary of the Congreso de los Diputados with 186 votes in favour from PSOE, Unidas Podemos, ERC, PDeCat, Ciudadanos, PNB, EH, Bildu and Más País, 47 votes against from Vox and 95 abstentions from PP and Junts. The legislative initiative was referred to the Senate and is awaiting final approval.

The new supervisory authority will centralise the complaints services of the Banco de España, the Comisión Nacional del Mercado de Valores (CNMV) and the Dirección General de Seguros y Fondos de Pensiones, with the aim of “resolving complaints against breaches of the rules of conduct, good practices and financial uses or the abusive nature of contractual clauses”.

This new ombudsman for financial clients includes in its protective function “users of the entities and operators of the so-called Fintech sector, as well as the provision of crypto-asset services, in the terms envisaged in the future Regulation of the European Parliament and of the Council on Crypto-asset Markets”.

To prevent financial exclusion, the regulation guarantees basic bank accounts and offers special protection not only to the elderly but also to other vulnerable groups such as migrants or the disabled. In this sense, when complaints do not have a financial content, the body will be able to impose compensations in favour of customers for amounts between 100 and 2,000 euros.

Decisions will be binding

Citizens’ complaints will be free of charge and will have to be resolved within a maximum of three months, but, unlike the current regulation, the decisions of the supervisory authority in cases of conduct and abusive clauses will be binding, provided that the amounts involved are less than 20,000 euros. These decisions may be appealed before the civil courts, although the filing of a lawsuit will not have suspensive effects.

As until now, affected citizens will have to present their claim to the financial institution’s customer services department in the first instance, and if this is not favourably dealt with, they can turn to the “Autoridad de Defensa del Cliente Financiero”, which “may agree to return the amounts unduly charged by the financial institution, plus the legal interest”.

The new body will also be able to impose sanctions of between €500,000 and €2 million for non-compliance with binding resolutions. It will also be able to impose fines of up to €1 million on the directors of financial institutions responsible for the most serious cases of misconduct. These measures should help to prevent financial institutions from continuing to abuse the system to delay payments in favourable cases.

Financial entities will bear the cost of claims

The 250 euro fee per complaint that was intended to finance the new authority was finally not approved during the negotiations. Even so, claims will be free of charge and 40% of the cost of running the institution will be distributed proportionally according to the number of complaints from each institution, while the remaining 60% will be distributed proportionally according to the number of favourable rulings for complainants from each institution, thus penalising those with the worst results.

Even so, customers who make repeated complaints to banks within a year and without grounds may be fined if bad faith in making the complaints is observed. They will be fined between 50 and 250 euros, or up to 1,000 euros if there is a repeat offence. These fines can be appealed through administrative channels or in the courts.

The new fees and penalties should help to reduce bad practices by financial entities and prevent disputes between these companies and their customers from being as unbalanced as they are now. That said, it remains to be seen whether this funding will be sufficient to provide this body with the necessary means to fulfil its purpose and whether the amount of the fines will be sufficiently dissuasive to change the bad habits that characterise the banking sector.

Fund lawsuits against banks. Do justice and get returns on your savings above inflation thanks to the compensation the banks will have to pay. All the information about Litigation Funding can be found at 11Onze Recommends.

What is the size of the gold market, what are the keys to the supply of this precious metal, and how is demand for it evolving? Discover the key elements of a growing market.

Gold is not the most expensive precious metal in the world, a privilege that belongs to rhodium, but mankind has used it for centuries as a currency and a store of value. It is estimated that over 200,000 tonnes of gold have been mined throughout history. Although that sounds like a huge amount, all that gold can practically fit into three Olympic-sized swimming pools.

Despite the relative scarcity, the rate of mining has greatly intensified in recent decades, with two-thirds of the total mined since 1950. Today, the pace of mining production is adding about 3,500 tonnes of gold each year to the total, according to the World Gold Council, an annual increase in reserves of about 2 per cent.

Three-quarters of the gold supply comes from mines scattered across most of the world. No single country accounts for 10% of world production, which helps to reduce price volatility relative to other commodities such as lithium, where production is much more concentrated. In addition, the recycling of gold from jewellery and technological devices, which accounts for a quarter of the supply, also helps to stabilise prices in times of high demand.

Twelve trillion in gold

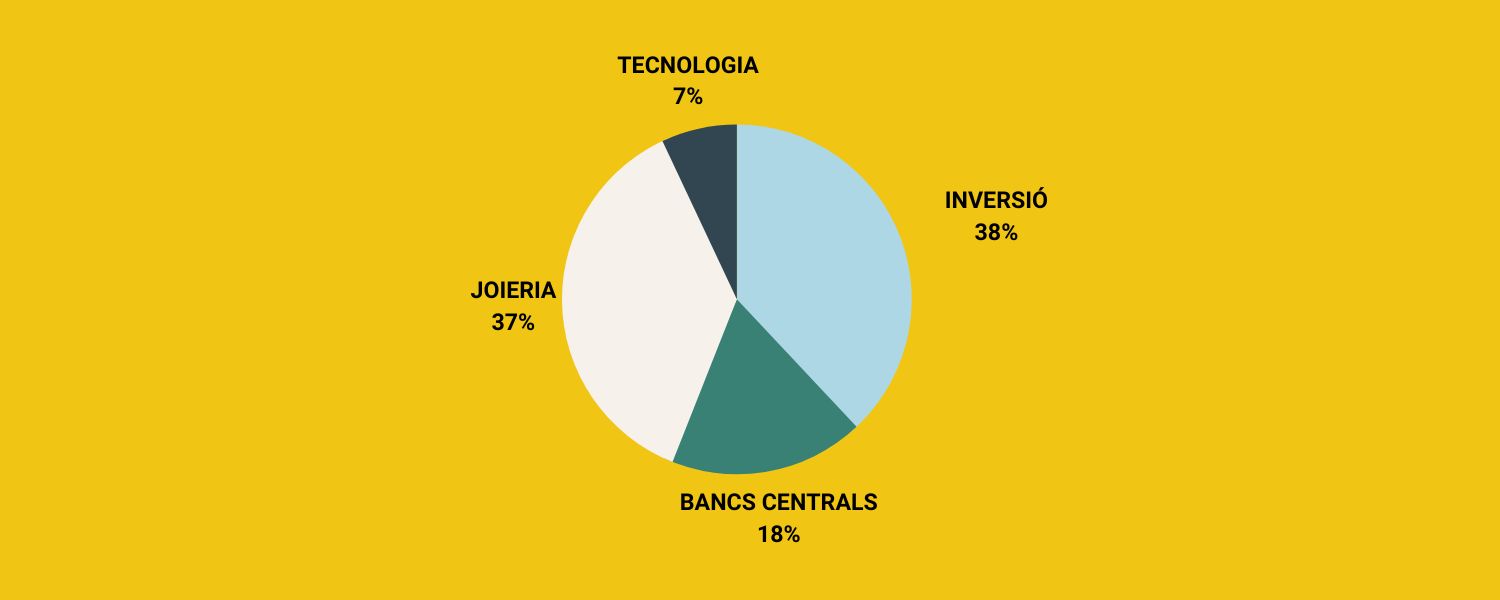

Of all the gold on the market, valued at around 12 trillion, around half (46%) has been used in jewellery, two-fifths have ended up in the financial system, either in central bank deposits (17%), in the form of investment bullion and coins (21%) or as ETFs backed by physical gold (2%), and the rest is split between industrial and other secondary uses.

However, the shape of demand has changed significantly in recent years. The main destination of gold today is already investment (38%), followed by jewellery (37%), central bank reserves (18%) and technological devices (7%).

DEMAND FOR GOLD | Source: World Gold Council

Emerging countries, led by China and India, already account for about 75% of the annual global demand for gold, while developed countries account for the rest.

The sheer size of the financial gold market, at close to five trillion euros, gives it considerable stability. Even large purchases and sales by central banks and institutional investors do not tend to have a major impact on price movements.

Central banks’ voracity

Central bank reserve managers are tasked with investing large sums of money in financial assets. And although the investment strategies of each of them are nuanced, they all follow the principles of safety, liquidity and profitability, qualities associated with gold.

This is why this precious metal has been one of the traditional reserve assets for central banks. According to the IMF, by the end of 2022 these institutions would hold more than 35,000 tonnes of gold. The approximate value of all this gold is 2 trillion euros, making it the third most important asset for central banks, after their dollar and euro reserves.

The demand for gold by these institutions has intensified since 2010. However, the weight of gold reserves in their portfolios varies considerably among them. In the case of developed countries’ central banks, gold is estimated to account for 21% of their assets, while in emerging countries it is only equivalent to 10%.

One per cent of global financial assets

Despite the voracity of central banks in the gold market in recent years, their gold reserves remain smaller than those held by investors in the form of bullion, coins and ETFs, which are worth $3 trillion.

On average, gold is estimated to account for just over 1% of global investment portfolios, although the World Gold Council has concluded that investors could benefit enormously from a share of between 2% and 10%, depending on their profile.

It should not be forgotten that, in addition to security, one of the great virtues of gold is its liquidity, which has nothing to envy to that of other major assets. As an example, suffice it to say that in the last five years the average daily volume of gold transactions has almost reached 150 billion euros, a figure higher than that of the Dow Jones Industrial Average.

Protecting savings with physical gold has been one of 11Onze’s main contributions to its community, and now the range of products is expanding. This is why, in the face of volatility, still high inflation and the growing crisis of confidence in the banking system, gold is once again strengthening its position as a safe-haven asset. Discover Gold Seed at Preciosos 11Onze.

The bailout deal following UBS’s purchase of Credit Suisse has caught AT1 bondholders by surprise and thrown a bond market worth 275 billion euros into turmoil. The Swiss bank’s subprime bonds, which had a face value of around 16 billion euros, are now worth exactly zero euros.

Investors in AT1 bonds have panicked after the Swiss Financial Markets Supervisory Authority (FINMA) announced that UBS’s purchase of Credit Suisse will result in a full redemption of the face value of all debt of this type of bond, also known as contingent convertible bonds or CoCos.

These AT1 bonds were introduced after the 2008 financial crisis and were intended to reduce the likelihood that, in the event of a bank failure, the taxpayer would have to pay for the bailout. They are essentially high-risk bonds that are converted into equity if a bank falls below a certain capitalisation limit, offsetting losses.

The announcement by the Swiss National Bank (SNB) that UBS would buy Credit Suisse for 3.01 billion euros, less than half of what the bank was worth at the last stock market close, represented a significant devaluation in the value of the shares. The surprise, however, was that with the purchase and rescue agreement, AT1 bonds were written down to zero, losing their nominal value of some 16 billion euros.

Alarm bells rang among investors in the AT1 market

Predictably, the nervousness among holders of AT1 bonds of other banks has become apparent in the face of the possibility of losing their investments in the event of a bank collapse. This puts a 275 billion euro AT1 bond market in jeopardy and is expected to force banks to raise the risk premium on these investment products.

The president of the European Central Bank (ECB), Christine Lagarde, sought to reassure investors who see an increased risk of large losses as part of any bailout, saying that “Switzerland does not set standards in Europe” in terms of conditions for bailing out banks.

It should be borne in mind that in Spain alone, large banks hold some 22 billion euros in contingent convertible bonds, CoCos. These are mainly distributed among the assets of Banco Santander (7,811 million), CaixaBanc (5,000 million), BBVA (5,000 million) and Banco Sabadell (1,750 million). It remains to be seen whether the high market volatility, marked by the banks’ liquidity problems that have grabbed the headlines in recent days, will be exacerbated by the support measures adopted to minimise its consequences.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Swift, the leading interbank messaging protocol for cross-border payments, has successfully completed the first phase of pilot testing for interoperability with CBDC. The successful outcome of the tests paves the way for the development of a beta version of the system.

Globally, most central banks and commercial banks in more than 100 countries are exploring the use of digital currencies issued by central banks. In order to maximise the benefits, CBDCs need to be able to interact within the international payment system, with each other and with existing fiat currencies.

In this context, in October 2022, Swift stated that it had developed a protocol for CBDC to move through systems based on blockchain technology and interact with fiat currencies. A technological breakthrough that would facilitate and streamline international transactions and cross-border payments, beyond traditional systems.

The recent press release announcing the successful testing of interoperability between the global interbank messaging cooperative and digital currencies is an important step towards achieving the goal of digital assets interacting with their traditional counterparts seamlessly, through a payment solution that delivers value to customers and financial institutions.

Accelerating large-scale implementation

The first phase of pilot testing lasted 12 weeks and involved 18 central and commercial banks, including the central banks of France, Germany and Singapore, as well as BNP Paribas, HSBC and UBS, among others.

Tom Zschac, Chief Innovation Officer at Swift, noted that “almost 5,000 transactions were successfully simulated between two different blockchain networks and with existing fiat currency-based payment systems“, and that “many of the participating banks have made clear their desire for continued cooperation on interoperability”.

In collaboration with another group including Cite, Clearstream, Northern Trust and SETL, it was also demonstrated how this same infrastructure can be used to interconnect multiple tokenisation platforms with different types of cash payments, simulating transfers in the secondary bond market.

The next step will be to develop a beta version for the second phase of testing to demonstrate new use cases and other practical applications and functionalities, such as securities settlement or trade finance, across different platforms of the more than 11,500 financial institutions that are part of the Swift ecosystem.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

The fall of Silicon Valley Bank and the fear of the bankruptcy of Credit Suisse caused a stock market crash in Spanish banks. Banco Sabadell once again led the sharp falls in the Ibex-35, dropping 10.49% at the close of trading on Wednesday.

Credit Suisse shares jumped 40% at the opening of trading on Thursday 16 March, a record high, after the Swiss National Bank (SNB) pledged funding of up to 57 billion euros to bolster its liquidity amid the banking crisis. Credit Suisse chief executive Ulrich Koerner defends the bank’s health and says his bank’s liquidity base is very strong.

The Spanish stock market was quick to react and opened with gains of 1.92%, in a day that will remain pending what happens with Credit Suisse and the meeting of the European Central Bank (ECB), which is expected to raise interest rates by 50 basis points.

A day to forget on the Ibex-35

Yesterday, however, the banking sector spurred the red numbers of the Ibex-35 caused by the collapse of Silicon Valley Bank and Signature Bank and the fear of the bankruptcy of Credit Suisse. The Swiss financial institution recorded declines of more than 20% after the refusal of Saudi National Bank, its main shareholder, to provide more capital.

Banco Sabadell once again led the stock market plunge with a fall of 10.49%, more than 500 million euros of its capitalisation. The bank led by César González-Bueno was also the bank with the biggest losses after plunging 11.41% on the announcement of the Californian bank’s defeat.

A day marked by losses that were replicated in the other financial institutions: BBVA (-7.38%) was behind Banco Sabadell, followed by Bankinter (-6.94%), Banco Santander (-6.89%), CaixaBank (-6.72%) and Unicaja Banco (-5.33%). Santander and BBVA are the institutions with the least liquidity drawer in both the short and long term.

Guaranteeing customer deposits

The ECB has begun consultations with the main European banks to find out their exposure to Credit Suisse. The aim is to prevent systemic bankruptcy. In the case of Spanish banks, citizens have almost one trillion euros in deposits, while the Guarantee Fund could barely cover 1% of this amount.

For this reason, many of Silicon Valley Bank’s savers transferred their money to financial institutions with an EMI (Electronic Money Institution) operating licence, which cannot use their depositors’ money to cover the institution’s expenses and are regulated by each country’s central bank.

Moreover, these entities cannot offer or promote risky investments, so they may be safer than banks, especially investment banks. Simply because they are not in the business of borrowing and gambling on the stock and credit markets, a business which, as we have seen repeatedly, can be extremely risky.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.