Mobilize the savers to finance NATO

Military spending is at the centre of the debate because conflict is increasing. At the same time, the public debt of the Member States far exceeds the limits of the EU Stability Pact. Will the military necessity drive the union of European capital markets? Are they looking to capture citizens’ savings for the war?

The North Atlantic Treaty Organization was born in 1949 with a very clear objective: to protect the member countries of the Soviet Union. The current situation, with the entry of Sweden and the interest of most of the countries bordering Russia, forces us to have a look at the military spending of the member states. The war in Ukraine has turned Europe into a powder keg and the EU seems determined to maintain the onslaught with or without the help of the United States.

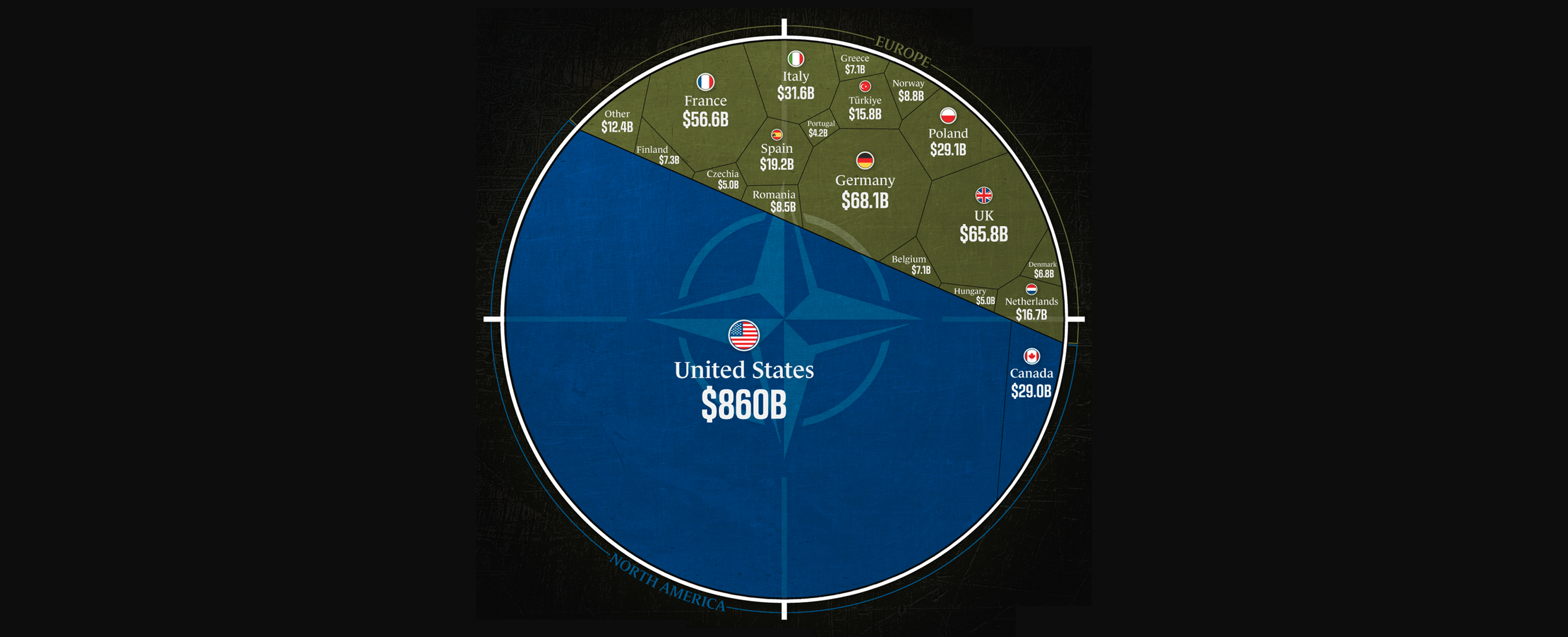

At this point, it is necessary to pay attention to who finances NATO since, the candidate for the presidency of the United States Donald Trump, announced that if he were to become president again he would not protect the countries that do not pay their part of the budget of the Atlantic Alliance. And it is true that around 69% of the budget is provided by the United States, reaching 860,000 million dollars. Therefore, it is true that the American contribution is much higher than the 68,000 million of Germany, the 66,000 of the United Kingdom or the 19,000 of Spain.

Source: Visual Capitalist

Who tries harder?

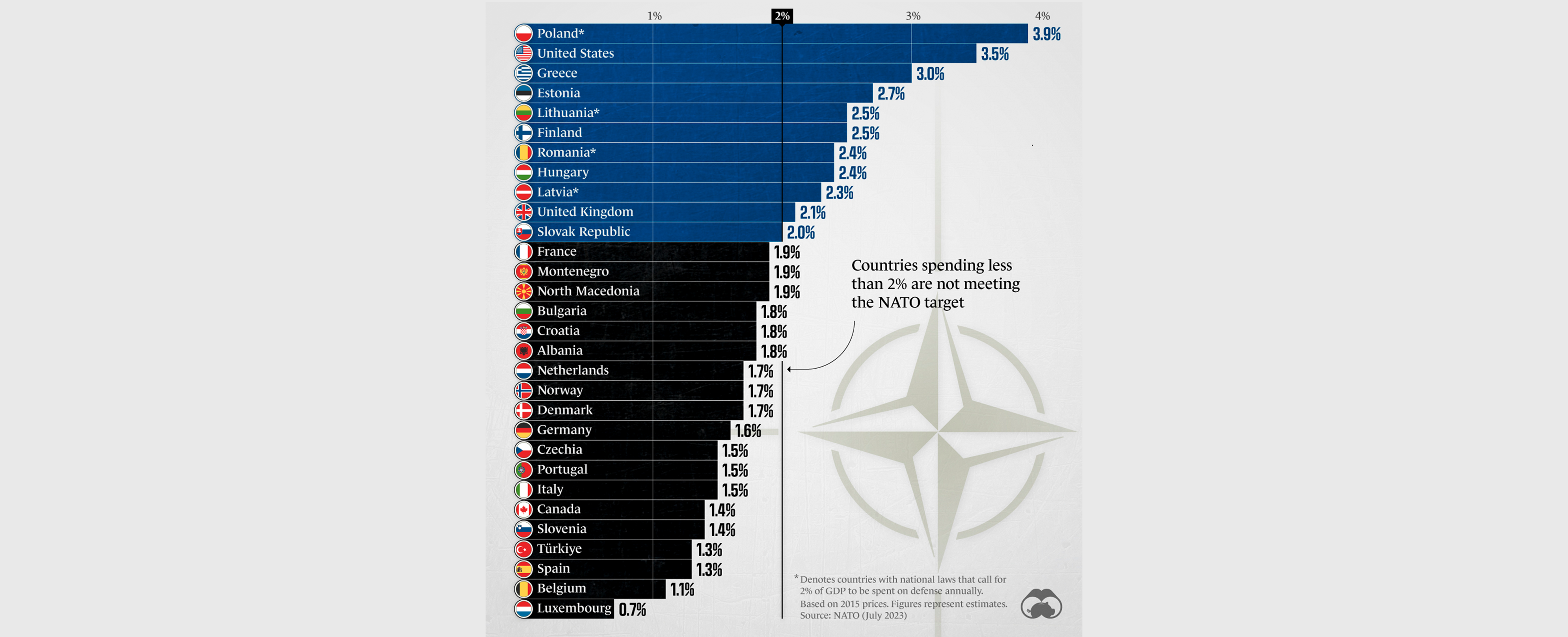

But it is necessary to put in context the contribution of the Member States because the effort is not the same for all economies. The objective is for each member to contribute at least 2% of their GDP. As we can see in the graph, there are many countries, including Spain, that do not inherit. But we also see interesting facts: Poland contributes, proportionately, more than the United States. And some of the countries that struggle the most border Russia and many were part of the Soviet Union, that is to say, they fear Putin based on common history.

Source: Visual Capitalist

European public debt

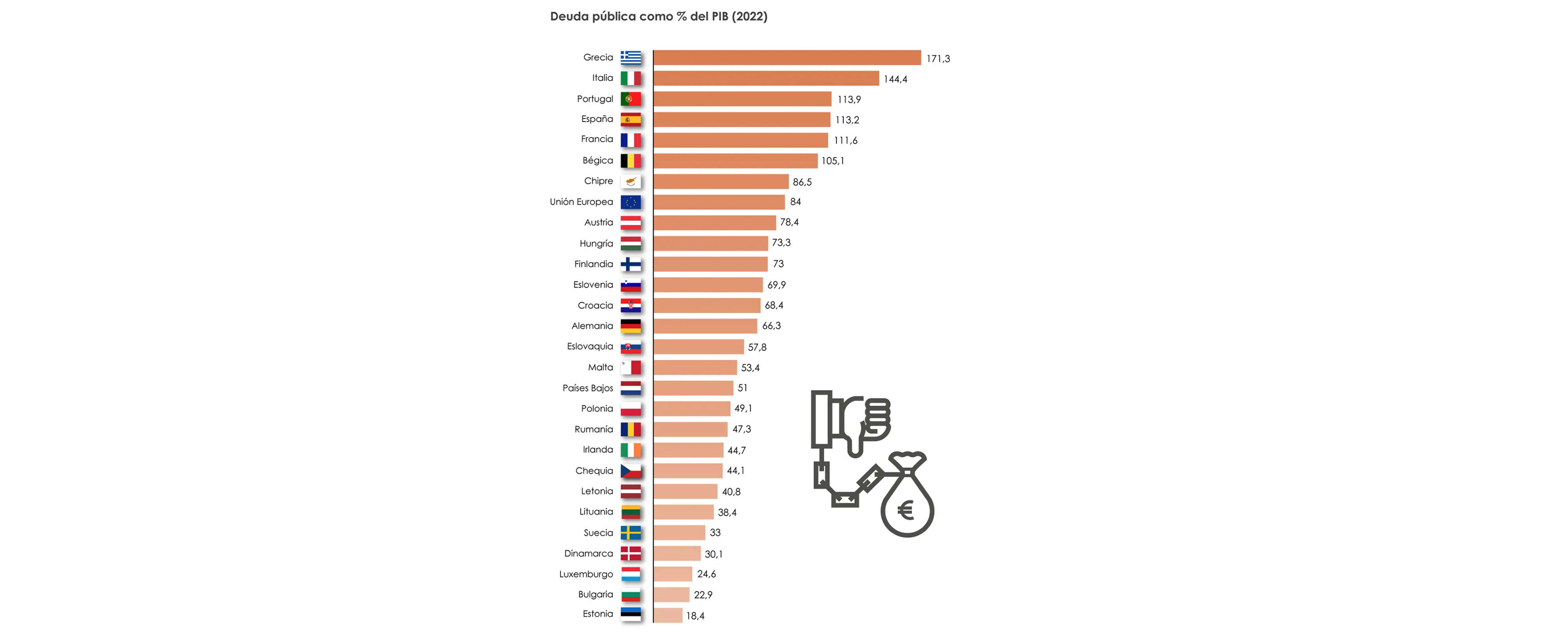

Given this situation, it should be remembered that the president of the European Commission, Ursula von der Leyen, announced her intention to continue increasing defence spending in the countries of the European Union. And here is another problem: most countries exceed the 60% debt allowed by the renewed Stability Pact. In other words, European countries must reduce their public debt at the same time that they are obliged to increase their military spending. Is it possible to square the circle?

Source: El Orden Mundial

Where will the money come from?

Although it is true that the Stability Pact of the EU includes the exception to deviating from the debt objectives for reasons such as defence, it is also true that large deviations would affect the credibility of the European countries in the markets, so it would be more difficult to finance.

In this context, a piece of news that has gone largely unnoticed, which is the intention to promote the union of European capital markets, gains particular importance. This is an old proposal that the French government is leading and that has Spanish support, but still does not have the German approval. Germany wants the 27 countries to join the union of capitals suddenly, while France sees it as impossible and plans to do it in phases.

The idea is to launch a common savings product to attract private capital. In other words, they want to attract the deposits of the citizens of the European Union. According to the French finance minister, Bruno Le Maire, it is necessary to “put the Europeans’ savings to work” to boost the massive investments that the European Union must make in the coming years. The official discourse is that capital must be obtained so that European startups do not end up asking American or Persian Gulf investors for money to advance their projects. Therefore, the idea would be to promote a certain economic independence from the EU. But the truth is that these massive investments have two-star themes: the energy transition and defence.

In this way, everything points to the fact that, during 2024, we will see the birth of a European investment product that will serve for EU countries to increase their participation in NATO without damaging much more their already punished public debt. The mobilization of savings for the war has already begun.

Ever since Mark Zuckerberg changed the name of Facebook to Meta, the idea of the metaverse has continued to grow. But the seed already existed. Technology gurus have been working for years to build the metaverse, a limitless digital universe where they claim we will do most of the vital transactions. Faced with the business opportunity, financial institutions have already begun to conquer this new virgin world.

Everything related to the metaverse sounds like science fiction, because it is, in fact, born of the science fiction that programmers, hackers, and technology tycoons love so much. The first time we read the word “metaverse” —a universe outside the universe— was in the cult novel Snow Crush (2010) by Neal Stephenson, who has publicly dismissed the way his idea is being used.

In this apocalyptic dystopia, the author imagines an internet world that is a single infinite highway, owned by a company called Global Multimedia Protocol Group. In this virtual state, users raise buildings in the shape and size they want, they transact without restraint and they themselves are embodied in impossible avatars. The only limit is the imagination.

The birth of a new world

Today, social networks and platforms are still incipient experiments that lead us irremediably towards this metaverse. But what does it really need to be? According to the experts, it needs to have four characteristics. The first is persistence, i.e. the new parallel universe must be like life itself, never ending and never restarting. Second, a massive scale of socialisation. Thirdly, an immersive technology that engineers are still not quite able to fine-tune and which they seem to want to introduce with virtual reality glasses. And finally, a real digital economy to sustain it.

It is in this sense that Mark Zuckerberg, after the very serious violations of the right to privacy that have taken him to court, aspires to lead and direct this new metaverse. In fact, for months now, rumours —the ‘New York Times’, without going any further, has echoed them— claim that Zuckerberg has already held talks with the big names in the American administration to make himself pardoned and to make them understand the geopolitical importance of the project.

We need to understand the context in which the idea of the metaverse is growing, because at least three battles are being fought at the same time. The first is undoubtedly the hegemony of the United States in a possible global crisis, as 11Onze’s Chairman, James Sène, explains. The second is the climate crisis: on a planet increasingly depleted of natural resources, the infinite possibilities of a metaverse are a fertile field for business. And the third is the struggle between the classic governmental structure of banking and the decentralised but equally predatory alternative proposed by the world of cryptocurrencies.

The universal conquest of finance

This is how companies, entrepreneurs, governments —the Catvers presented by the Generalitat is a good example of this obsession— and financial institutions have launched themselves into the conquest of the metaverse. According to a Bloomberg report, this new digital environment is currently worth 500 billion dollars.

From the world of finance, the first to give its unconditional support is Jefferies. Its Global Head of Thematic Research, Simon Powell, has stated that the metaverse will be “the biggest disruption” that humanity will experience in centuries. The other major banking group that has not been long in coming is Goldman Sachs, which points out that the blockchain will be the “fundamental technology” of the new metaverse. In this sense, its Managing Director, Rod Hall, has assured that in the new metaverse it will be necessary to identify the ownership of each asset very well and that this represents an opportunity for any financial institution.

The other big bank that is betting on this is Bank of America, which has already begun to train employees in its 4,300 centres in the United States in virtual reality. The bank’s Research Director, Haim Israel, has stated that cryptocurrencies can find in the metaverse an “opportunity” to become massive. It seems that traditional banks are beginning to realise the potential of cryptocurrencies and are willing to co-opt their structure, which until now has been growing on its own.

The bet is so strong that some banks, such as Korea’s IBK and KB Kookmin Bank, are already looking to work directly in the metaverse. IBK has reached an agreement with Cyworld, a Korean social networking platform that has its own cryptocurrency, Dotori, to launch financial products for its users. And in Spain, according to ‘Cinco Días’, the major financial institutions have already begun to test formulas and products just for the new digital world. The conquest of the metaverse by the financial sector is now unchecked.

11Onze is the fintech community of Catalonia. Open an account by downloading the app El Canut on Android and Apple and join the revolution!

Les Fintech estan guanyant terreny a la banca tradicional, prioritzant l’atenció al client i millorant la seva competitivitat gràcies a les eines que proporcionen les noves tecnologies. Joan Benedicto, agent d’11Onze, ens fa un resum dels principals avantatges de les Fintech.

De la fusió de “financial” i “technology” sorgeix el terme Fintech. Aquestes plataformes tecnològiques proporcionen serveis financers a través d’Internet i dispositius mòbils, i estan canviant la manera en què les persones administren els seus diners. Operen íntegrament en línia i ofereixen una àmplia gamma de serveis i productes, des de comptes corrents i d’estalvi fins a préstecs i inversions.

Un dels avantatges més importants de les Fintech és la comoditat. Les aplicacions i plataformes Fintech permetent als usuaris accedir als seus comptes i realitzar transaccions des de qualsevol lloc i en qualsevol moment, eliminant la necessitat de visitar una sucursal física. Això és especialment útil per als qui viuen en zones rurals o tenen agendes molt atapeïdes.

Avantatges de les Fintech

Innovació, agilitat i menys comissions

Les Fintech també ofereixen una major eficiència en comparació amb els bancs tradicionals. L’automatització els permet processar transaccions i fer-ne el seguiment de manera més ràpida i precisa. Això significa que els usuaris poden obtenir informes financers en temps real, efectuar pagaments i transferències en línia i obtenir respostes ràpides a les seves preguntes.

Gràcies a l’ús de les noves tecnologies, poden oferir productes financers innovadors i amb més flexibilitat respecte als productes dels bancs tradicionals. Això inclou préstecs en línia, pagaments amb targetes de crèdit virtuals, inversions en línia i pagaments amb criptomonedes.

Aquestes plataformes digitals no estan subjectes a sistemes heretats que depenen d’una costosa xarxa de sucursals físiques. Com apunta Benedicto, “com que els costos de l’empresa són menors, poden oferir serveis a un preu més reduït”, deixant enrere les comissions desorbitades a les quals ens té acostumats la banca tradicional.

11Onze és la fintech comunitària de Catalunya. Obre un compte descarregant la super app El Canut per Android o iOS. Uneix-te a la revolució!

Financial institutions have a long history of unethical and illegal behaviour. Abusive practices have resulted in numerous fines and penalties for banks, as well as damage to their reputation. Although governments and regulators claim to have strengthened supervision and regulation of the financial sector, the implementation of these measures has proved insufficient to ensure consumer protection.

The Payment Protection Insurance (PPI) scandal, which emerged in the UK in the early 2000s, concerned the mis-selling of insurance policies by banks and other financial institutions. These policies were sold with the intention that consumers would protect their loan or credit card payments in the event of illness, unemployment or other unforeseen circumstances.

However, many of these policies were sold to people who did not need them or did not qualify for them. In addition, payments to customers involved commissions in excess of 50%, thus preventing customers from actually benefiting from the policies’ coverages.

As a result of this inappropriate marketing, the Financial Conduct Authority (FCA) required the banks to pay billions of euros in compensation to affected consumers, who have been forced to pay out almost 60 billion euros. Sanctions and fines were not limited to British banks; Banco Santander had to set up a fund of 2 billion euros to cover possible claims.

Despite the compensation paid by the banks, the PPI scandal is far from over. Following a recent hearing in the UK High Court, it will be decided whether to extend the scope of the claims’ deadline, previously set for 29 August 2019, by up to six years to allow thousands of outstanding claims to be paid.

Claims at the Bank of Spain soar

Legal proceedings against abusive banking practices are increasing year after year. In 2021, customer complaints to the Bank of Spain increased by 61%, with CaixaBank, Santander and BBVA being the financial institutions with the highest number of complaints.

The banking malpractice of Spanish financial institutions since the financial crisis of 2008 is worthy of study. Abusive commissions, vulture funds, mortgage clauses, revolving cards, the preference shares fraud… these are just some of the abusive practices of banks, negligent and contrary to the interests of their customers.

The majority of customer complaints are concentrated on mortgages, cards and accounts and deposits. Eight out of ten complaints are directed against banks (83%), followed by credit unions (4.7%).

How to complain in the banking sector

The complaints’ system in the banking sector depends on the Bank of Spain, but before submitting any complaint to an official body, you should complain directly to the institution. If you go to a bank branch, you can ask for a complaint form, or send a letter by burofax or registered mail addressed to customer service.

The bank must respond within 15 working days in the case of claims related to payment services, and up to two months in the case of other claims. The next step is to wait for a response from the institution, but if it does not respond within these deadlines, or you do not agree with the resolution, you address your complaint to the Bank of Spain.

You can make your complaint in writing or online at the Banco de España’s Virtual Office, provided you have a digital certificate. This is a free, independent and impartial service, which does not take sides on behalf of consumers or banks, and which will decide whether the customer’s complaint is justified or not.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

UK financial entities have been fined billions of euros for abusive practices. We spoke to Farhaan Mir, CFO of 11Onze, about the Payment Protection Insurance (PPI) scandal.

The Payment Protection Insurance (PPI) scandal concerned the mis-selling of insurance policies, and it became known as Britain’s costliest consumer scandal. It emerged in the United Kingdom in the early 2000s, when banks and other financial institutions were found to have mis-sold PPI policies to millions of customers, often without their knowledge or consent, opening the floodgates to 60 billion euros of compensation claims.

The insurance policies were intended to cover loan and credit card payments in the event of unemployment, illness, or death, but many customers were sold policies that they were unlikely to be able to claim on, or that duplicated existing insurance coverage. In addition, payments to customers involved commissions in excess of 50%, thus preventing customers from actually benefiting from the policies’ coverages.

What were the main reasons why PPI policies were mis-sold to consumers?

In call centers and high pressure sales environments, people were pushing to get their commissions upfront. That’s the game banks played because the more loans they sold, the more profit they made. When you’re selling an insurance policy, a regulated product, you have to follow a process. In this case, the high profits and the commissions paid to the sales teams, which in some cases were paid three years in advance, were more important than applying the correct process.

How have financial institutions been held accountable for their role in the scandal?

It started with the Financial Ombudsman, when the non-disclosure ended, there was a complaint. As soon as that complaint went in, the banks had to start putting money aside for the penalties they needed to pay. They were aware they could not fight this in court. Basically, they were held accountable in the courts for the amount of PPI they miss-sold, and they’ve been held responsible for the amount of money that needs to be repaid.

What steps have been taken to ensure that similar mis-selling does not occur in the future?

Firstly, there were penalties for the banks. Second of all, when you buy a regulated product from a financial institution they have to tell you whether you’re eligible, or in other words, that you meet the suitability requirements. Basically, parties selling insurance have to make sure they’re selling you the right product, the right way, otherwise they risk being fined. Also, The Financial Services Authority (FSA) banned sales of single-premium payment protection insurance (PPI) alongside personal loans.

What’s the process of making a claim and how long does it usually take?

You can write to the bank directly and submit the documents yourself, or you can get a private lawyer to do it for you. If you believe you have a valid claim and the bank rejects it, then you can appeal. And if you think the bank is not being fair, you can report the bank to the Financial Ombudsman. So far, these claims are taking from 6 to 8 months.

If you want to find out how to get returns on your savings with a social justice product, 11Onze recommends Litigation Funding.

Interest rate hikes by the European Central Bank (ECB) and the tightening of conditions for accessing financing have led to a fall in the number of mortgages taken out in 2023. Even so, this year is expected to see a change of cycle in mortgage loans, whether they have fixed or variable rates.

Despite the fall in the Euribor in the final stretch of the year, dropping to 3.724% in December, after reaching annual highs of 4.22% in September, 2023 has been a year of slowdown in the mortgage market. Up to October – the last month with data provided by the National Statistics Institute (INE) – 323,988 mortgage loans had been contracted, while in the same period of 2022, the figure rose to 393,730 mortgages. A reduction of 17.7% from one year to the next, which accumulated three consecutive months of falls of more than 20%.

Real estate agencies and the banks themselves, which have advanced data concerning the official statistics, point out that mortgage production has recovered slightly in the last three months of the year, helping to cushion the fall in the mortgage sector. Nonetheless, the uptake on mortgages is expected to have declined by 15% compared to 2022.

Hikes in mortgage interest rates to highs of 3.32% not seen since 2015, together with the tightening of the criteria and conditions applied to grant mortgages due to the fear of default, have slowed down a real estate market in which the number of home sales and purchases has been falling for months, while prices have remained stable.

Improve conditions, settle or cancel

Analysing the historical data provided by the Bank of Spain over the last three years, we see that mortgage costs have shot up disproportionately. While at the end of 2021, the APR was 1.5%, a year later it reached 3.12%, starting 2023 at 3.37% and reaching 4% during the last part of the year.

In this context, many families have tried to improve the conditions of their mortgages, either through their bank, moving the loan to another financial entity or cancelling their mortgage to sign a new one. According to data from the real estate portal idealista, in the last four months of 2023, contracting of new mortgages to improve the conditions of existing mortgages has accounted for more than 10% of the total, exceeding 20% during August and October, four times more than they represented in 2021 and at the beginning of 2022.

Likewise, mixed mortgages have shot up to the detriment of fixed and variable mortgages. These establish a fixed-rate monthly payment during the first years, while the rest of the loan term is determined by a variable interest rate. This type of mortgage loan is very similar to variable-rate mortgages but includes some special conditions.

On the other hand, some households have taken advantage of the rise in interest rates to repay their loans early, either partially or in full, to save interest over the life of the mortgage. Although a priori it is a good idea to take advantage of money saved to repay or reduce a mortgage loan early, everything will depend on the repayment conditions that have been signed in the mortgage contract.

Euribor consolidates a sharp decline

The Euribor closed December at 3.679%, dropping below 4% for the first time in the last six months and representing the biggest monthly fall in 14 years. Four days into the new year, it stands at 3.54%. If it closes the month like this, it would be the fourth monthly fall in a year and those mortgages reviewed every six months will experience a reduction in the instalment.

Although the European Central Bank has not made any official announcement, experts predict that the Euribor, the reference rate for most mortgage loans in Spain, will remain below 4% during 2024. This is based on the prediction that the ECB’s rate hikes have already come to an end and what we would see in 2024 would be the first cuts.

This lower mortgage rate would make new mortgages cheaper. As for current mortgages, these are still experiencing an increase in their annual repayments due to the annual review, as the Euribor is still higher than it was a year ago. Even so, from the second quarter onwards, if this trend continues, reductions will be seen in mortgage payments with annual revisions, which tend to be the majority.

If you want to find out about a home insurance policy that’s right for you and for society, check 11Onze Segurs.

Credit or debit cards are known as “plastic money”. Today, there are more than 2.8 billion of them in circulation in the world. Beyond the environmental impact they cause, in this article we explain how to avoid having your wallet stolen.

We have already told you about the origin of the credit card in La Plaça. Many years have passed since McNamara’s famous idea and the techniques that thieves use to steal money from the card have also evolved. So, if you haven’t switched to virtual cards and still use the so-called “plastic money”, here are four tips to avoid being taken for a ride.

- You are the one who has to swipe your card through the dataphone. If you buy in a shop, never let the salesperson take the card and you cannot see the dataphone. There are many card copiers that, just by swiping the card, copy all the data. It is therefore important that you are the one who swipes the card over the dataphone.

- Make sure that the device does not have any strange wires. If you swipe your card yourself, especially if you are not making a purchase at a trusted merchant, make sure that there is no device, large or small, connected to the dataphone. Nowadays, there are many devices that connect to the dataphone and can also copy data. Therefore, if the device is not wireless, check that only a cable is hanging from it.

- Do not make purchases using WIFI or public computers. WIFI networks and public computers have made the internet accessible to everyone, but virtual shopping is best done with your personal computer and from your home WIFI. Encourage safe shopping.

- Avoid ‘fishing’. Finally, avoid so-called ‘fishing’ whenever possible. Whether by phone call or e-mail, some thieves have specialised in asking for your card details with the excuse that they need them for a service you have contracted. Do not give out any personal or financial information except through the service’s corporate intranet or in the shop itself.

Plastic money

It is clear that online shopping is becoming more and more widespread among all of us. It saves us from having to travel to go shopping and we can do it at any time and moment of the day, whether it is near or on the other side of the world. How safe is it to pay via the Internet?

In general, online payment is very secure. Its security has improved a lot since its use became widespread. The need to offer security to buyers led to a lot of resources being invested to implement improved web security systems, and the result is that nowadays, buying a product over the Internet is as secure as or more secure than buying it in a physical store.

This security also depends, to a great extent, on the caution of the user himself. Some recommendations in this regard may be from having a good antivirus on the computer, to check security protocols and data encryption, or even buy in known or trusted places.

For users less experienced in online shopping there are several payment methods that provide added security, making the risk of buying online virtually zero. The most important thing in online sales is that the buyer can have the guarantee that no one can, as a result of a particular transaction, impersonate his personality in the future by making other purchases in his name and at his expense. There are several ways to pay for online purchases with added security:

- Payments with the PayPal system. PayPal is one of the most popular and secure platforms for making transactions. It is not only useful for making purchases, it can also be used to make money transactions between individuals. This platform acts as an electronic intermediary through the user’s credit or debit card, with the objective of ensuring confidentiality, both for the seller and the buyer, and offering the guarantee that the commercial transaction is carried out satisfactorily. This platform has the advantage that if the customer has any problem or does not receive the purchased item in the proper conditions, a claim can be made, which will initiate an investigation by the Paypal platform, which in most cases will end up giving the buyer the reason and returning the amount of the purchase.

- Cash on delivery payments. This system has been used for a long time in purchases that do not necessarily have to be online, although it is not very widespread in online shopping. It is the only means of payment used in e-commerce that involves the use of cash. By doing so, the only information the buyer has to provide to the seller is his personal data and postal address. It has the disadvantage that the buyer has to be present when the shipment arrives to make the corresponding payment, unless a notification arrives to pick up the item later at a delivery office. This system guarantees delivery of the item at the time of payment. From the seller’s point of view, this means of payment entails a delay in collecting the money for the item sold, and the need for physical collection of the money by the person making the delivery.

- Charges on bank account. Some platforms offer this type of payment, but it is not widely used in online commerce. In this case you buy what you need online and give your bank details, nowadays it is usually the IBAN number, and the seller makes the charge directly to the current account provided. It is usually used for periodic charges or subscriptions.

- Debit or credit cards. Debit or credit cards are the most popular means used in e-commerce. For the buyer it means, in the case of using his debit card, the immediate payment at the moment of making the transaction, or in the case of using his credit card, his deferred payment for the end, or in the surroundings, of the end of the month. For the seller, this means quick payment in exchange for a small commission deducted by the drawer’s bank from the amount to be charged for the sale of the item.

- Pay later. Some Internet platforms, in collaboration with financial institutions, advance the money for the purchase, which will be charged in monthly installments, generally charged to the debit or credit card, during the term chosen. These services act as intermediaries between the seller and the user and therefore no sensitive information is shared with third parties.

- Exclusive accounts linked to debit cards. This option is one of the safest that the buyer can use to protect his bank accounts. The user has to ask his bank for an exclusive account to make online purchases and request a debit card associated with this account. The buyer, every time he wants to purchase a product, will have to transfer the amount to be paid to the online seller, to this exclusive account, and then pay using the card linked to where he wants to make the online purchase. In this way, the user can be sure that, even if his card data is compromised, the bank account to which it is associated does not have a balance to make the corresponding payment.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

If you liked this article, we recommend you read:

After going up by almost 7% during October, gold prices continue the upward trend seen during the last quarter, thanks to geopolitical tensions and a weakening dollar on expectations that the US Federal Reserve will stop raising interest rates.

Gold prices started the month of October on a downward trend, after having fallen during September, but the outbreak of a new armed conflict between Palestine and Israel pushed the price of the golden metal up by more than 10%, surpassing the mythical figure of 2,000 dollars per ounce and compensating for the losses that had occurred since the highs of May.

Today, 22 November, gold continues to break through the $2,000 barrier, boosted by the latest monetary policy announcement at the US Federal Reserve meeting earlier this month, which suggests that interest rates have peaked, and precludes a cautious approach to further hikes.

Gold Patrimony

With inflation slackening, Federal Reserve officials therefore agreed that interest rates would only have to rise if insufficient progress was shown in reducing inflation. In this context, the dollar hit lows not seen for more than two and a half months, inversely proportional to the value of gold.

Financial market experts agree that the Federal Reserve will end interest rate hikes and start cutting rates in the first half of 2024, encouraging a revaluation of gold. Marko Kolanovic, head of markets at JPMorgan, advises investors to bet on safe-haven assets such as gold and bonds as tensions in the Middle East escalate, while Goldman Sachs forecasts a rise in commodity yields, such as gold, over the next 12 months.

Protect yourself from economic crises with the ultimate safe-haven asset: gold. If you want your savings to keep or increase their value, Gold Patrimony.

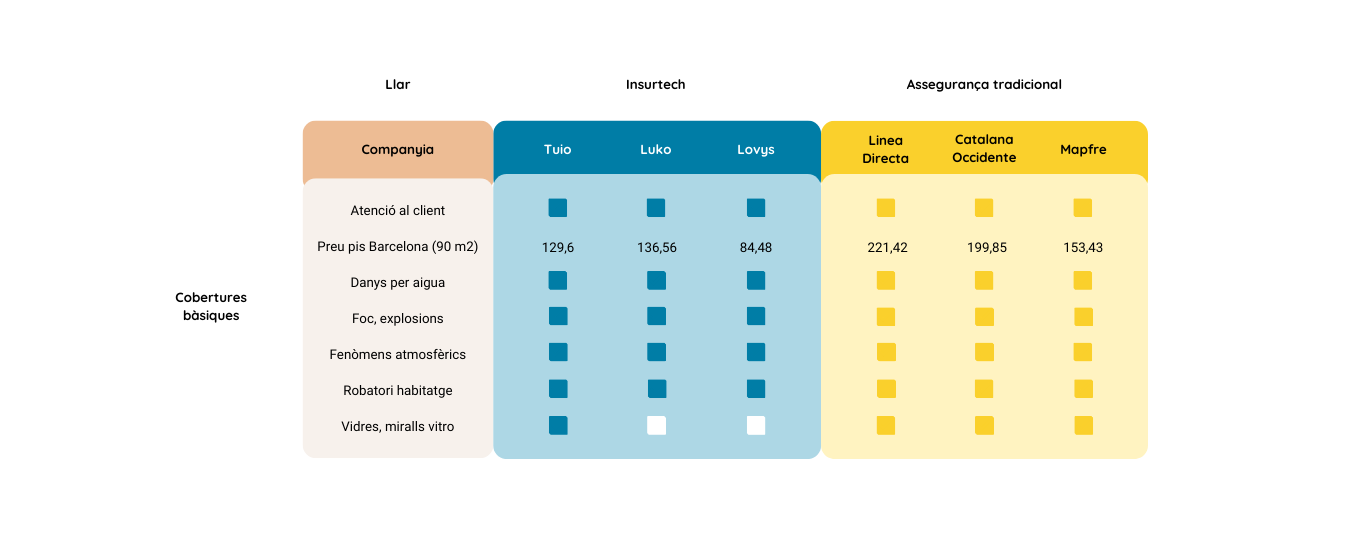

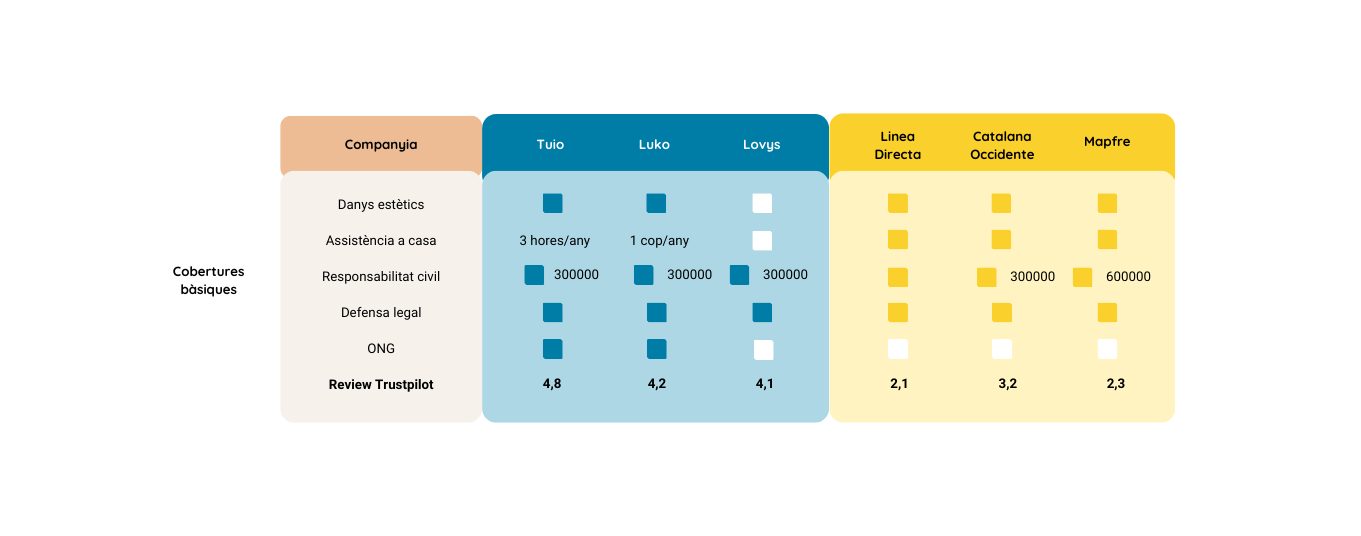

Everyone agrees that a good home insurance provider should offer good coverage options, transparency, impeccable customer service and fair prices. However, the reality of the market is far from this almost utopian vision. The new, fully digital insurers have arrived with the intention of modernising the sector. We compare coverage and prices from various providers to help you choose the best option for your particular circumstances.

According to Unespa data, almost 80% of Catalan households have insurance that protects them in the event of a claim, surpassing even the popularity of car insurance. In this case, only 76% of Catalans have an insured vehicle, possibly due to the concentration of population in urban centres, where private cars are not so necessary. This means that around 20% of homes do not have insurance to protect them against a possible claim.

A study published by ICEA indicates that the average cost of a home repair is around 200 euros, while a policy can cost, on average, 140 euros per year. And it should be borne in mind that other mishaps, such as a burglary or damage to third parties due to a water leak, can push up the repair or loss figure considerably.

Therefore, when comparing insurance, it is important to bear in mind the transparency and scope of cover to avoid last-minute surprises. The reality, however, is that often the complication of small print and paperwork makes it difficult for us to know what coverages we are taking out and to what extent our insurance protects us. This is precisely why insurtechs are taking advantage of the digital transformation to simplify this procedure, adjust prices and offer policies that are better adapted to the needs of each client.

11Onze Segurs.

Most common coverages and claims

The price of insurance depends on several factors: the year of construction of the property and the square metres it has, as well as the location, the number of people living in the home or whether we insure only the contents or also the building can substantially vary the premium of the policy. Even so, there are some basic concepts of coverage that should be included in any insurance policy, regardless of the price.

The covers most requested by clients tend to coincide with the most common claims. Thus, burglary, damage caused by water leaks, and the repair of household appliances should be among the essential covers of an insurance policy. Even so, it is important to bear in mind the differences that can be found between the insurances that offer these coverages. For example, do they include a home assistance service, do they cover labour in the event of repairing electrical appliances, aesthetic damage?, glass?

These details are significant and can make the difference between the small inconvenience of having to claim an incident from the insurer who pays for the costs, or finding out that we have to cover a significant part of the charges out of our pocket. In the comparison table below, we present a compilation of some of the best policies on the market, including new digital insurers that even consider their impact on society by investing a large part of their profits in NGOs of your choice.

If you want to discover fair insurance for your home and for society, check 11Onze Segurs.