Student finances: how to manage money

Els diners formen part de la nostra vida des de ben petits. Amb les primeres monedes que posem a la guardiola, els diners que ens donen els avis per l’aniversari, la primera feina d’estiu, l’ajuda dels pares per comprar-nos els primers capricis… I de sobte, arriba la majoria d’edat i, entre molts d’altres canvis, per primera vegada tenim el control sobre els nostres diners. Però realment ens han ensenyat a gestionar-los? Serem capaços d’independitzar-nos, d’arribar a final de mes? La resposta és que, sens dubte, sí, controlar tot això està a les nostres mans, i només necessitem una mica d’organització per treure’n el màxim rendiment.

Per què necessito els diners?

El primer estereotip que hem de trencar respecte als diners és comparar-nos amb els altres. Calcular el que tenim o guanyem en funció del que té la gent del nostre entorn no és ni ser objectiu ni realista. Cadascú neix i creix dins un entorn determinat, en unes condicions sobre les quals rarament ha pogut influir. Si estàs estudiant i tot just comences a encaminar el que serà la teva vida, treu-te la pressió de sobre, perquè res està escrit, i l’important no és on comences sinó on pots arribar. Així doncs, el primer que ens cal fer és analitzar la situació actual i determinar el nostre objectiu a mitjà termini. No serà el mateix viure a casa dels pares i centrar-nos en els estudis que tenir la voluntat d’independitzar-nos, encara que per aconseguir-ho hàgim d’invertir part del nostre temps en treballar. Determinar això ens portarà a la següent pregunta: quants diners necessito per viure?

En aquest punt ja hem de començar a jugar amb les nostres finances i diferenciar les despeses fixes de les variables, tal com fan les empreses. Les fixes seran totes aquelles que tenim tant sí com no cada mes, com ara el lloguer del pis, el gimnàs, el preu de la targeta de transport o una subscripció a Spotify. En el cas de les variables, seran totes aquelles en què l’import pot variar d’un mes a l’altre en funció de les nostres necessitats. Per exemple, tot i que el menjar és imprescindible, no gastarem el mateix un mes que l’altre, i justament és un dels punts on podem retallar despesa. Amb això no ens referim a deixar de menjar o comprar els productes més econòmics del mercat, independentment de la seva qualitat. Més aviat ens referim a tot el contrari: apostar per un consum més responsable.

Com puc reduir la meva despesa mensual?

Només cal mirar l’entorn actual per veure que les tendències de consum, és a dir, el tipus de compra que fa la major part de la societat, està canviant, i cada vegada són més les persones que en comptes de comprar en grans superfícies industrialitzades busquen el producte de proximitat, més qualitat i menys quantitat. Aquests petits canvis ens permetran fer una compra amb consciència, prioritzant només els productes que necessitem i cuidant al mateix temps la nostra salut i economia. Algun exemple que podem aplicar a la nostra vida diària podria ser beure aigua en envasos reutilitzables (ampolles de vidre o metàl·liques) i evitar així la compra diària d’ampolles d’aigua, tot substituint-les per garrafes que són més econòmiques i ens duraran més temps.

El mateix podem fer a l’hora de la compra, portant la nostra bossa per evitar comprar bosses de plàstic. Un altre truc útil pot ser organitzar el nostre menú setmanal, per saber què menjarem cada dia i, per tant, què ens cal comprar. Ni més ni menys. Pel que fa a productes d’higiene, podem optar per paquets familiars, on hi ha més quantitat per menys preu, o bé alternatives com les pastilles de sabó o les copes menstruals que, més enllà de ser econòmiques, no generen residus. També existeixen botigues a granel on pots comprar només la quantitat que necessites, sigui de productes alimentaris o de neteja de la llar. Investiga la teva zona i busca l’opció que més s’adapti a la teva butxaca, recordant sempre que allò que s’ha fet sempre, o allò que fa la majoria, no sempre és la millor opció per tu.

Pel que fa al transport, també cal buscar aquest equilibri i valorar alternatives al transport privat, que suposa un cost més elevat si sumem gasolina, impostos, assegurança i reparacions. El transport públic o la bicicleta són dues opcions econòmiques que ens poden ajudar a controlar les nostres despeses al mateix temps que cuidem el medi ambient. Fins i tot en el moment de sortir de festa podem retallar despeses si actuem amb consciència. Reservar amb antelació, aprofitar ofertes i descomptes o marcar-nos la quantitat que volem gastar abans de començar la nit ens ajudarà a mantenir un cert control. Si aquesta última part és la més difícil, un truc pot ser portar en efectiu l’import que volem gastar. D’aquesta manera, no hi haurà marge de passar-nos de pressupost i això ens permetrà gestionar millor les sortides, sense gastar ni un euro més del que toca.

Controla la teva situació econòmica des del mòbil

Aquestes són algunes de les recomanacions que ens ajudaran a mantenir el control dels nostres estalvis, però la tasca important és analitzar la nostra situació particular i fer-nos les següents preguntes: de quins ingressos disposo? Quina quantitat he de destinar a despeses fixes? Què em queda per destinar a l’oci? Necessito estalviar de cara al futur?

Si una cosa tenim a favor, és que actualment existeixen aplicacions per gairebé tot. Controlar les nostres finances mai ha sigut tan fàcil. La majoria d’entitats financeres s’estan posant les piles des de fa anys perquè l’experiència del nou client digital sigui intuïtiva i àgil, de manera que en un sol clic tinguem a la nostra disposició tota la informació que desitgem, des del saldo total del compte (els diners de què disposem), fins a les despeses que hem realitzat amb la targeta, veient de manera gràfica on estem destinant la major part dels nostres diners. Això ens permetrà fer-nos una idea de la nostra situació actual i cap a on hem de dirigir els esforços futurs.

Treballar i estalviar, els dos grans aliats per tenir diners

Una eina clau per gestionar els nostres estalvis són les guardioles digitals, un espai del compte on posarem els diners que volem destinar a una activitat concreta. El funcionament n’és senzill: ens hem de proposar un objectiu, sigui un viatge o alguna cosa que volem comprar, i a partir d’aquí calculem quin import hauríem d’ingressar cada mes per aconseguir-lo. Cal buscar l’equilibri entre allò que desitgem i els nostres recursos actuals. Si volem més diners, haurem de treballar més. Si no podem treballar més, els haurem de gestionar de forma més eficient. Però, sigui quina sigui la nostra situació, prendre el control de les nostres finances i saber en tot moment què està passant al nostre compte corrent és indispensable.

L’últim consell és no perdre de vista que mai caminem sols. Tenim pares, familiars i molta gent al voltant que ens pot ajudar a entendre què significa tot allò que té a veure amb els diners, que, en definitiva, és entendre com funciona el món actual. Tenir el seu suport i seguir els seus consells serà un pilar indispensable perquè aquest primer contacte amb el món de les finances sigui clar i comprensible. Quan prenem el control dels nostres diners, estem prenent el control de la nostra vida.

11Onze és la comunitat fintech de Catalunya. Obre un compte descarregant la super app El Canut per Android o iOS. Uneix-te a la revolució!

The need for speed, traceability and transparency in cross-border payments expressed by corporates was one of the banking industry’s unfinished businesses. The widespread adoption of the SWIFT gpi service has transformed the cross-border payments experience.

The SWIFT bank-to-bank communication protocol, an acronym for Society for Worldwide Interbank Financial Telecommunications, is a messaging network that financial institutions use to transmit information and payment instructions globally. They do so using a secure and standardised system. Although there are alternative systems, such as the Russian SPFS or the Chinese CIPS, these are still in the minority.

Despite the popularity of the SWIFT protocol, the increasing globalisation and digitisation of international trade revealed some of the system’s shortcomings. Slowness, delays, errors, lack of transparency and high transfer fees were common customer complaints.

To address these shortcomings, SWIFT introduced the Global Payment Innovation (gpi) service in early 2017. Within the first year of its launch, 30% of international cross-border payments were sent via SWIFT gpi, and by 2020 this had risen to 70%.

SWIFT gpi

Speed, traceability and transparency

It is a protocol that adds a tracking process through a unique reference code, similar to that applied when sending or receiving a parcel by courier. It, therefore, provides a real-time view of the transfer, from sending to receiving the funds. Initially, only banks have direct access to this information, but it can be passed on to customers on request.

The ability to share this additional information with customers not only improves the customer experience but, according to SWIFT, eliminates manual intervention and saves on resource costs by reducing customer enquiries. Even so, the costs, fees and deductions applied by intermediaries are known in detail to all parties.

On the other hand, the real-time payments system – half of SWIFT’s gpi payments are paid in less than 30 minutes and all in less than 24 hours – makes it less likely that banks will ‘hold’ customer money for hours or days until it is credited to the recipient’s account, and makes it easier for a large proportion of payments to be made on the same day.

This is the key to the success and potential evolution of this technology. The rapid adoption of SWIFT gpi by financial institutions should translate into a win-win situation, providing users with direct, real-time access to gpi information without requiring a call to the bank, thus empowering the customer.

If you want your business to make a giant leap, use 11Onze Business. Our business and freelancer account is now available. Find out more!

The real estate sector is experiencing a sharp drop in sales caused by high-interest rates and difficulty in obtaining credit. François Villeroy de Galhau, governor of the Bank of France, urges commercial banks to make it easier for consumers to borrow.

The rise in interest rates that began more than two years ago across the European Union has had an effect on the real economy, causing European residential real estate investment to fall by 54% in the first nine months of 2023 compared to the previous period, 55% lower than the average of the last five years.

This implosion of the real estate sector has been particularly evident in Europe’s richest countries. In France, the year began with construction of new housing falling to levels not seen since 2010. As wages stagnated, prospective buyers were faced with soaring inflation and increasingly unaffordable mortgages. This translated into a sharp drop in real estate transactions in the first half of 2023, particularly significant (-30%) in the Paris metropolitan area.

The French government and the ECB indicate that, for the time being, there will be no further interest rate hikes. Even so, according to the barometer of the Odoxa Demoscopic Institute, the rise in interest rates, the difficulty in obtaining credit, and concerns about the current international economic situation have caused 38% of French consumers who were considering a real estate project to cancel or postpone it.

This crisis is having a significant impact on the whole real estate sector, which represents 13.3% of France’s GDP. Real estate agencies, construction businesses, developers and, especially, credit intermediaries have experienced an increase in the number of insolvencies that had not been seen for years.

According to data from Altarès, an agency specialising in business information, during the first four months of the year, non-payments by developers have increased by 53.8%, those of construction companies by 55.6% while those of real estate agencies have almost doubled, with an increase of 84% compared to the same period in 2022.

Facilitating access to credit

With interest rates rising from an average of 1.03% in October 2021 to more than 4% in May 2023, and strict regulations on the granting of mortgages, obtaining a loan has become increasingly difficult for consumers looking to buy a home.

The governor of the Bank of France, François Villeroy de Galhau, has taken a stand against investors who expect interest rate cuts in the first half of next year, stating that the ECB is likely to keep them at 4% “at least for the next few meetings and the next few quarters”.

Even so, he urged commercial banks to “play the game”, facilitating lending to consumers, “It is desirable that the supply of bank loans now gradually recovers, but without running the risk of over-indebting households”. Bear in mind that the granting of real estate loans by commercial banks is at historic lows that have not been seen since 2015.

In this context, there has been an average year-on-year fall of 3% in house prices and this trend is expected to continue over the next six months, especially in large urban centres. Eric Allouche, CEO of ERA Immobilier, noted that property price falls are moderate compared to the collapse in sales, but that it is possible that by the end of the year house prices will fall by up to 6%.

Protect yourself from economic crises with the ultimate safe-haven asset: gold. If you want your savings to keep or increase their value, Gold Patrimony.

The largest cumulative banking collapse in modern US history, along with the defeat and subsequent sale of Credit Suisse, represents the worst year for banking since the 2008 financial crisis.

The failures of Silicon Valley Bank and Signature Bank in March 2023, followed two months later by First Republic Bank, marked the worst US banking crisis in its modern history. The total assets held by the three banks amounted to more than 450bn euros. Adjusted for inflation, this number exceeds the holdings of the 25 banks that collapsed during the 2008 global financial crisis.

The financial markets were panicking, central banks were mobilised, while the US administration called for calm and put in place a series of emergency measures to strengthen confidence in the banking system. To stop the flight of deposits and avoid contagion to other banks, which would have a domino effect, the US regulators launched a one-off initiative to guarantee 100% of deposits.

Meanwhile, on the other side of the pond, Credit Suisse was in free fall. The financial institution’s sharp stock market decline has halved the value of its shares, while the restructuring announced by the bank’s management did not prevent a flight of hundreds of millions of euros in deposits.

The Swiss National Bank (SNB) approved emergency funding of up to 57 billion euros to bolster Credit Suisse’s liquidity amid the banking crisis. A few days later, UBS absorbed its banking counterpart in a rescue operation designed to prevent its demise.

Holding US Treasuries as collateral

A large part of SVB’s business model was based on investing the money of its clients – mostly tech start-ups with a lot of liquidity – in long-term fixed-income deposits. After decades of very low, or even negative, interest rates, it was a very lucrative business. At the end of 2022, this institution had a total of $160 billion in deposits, half of which was invested in US Treasury bonds and mortgage-backed securities.

In the context of the global crisis and subsequent interest rate hikes by the Federal Reserve to combat inflation, the price of money became more expensive and investment was reduced. As a result, many of these start-ups suffered from a lack of funding or wanted to get more return on their deposits. This led many of them to withdraw more funds than the bank had planned, thus forcing the financial institution to sell a large part of these investments in public debt before maturity and at a discount to return the deposits.

Fears that the bank would not have enough cash to return the money to customers who asked for it caused panic and the withdrawal of 41 billion dollars in just one week. The bank sold a bond portfolio valued at 21 billion, just to cover its liquidity, at a loss of 1.8 billion. A rapid deterioration of the bank’s balance sheet led to its collapse.

Since the 2008 financial crisis, certain supervisory rules were relaxed for mid-size banks such as SVB. The regulation under which they were operating did not require them to recognise any of the losses they were taking on those bonds that were dropping in value as rates went up.

In the case of Credit Suisse, and beyond the lack of investor confidence due to the negative figures and doubts about the bank’s funding capacity, the bank had long been in the red due to a string of scandals and a series of fundamental management errors that castrated its ability to recover after the downturn experienced by the investment banking sector in the wake of the health crisis.

Protect yourself from economic crises with the ultimate safe-haven asset: gold. If you want your savings to keep or increase their value, Gold Patrimony.

What many suspected has been confirmed: Black Friday is actually a big marketing campaign. Discounts hardly ever reflect reality and prices on electronics and household appliances are on average 3% higher than the lowest price recorded in the previous 30 days, according to the Organisation of Consumers and Users (OCU).

According to a survey by Tandem Up, 85% of consumers planned to buy something on Black Friday. And the fact is that more and more people are bringing their Christmas shopping forward to take advantage of the supposed sales of this campaign. However, the reality is that the advertised discounts that they found were almost always false, according to a study by the OCU.

This research has compared the evolution of 16,000 online prices over more than a month, mainly for electronics and household appliances, but also in other areas. Its main conclusion is that 99% of the advertised discounts are not real. In fact, the theoretical average discount of 25% labelled for Black Friday turns into an average increase of 3% on the minimum price recorded during the last month.

Non-compliance with regulations

For most products, online retailers do not use the lowest price of the last 30 days as a reference for comparative savings, but any other price recorded during that period or even the recommended retail price, which breaches current legislation.

It should be borne in mind that Law 7/1996 on the Regulation of Retail Trade, recently amended to adapt it to European directives, establishes in article 20.1 that whenever articles are offered with a price reduction “the previous price must be clearly shown together with the reduced price” and that “the previous price shall be understood to be the lowest price that had been applied in the previous 30 days”.

Fortunately, if you think that your rights have been violated, you can file a complaint with the Catalan Consumer Agency, a Municipal Consumer Information Office or one of the Consumer Arbitration Boards.

Catalonia is no exception

Bad practices on Black Friday seem to be widespread if we take into account research on the previous Black Friday campaign in the UK that reaches very similar conclusions to those of the OCU.

After checking 214 offers at seven of the UK’s leading home and technology retailers (Amazon, AO, Argos, Currys, John Lewis, Richer Sounds and Very) during the 2021 Black Friday campaign, it found that 86% of these items had been offered cheaper or at the same price at some point in the six months prior to Black Friday.

It’s clear that Black Friday discount labelling can’t be trusted, so the only alternative, if you’re looking for bargains, is to keep track of price trends for the products you’re interested in. This is the only way to make sure you get them at the right time.

If you want your business to make a giant leap, use 11Onze Business. Our business and freelancer account is now available. Find out more!

While the top 1% hides 10% of the world’s GDP in tax havens, governments keep chasing freelancers and small businesses as if they were to blame for the gap. A structural imbalance that exposes the moral, economic, and political bankruptcy of the current fiscal system.

Globally, around 10% of the planet’s GDP is hidden in opaque jurisdictions. Trillions of euros escape taxation, distort economies, and perpetuate inequality. Yet, tax audits remain focused on the self-employed and small companies —a paradox that exposes the extractive and clienteles nature of our economic system.

The shadow of global money

According to estimates from the Tax Justice Network, around 10 trillion dollars —one-tenth of the world’s GDP— are hidden in tax havens. Luxembourg, the Cayman Islands, Bermuda, or Switzerland act as safe harbours for capital fleeing taxation, regulation, or social responsibility. Major fortunes, multinationals, and investment funds channel profits there that go untaxed where they were actually generated.

These practices are legal in many cases, but ethically indefensible. Above all, they represent a massive drain on public finances. According to the OECD, states lose more than 400 billion euros every year in tax revenue —money that could fund public services, reduce debt, or boost productive innovation.

Taxation for the usual suspects

On the other hand, workers, freelancers, and small businesses face record-high tax pressure. In Catalonia, according to Spain’s Tax Agency, people pay up to 12.5% more income tax than in Madrid. This burden falls mainly on middle and low incomes, while large fortunes optimise their taxation through international structures.

This dynamic is the essence of what 11Onze has often described as clienteles capitalism and the extractive system: a model in which political and economic power cooperate to keep wealth flowing from the bottom up, socialising losses and privatising profits. The biggest tax dodgers don’t need briefcases —they have law firms.

Clienteles capitalism: legal corruption

Most of this fraud is not the work of criminal networks, but of law firms, auditors, and lobbies exploiting tailor-made legal loopholes. This is what we call crony capitalism: an ecosystem where laws are drafted to protect private interests, and the line between public and private power becomes blurred.

The result is that, while small taxpayers are criminalised, large-scale evasion becomes just another financial service —offered with total impunity. The same states that bailout banks and corporations with public money turn a blind eye to the flows of capital escaping to Delaware or Luxembourg.

The vicious circle of inequality

The most perverse aspect of this mechanism is its multiplier effect. When the richest stop paying taxes, governments offset the loss by increasing the tax burden on consumption and middle incomes. VAT goes up, public services deteriorate, and inequality deepens.

This spiral erodes public trust and undermines the social contract. Why should ordinary citizens comply with the tax authority when the wealthiest don’t?

A system that protects itself

The implicit message is clear: not everyone plays by the same rules. Pursuing small taxpayers is profitable —statistically and politically— while fighting international tax evasion is complex and threatens powerful interests. Thus, the system defends itself, as described in the article The relevance of the extractive system: power mechanisms are designed to guarantee stability, not justice.

The solution is not merely technical but political. It requires the will to confront massive capital flows and establish an international tax framework that prevents a race to the bottom between nations. Initiatives like the G20’s 15% minimum corporate tax rate are a timid step, but far from enough. The real challenge is to make money work for society —not the other way around.

As long as 10% of the world’s GDP remains hidden, the official narrative will keep talking about a “fight against tax fraud” through audits of freelancers earning €2,000 a month. But the real fraud is structural. If we want a sustainable and fair future, we must demand transparency, sovereignty, and accountability. Taxation should not be a tool of submission, but an instrument of redistribution.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

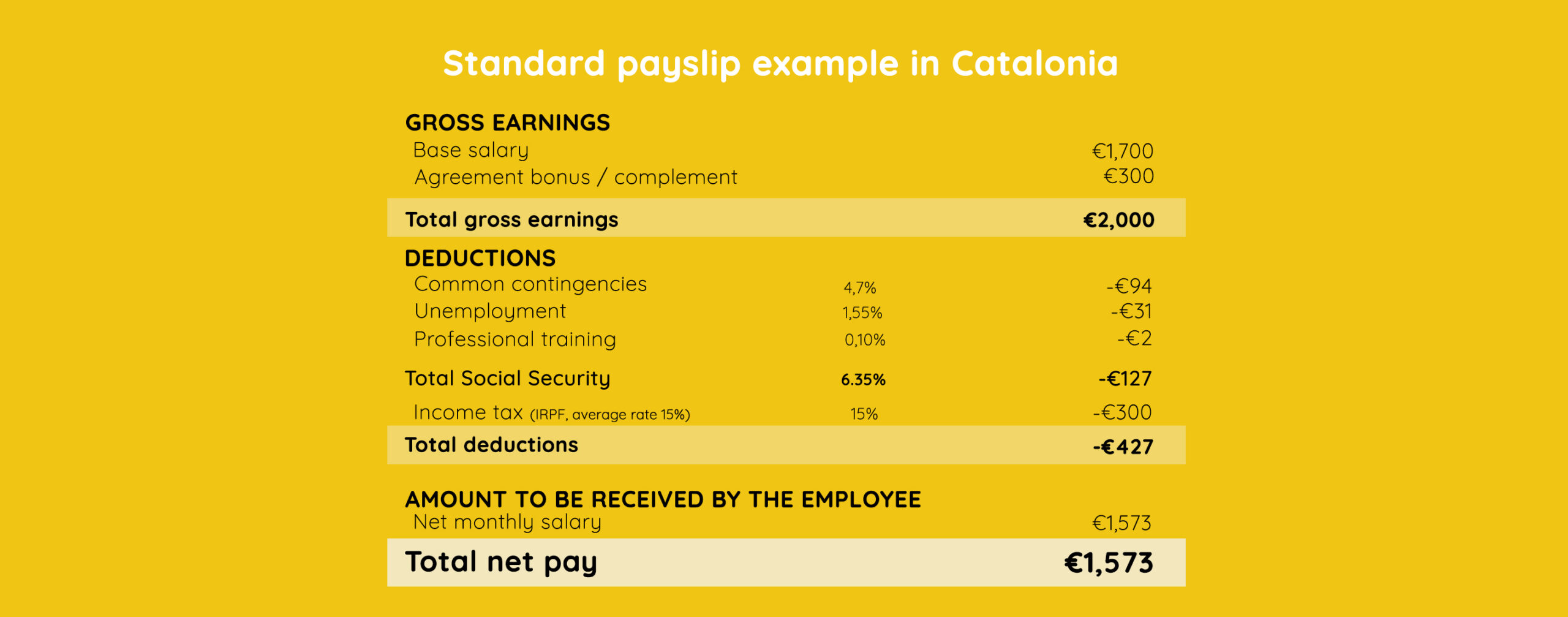

When you receive your payslip and notice that nearly a hundred euros are missing each month, it’s natural to ask: where is that money going, and why is it increasing if taxes haven’t been raised?

The answer is less visible than it seems. It’s called “cold progressively”, and it’s the silent tax hike that occurs when the government fails to update income tax brackets (IRPF) in line with inflation.

The IRPF withholding is the part of your salary that your company pays directly to the tax office on your behalf. It’s not a new tax — it’s an advance payment of what you’ll declare later on your annual income tax return. That means each month you’re lending money to the State, which may or may not refund it, depending on your personal situation. These funds don’t go specifically to pensions or any concrete service: they flow into the State’s general treasury, from which all public spending — including pensions — is financed.

Example of a real payslip showing how deductions reduce

the gross salary by €427 per month.

So far, so good. The problem arises when your salary increases to offset inflation — say, by 4 % — and suddenly your tax withholding also increases. You’re not wealthier: the tax system simply isn’t adjusted to the real price level.

IRPF: a progressive tax… frozen in time

The IRPF is progressive, yes: the more you earn, the higher percentage you pay. But this progressively gets distorted when brackets aren’t updated for inflation. A nominal salary increase — without real purchasing power gain — pushes you into a higher bracket, making you pay more for earning the same or even less.

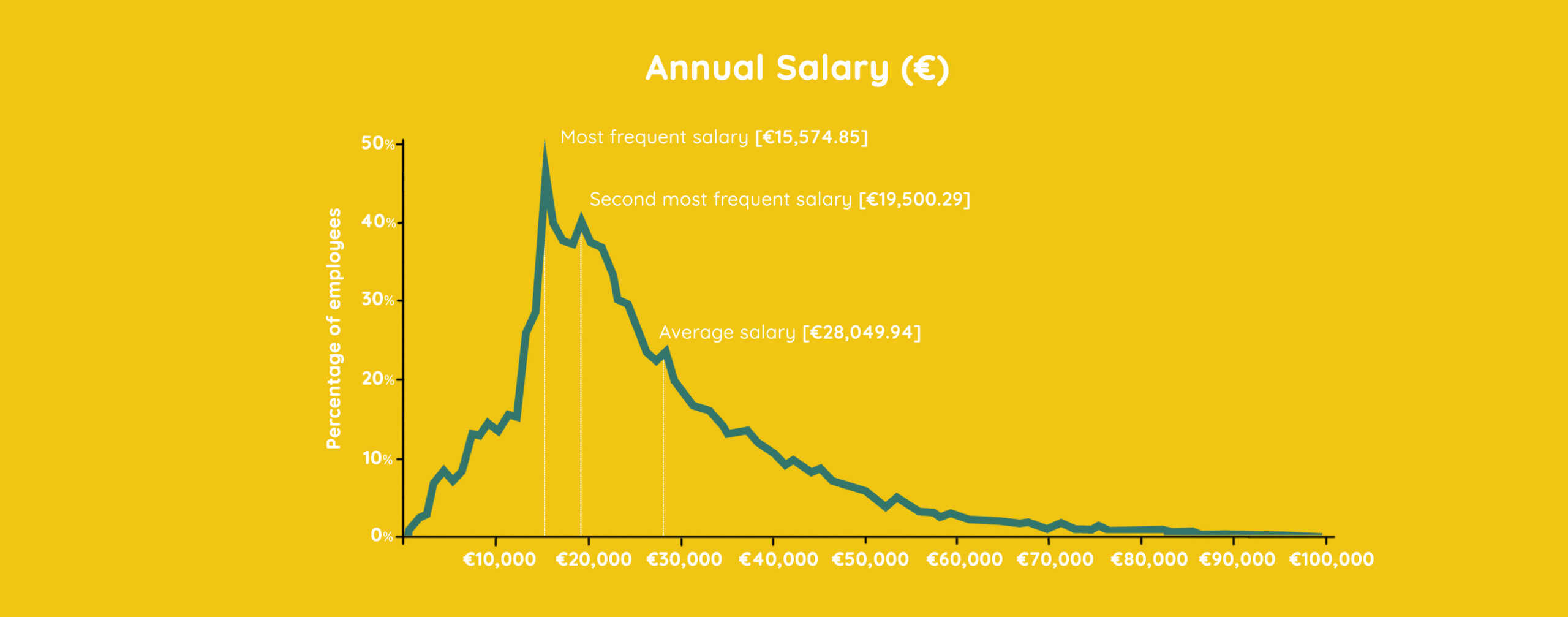

A worker going from €20,000 to €21,000 to offset inflation ends up paying €95

more in annual IRPF without improving purchasing power. (Source: INE)

According to the Fedea (Foundation for Applied Economics Studies), failing to adjust tax brackets to inflation costs the average family €736 per year. And Funcas (Foundation of Savings Banks) estimates that half of the IRPF revenue growth between 2019 and 2023 comes from this inflation effect on stagnant real wages. In other words: your salary rises by 4 %, prices by 4 %, yet you pay 6 % more to the tax office. The perfect trap.

Inflation: the silent ally of the Treasury

When prices rise, so do tax revenues. VAT, for instance, is applied to higher prices: if a purchase goes from €100 to €110, the 21 % VAT also increases. That happens in millions of transactions every day.

According to data from the Spanish Tax Agency, total tax revenue in 2022 hit a record €255.463 billion, 14 % more than the previous year. No new taxes, no rate hikes — just inflation. Economists call this the “invisible tax of inflation”: a mechanism that collects more without any parliamentary approval.

Real wage vs. nominal wage: the loss of purchasing power

Many workers have seen their salaries rise by 3–4 %, but if inflation is 5 %, the real outcome is negative. You earn more, but you can buy less.

According to INE (Spain’s National Statistics Institute), average purchasing power has fallen 6.7 % since 2020, while IRPF revenue has risen by over 20 %. In other words: wages rise 4 %, prices 4 %, but you pay 6 % more in taxes.

This combination is devastating. It shows Spaniards have less purchasing power, higher taxes, and lower household savings. A formula that punishes middle and working-class families.

At La Plaça, we’ve already explained that a living minimum wage in the Barcelona area should be around €1,322 per month, well above the national minimum wage. This wage gap explains why inflation hits working households hardest and drastically reduces their saving capacity.

Europe: three models, three outcomes

In Europe, there are three different approaches:

- France and Austria automatically adjust brackets to inflation, so taxpayers don’t lose fiscal purchasing power.

- Portugal does it partially, revising thresholds and deductions each year.

- Spain hasn’t done it since 2008, despite cumulative inflation of 26 % in fifteen years.

The result, according to Eurostat, is clear: Spain’s tax burden stands at 42.2 % of GDP — the highest in its history and above the European average (41.4 %). Yet, paradoxically, public services haven’t improved accordingly.

Who pays more? Always the middle class

High-income earners find legal ways to optimize; low-income earners receive subsidies and allowances. But households earning between €20,000 and €40,000 a year bear the bulk of the tax burden. That’s the heart of “cold progressively”: a system that becomes regressive under inflation.

Experts agree:

- Index IRPF brackets and thresholds to inflation.

- Lower withholdings for incomes under €30,000.

- Review family and dependency deductions.

- Increase transparency around actual withholdings.

These measures would preserve true progressively without undermining structural revenue.

No government announces this hike. It doesn’t appear in budgets or press conferences, yet each year tax brackets remain frozen, the State collects more and workers take home less. Inflation is inevitable. Fiscal abuse isn’t. Understanding what’s being withheld is the first step to defending your real income.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Financial markets are concerned about the growing fiscal deficits of Western governments, which risk entering a vicious circle that might send debt spiralling out of control, threatening the credibility of their currencies.

Republican Senator Rand Paul could not have been more blunt when he said in an interview on Fox News last Sunday that “it’s out-of-control spending, and we are threatening the very existence of our currency, and perhaps our country, with this crazy, profligate spending”.

He is neither the first nor the only voice warning of the dangers of excessive government spending. Billionaire Jeffrey Gundlach, known in the US as the bond king, “Bond-King”, warns that “the future of the US dollar and possible runaway inflation depends on getting the budget and spending under control”. More worryingly, he warns that the federal government is likely to spend aggressively during the next economic downturn and bring itself to the brink of financial collapse, “The response to the next recession will be a complete disaster relative to our fiscal position, and this will be the wake-up call where we realise that the United States is bankrupt, that we cannot meet our liabilities”.

It is no secret that in the face of economic crises come large fiscal expansions, but the resulting increases in sovereign debt and interest rates can limit the availability of business borrowing, reduce investment and weaken national currencies. President Joe Biden is asking Congress for $100 billion in new foreign aid and security spending at a time when the US budget deficit has ballooned to a level not seen since the COVID-19 pandemic.

A deficit of nearly $1.7 trillion in fiscal year 2023 – a 23% increase over the previous year – due to falling revenues and rising expenditures has once again brought the debt sustainability debate to the fore and called into question the fiscal policies of the current administration.

Europe lagging behind the US

While it is true that decoupling US monetary policy from the monetary policies of other Western central banks could alleviate the risk of global recessions, in practice, concerted monetary policies between countries in the same geopolitical bloc remain the norm, facilitating the global contagion effect of economic crises.

That said, the divergence between the EU and US economies is significant. After the pandemic, the US economy recovered much better than the EU, and this dissonance has widened further in recent months. While the US economy is accelerating at a healthy pace and grew by 4.9% in the third quarter, half of Europe is stagnant or in economic contraction and the GDP of the eurozone countries fell by 0.1% in the third quarter of the year, leaving them close to a recession.

Wall Street banks expect rising energy prices and weak eurozone growth to drag the euro down into parity with the dollar. JPMorgan has revised down its forecast for the euro to $1 by the end of the year, while Citibank expects it to reach parity “within six months”, given its “current view that the European recession is well ahead of the US recession”.

Given this bleak economic outlook and the unreliability of these two currencies, it is hardly surprising that central banks and private investors continue to buy gold en masse, at the very least, to secure an alternative to a Western monetary system that appears to be in agony and free-falling.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

American magnates —Bezos, Dimon, Buffett, Ellison— are selling stocks in a moment of market euphoria. What do they know that the rest of us ignore? When those with privileged information flee the very markets they built, we may not be talking about conspiracies, but about a clear signal: the system is creaking from within.

At first glance, everything looks fine. The S&P 500 is hitting record highs, the Nasdaq has recovered from the 2022 crash, and the big tech companies are leading the party. The media speaks of a “new innovation cycle.” But beneath this radiant surface, something is stirring.

According to public data, Bezos sold about $737 million worth of Amazon shares at the end of June 2025. Jamie Dimon sold roughly $31.5 million in JPMorgan shares this year —the first sale since he became CEO—; Brian Chesky (CEO of Airbnb Inc.) sold 190,301 shares on February 12, 2025, worth approximately $26.7 million.

The University of Melbourne sums it up: “While institutional investors sell, retail investors buy.” Small investors, encouraged by media optimism, enter the market just as those who know it best are heading out the back door.

Those who see before we do

This is not about conspiracy, but information asymmetry. The big players have analytical systems and access to data that allow them to detect, months in advance, the symptoms of a brewing crisis. The indicators they track —tensions in the debt market, drops in real productivity, or signs of exhaustion in the Federal Reserve’s expansionary policy— are invisible to ordinary citizens.

When these warnings pile up, smart money moves. The rich don’t sell because they need liquidity; they sell because they want to leave before collective confidence breaks. It’s the same instinct that makes central banks hoard gold while assuring us that inflation is “transitory.”

Turkish economist Nouriel Roubini is known for his ability to foresee major financial crises. A professor at NYU’s Stern School of Business, he rose to global fame after accurately predicting the 2008 financial crisis, earning the nickname “Dr. Doom.” In his words: “Confidence in the financial system doesn’t collapse overnight; it unravels like a threadbare stocking.” The tycoons’ moves are precisely those first threads snapping.

Fear of the new financial order

Another factor haunting the ultra-rich is the structural shift in the global monetary system. The Bank for International Settlements (BIS) confirms that over 130 countries are now working on central bank digital currency (CBDC) projects. At first glance, they appear to be a natural technological evolution of money. But in practice, they enable total control over transactions and individual wealth.

Bloomberg recently warned that CBDCs could pose serious privacy and control challenges, as governments would gain direct access to transaction data and could impose restrictions on how money is used.

Meanwhile, dedollarization is advancing. Russia, China, India, and Brazil are promoting bilateral trade deals without the dollar, while central banks are hoarding gold at record levels. According to the World Gold Council, more than 1,000 net tons of gold were purchased in 2024 —the highest volume in half a century. Private capital is following the same path. They no longer trust the system they designed themselves.

The divorce between the market and the real world

Meanwhile, the gap between market valuations and the real economy widens. Corporate profits are not growing at the same pace as stock prices, and U.S. public debt already exceeds 125% of GDP.

Stock prices now reflect a fiction of prosperity, sustained by massive buybacks and money printing. The Federal Reserve has injected more liquidity in the last decade than in the entire 20th century. But cheap money has created an artificial economy where wealth isn’t produced —it’s mirrored.

This model increasingly resembles a pyramid: as long as new investors are willing to buy, the system stands. Once those at the top start selling, the countdown begins.

The return to real assets

When the air of the system becomes too toxic, the rich return to where there’s always oxygen: tangible assets. Gold, silver, farmland, energy, and even physical art become safe havens against monetary instability.

Gold keeps breaking records daily, the clearest example of all. While markets celebrate new technologies and digital ETFs, financial elites are buying physical metal. The Wall Street Journal notes that while gold-related companies grow, physical gold remains the only true safe haven —proof that trust has gone digital, but fear remains solid gold.

The logic is simple: an asset that depends neither on a government’s promise nor a company’s performance is the only one capable of weathering a systemic storm.

When flight becomes a warning for all

The rich fleeing is not an anecdote —it’s a metaphor for the end of a cycle. Financial capitalism, as we know it, is reaching saturation, driven by unlimited debt, wealth concentration, markets detached from reality, and confidence that is no longer blind but forced.

However, this flight could also be an opportunity. If those who control the system are stepping aside, it’s time for citizens to regain real financial power: to learn how money works, protect their savings, diversify, and invest with common sense.

As Raymond Thomas Dalio, one of the world’s most influential investors and founder of Bridgewater Associates, reminds us: “When things that seem permanent stop being so, those who understand change survive; the rest suffer.”

We need not see conspiracies where there is prudence —but we cannot ignore that when those who know the most about money leave the table, the game is about to change. The rich are fleeing their own system because they know trust is finite —and the next crisis won’t just be financial, but one of legitimacy.

In that scenario, the ordinary citizen has only one choice: understand the system to stop being its victim. Start thinking like those who are leaving —not to imitate them, but to anticipate. Because true economic freedom is born from knowledge, not faith in a system already taking on water.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Alguns conceptes són bàsics per a entendre per què estem a la vora d’una recessió, cap a on s’encamina el nou ordre econòmic mundial i quins seran els seus protagonistes.

El “Gran Reinici” és el nom d’una iniciativa del Fòrum Econòmic Mundial que pretenia repensar el model econòmic capitalista una vegada superats els estralls provocats per la pandèmia. La realitat és que a la crisi sanitària s’han sumat una crisi de deute i una crisi inflacionària que ens han situat a la vora de la recessió.

En el context actual, el “gran reinici del capitalisme” que reclamava aquest organisme internacional es fa més necessari que mai. Repassem alguns conceptes clau per entendre com hem arribat a una situació pròxima al col·lapse i quins factors condicionaran el futur pròxim de l’economia.

Àsia

L’eix de l’economia global s’està desplaçant d’Europa i els Estats Units cap a Àsia. Segons un estudi de la consultora McKinsey, l’any 2040 el continent asiàtic suposarà més de la meitat del producte interior brut mundial i un 40 % del consum. La pèrdua de protagonisme d’Europa és evident i l’FMI preveu que almenys la meitat dels països de l’eurozona entraran en recessió en els pròxims mesos.

Canvi climàtic

L’escalfament global ha obligat a deixar enrere la idea d’un creixement il·limitat a costa d’esgotar els recursos naturals i ha donat pas a la idea de l’economia circular, amb oportunitats en el camp de l’economia “verda”. Com ha posat de manifest la COP27, ara falta definir fins a quin punt els països industrialitzats assumiran el cost econòmic del canvi climàtic que han generat i quines mesures estan disposats a adoptar per alentir l’escalfament en un context de crisi econòmica.

Descentralització

Les noves tecnologies estan permetent l’aparició de productes i serveis que escapen al control dels Estats i les grans corporacions. Com apuntava James Sène, president d’11Onze, en una sessió de Fintech Talks, ens trobem davant una “transició del model antic, totalment dominat per uns pocs, a un nou model que arriba a més gent i està descentralitzat”. La descentralització de la creació monetària, per exemple, ha estat un dels grans pilars de les criptomonedes.

Desigualtat

Les dades de l’informe “World Inequality Report 2022” mostren que el 10 % de la població més rica del planeta ha acumulat des de mitjan anys noranta el 76 % de la riquesa generada al món. De fet, el 38 % es va concentrar a les mans de l’1 % de la població mundial. I la meitat de la població més pobra s’ha hagut de conformar amb les engrunes: el 2% de la riquesa generada durant aquestes últimes dècades. Per desgràcia, aquesta escletxa entre els superrics i el comú dels mortals no ha fet més que eixamplar-se durant la pandèmia. I els experts coincideixen que aquesta creixent desigualtat suposa un fre per al desenvolupament econòmic mundial.

Deute públic

El deute públic en el món s’ha disparat en els últims anys i limita el creixement econòmic. Tot i que el límit que estableix el Tractat de Maastricht per als Estats de la Unió Europea és del 60 % del seu PIB, el conjunt de països de la zona euro ja porta més d’un any per sobre del 100 %, segons dades d’Eurostat. La situació fora d’Europa no és millor, ja que el Fons Monetari Internacional estima que, a la fi de 2021, el deute públic global també representava el 100 % del PIB mundial. A més, els nivells de deute podrien empitjorar si la crisi s’accentua.

Estagflació

Des de març de 2021, els preus han pujat amb força i de forma gairebé ininterrompuda. La inflació a Catalunya, que va arribar a superar a l’estiu el 10 % interanual, es va situar a l’octubre prop del 7 %. La situació més enllà de les nostres fronteres no és millor, ja que la inflació d’aquest mateix mes en el conjunt de la zona euro va arribar al 10,7 %. S’espera que les successives pujades dels tipus d’interès contribueixin a controlar uns nivells d’inflació desconeguts des dels anys vuitanta del segle passat. El preu a pagar serà un major estancament de l’economia, que portarà a la recessió de les grans economies.

Impressió de moneda fiat

S’estima que el total de diners en circulació en el món, incloent-hi bitllets, monedes, xecs i pagarés, supera els 60 bilions d’euros. El problema és que una part considerable d’aquests bitllets s’han posat en circulació en els últims anys. Per exemple, només l’any 2020 l’oferta monetària dels Estats Units va augmentar un 24 %. La majoria dels bancs centrals s’han dedicat a imprimir moneda per fer front a un deute públic galopant. I aquest augment de moneda fiat ha estat el principal responsable de l’actual inflació.

Monedes digitals

Davant l’avanç de les criptodivises, que plantegen un model monetari totalment descentralitzat, els Estats treballen a contrarellotge en el desenvolupament de monedes digitals controlades pels bancs centrals (CBDC) per mantenir un sistema financer centralitzat. A la Xina, més de 260 milions de persones ja han utilitzat el iuan digital (e-CNY). A Europa, la Comissió Europea preveu que la regulació sobre l’euro digital estigui llesta a principis de 2023 i que aquesta moneda digital entri en funcionament l’any 2025. L’objectiu en un primer moment és que l’euro digital, gestionat i supervisat pel Banc Central Europeu, no substitueixi els diners en efectiu, sinó que els complementi.

Poder corporatiu

Les grans multinacionals tenen un poder creixent enfront de la minvant capacitat d’influència dels Estats. Moltes d’aquestes corporacions supervisen enormes cadenes de subministrament, venen els seus productes a tot el món i tenen uns ingressos superiors als de molts governs. De fet, si fos un país, Walmart seria el desè per nivell d’ingressos. La globalització ha capgirat les relacions de poder i en molts casos les grans corporacions es permeten eludir el pagament d’impostos amb total impunitat.

Subscripció

Com assenyalàvem en un article de La Plaça, està sorgint un nou model mutualista, més comunitari i basat en la compartició de béns i serveis, com a alternativa al model de compra i ús individual. En els models de negoci de subscripció cada client paga quotes que li permeten l’accés prolongat a un bé o servei en lloc de realitzar un gran pagament per endavant per posseir aquest bé o servei. Aquest model de negoci cada vegada és més freqüent en la indústria informàtica, de l’entreteniment o de l’automoció.

Tipus d’interès creixents

Després d’11 anys sense augments, el Banc Central Europeu va iniciar al juliol l’escalada dels tipus d’interès a Europa. De moment, ja han arribat al 2 % i la previsió és que continuïn incrementant-se en els propers mesos per refredar encara més l’economia i frenar la inflació. El BCE s’ha alineat amb la majoria de bancs centrals del món, que també estan incrementant les seves taxes d’interès per combatre l’escalada de preus. Aquesta mesura repercutirà directament en la butxaca de molts ciutadans, ja que les quotes de les hipoteques i dels préstecs amb interès variable resultaran cada vegada més elevades.

Virtualitat

No vivim en un món virtual, però sí virtualitzat, ja que “el que passa en el món digital té un impacte real en la nostra vida”, com advertia James Sène en una sessió sobre l’actual situació econòmica. En aquest sentit, el president d’11Onze vaticinava que el metavers, l’economia del qual depèn de l’autenticació de les propietats digitals, jugarà un paper clau a l’hora de digitalitzar les nostres identitats.

Si vols que el teu negoci faci un gran salt, utilitza 11Onze Business. El nostre compte d’empresa i autònoms ja està disponible. Informa-te’n!

Si t'ha agradat aquesta notícia, et recomanem: