China buys gold and sells US treasuries

While China’s demand for gold has risen 68% year-on-year in the first quarter of 2024, pushing prices to record highs, the Asian giant continues to trim its holdings of US Treasuries.

Gold had another good month in April with a 4% gain, ending the month at $2,307 per ounce. According to the latest World Gold Council (WGC) report, Chinese purchases, mainly attributed to an influx of retail investors, and central banks, appear to be the main drivers of demand.

China has accumulated over 300 tonnes of gold worth $561 billion in the past 18 months alone. China’s official gold reserves have increased for 16 consecutive months. The addition of 12 tonnes in February brought its total to 2,257 tonnes, 4.3 per cent of the country’s foreign exchange reserves. Moreover, the GWC notes that China is inspiring other BRICS nations to buy the precious metal as a reserve to the detriment of the US dollar.

However, the official figures for its gold reserves remain absurdly low, since unlike many central banks that report their gold purchases to the IMF every quarter, central banks in China, Russia and other countries buy and store gold without declaring it as reserves.

China sheds more US debt

Although China has purchased large amounts of US Treasury bonds in recent decades – in January 2024 the Asian nation accumulated some $797.7 billion in US Treasuries, roughly 10% of the US national debt – it has sold more than $74 billion of this debt in the past year, according to Treasury Department data, $22.7 billion in February alone.

China is intentionally minimising its exposure to the dollar. Concerns about geopolitical tensions and the use of economic sanctions by the United States as a tool in its trade war, along with the further postponement of the Federal Reserve’s planned interest rate cuts, continue to dampen Beijing’s appetite for US Treasury bills. Thus, the Asian giant has gone from holding $849 billion to $775 billion between the beginning of the second quarter of 2023 and the second quarter of 2024, reaching its lowest level since 2009.

The data was published at the same time Sergey Lavrov, the Russian foreign minister, said that Russia and China use virtually no dollars in their trade transactions. According to Lavrov, currently, more than 90% of trade between the countries is conducted in their national currencies.

Moreover, China and Russia, the two founding members of the BRICS alliance, plan to trade $260 billion without using a single US dollar and have long been trading in yuan with other countries, such as the Philippines, the Arab Emirates, Japan, Malaysia, Thailand and Tajikistan, accelerating a process of de-dollarisation that seems unstoppable.

Preciosos 11Onze makes it easy to buy gold, at the best price and with total security. Give us a call and speak to one of our agents without any obligation to clarify any doubts you may have and protect yourself from economic crises with the ultimate safe-haven asset: gold. If you want your savings to keep or increase their value, Gold Patrimony.

The timid reaction of Spanish banks to reflect the ECB’s interest rate hike in the remuneration of savings means that profitability is not in bank deposits but in investment.

High inflation continues to erode savings left in the bank. Despite the fact that on 4 May the ECB raised interest rates again, for the seventh time since July 2022, bank customers are receiving an improvement in the remuneration of their deposits in dribs and drabs.

This has led to a deposit flight by many families who have decided to diversify their savings by taking their money out of banks in favour of other products and investments that offer a higher return. This situation has been aggravated by fears about the safety of deposits due to the string of bank collapses in recent months.

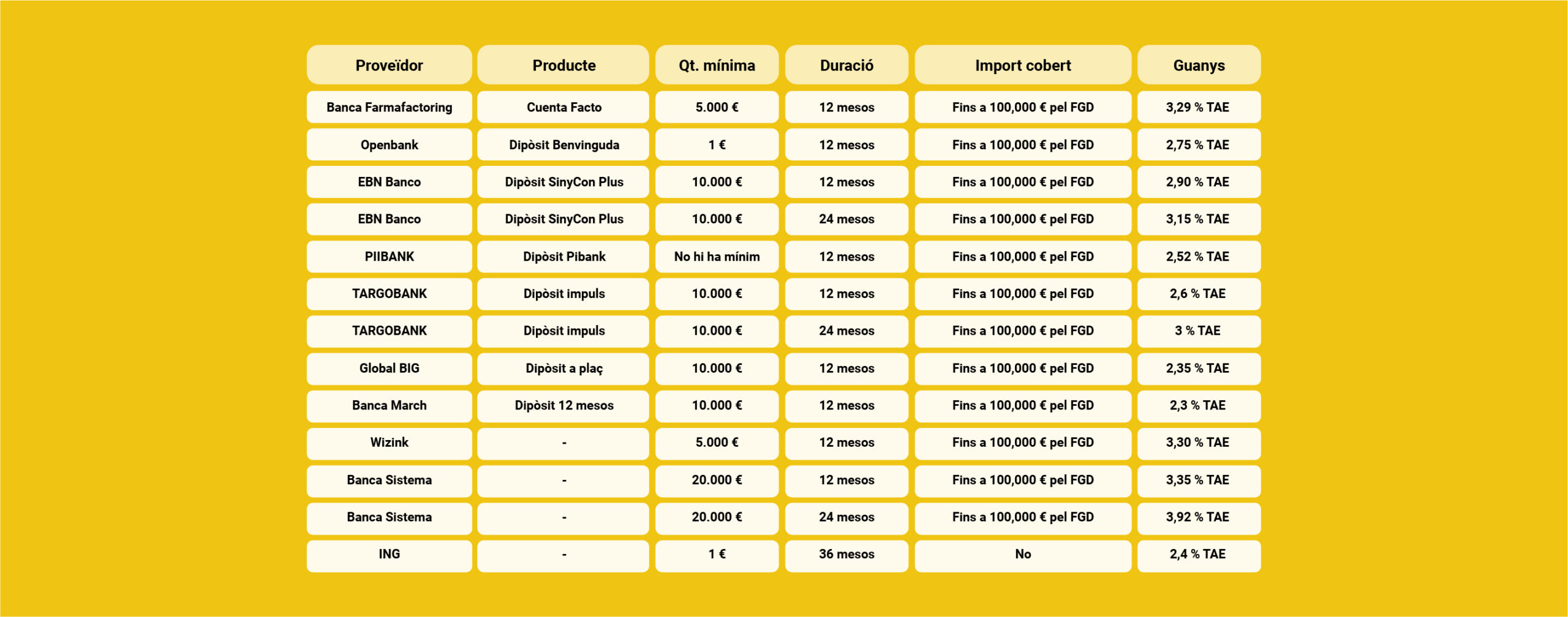

In Spain, the best deposits give a yield of almost 4%, which means that in the best of cases, they do not compensate for the deterioration caused by the current inflation rate of 4.1%, or even less if we take into account accumulated inflation. Nevertheless, we have prepared a comparative table with the most profitable deposits currently offered by banks.

Are there better options for increasing the return on my savings?

What would you think of earning between 9% and 11%, contributing a minimum capital of just €10,000, in a low-risk product that incorporates high quality insurance. It doesn’t seem possible, does it? If you want to find out how to make money on your savings with a social justice product, 11Onze Recommends Litigation Funding.

Litigation Funding

Fund lawsuits against banks. Get justice done and returns on your savings above inflation thanks to the compensation the banks will have to pay. All the information about Litigation Funding can be found at 11Onze Recommends.

If you liked this article, we recommend:

Economy

EconomyLitigation Funding: high returns & social justice

3 min readLitigation Funding, which 11Onze Recommends, is simplified...

The volume of transactions in the precious metal par excellence has exceeded 150 billion euros per day over the last twelve months, making it the most traded financial asset after currencies. Despite record highs in its price, investors are more active than ever in gold trading.

The intrinsic value of gold, which carries no credit risk, cannot be inflated, and has remained unchanged throughout history, has made it the safe-haven asset par excellence for investors in times of economic uncertainty and makes it particularly attractive when it comes to diversifying and making our savings profitable.

This characteristic has made gold more popular than ever in the economic and geopolitical context we have been experiencing in recent years. The price and demand for the golden metal have reached record highs over the last two years and show no sign of abating in 2024.

Global gold demand held firm in the first quarter of the year, rising 3% year-on-year to 1,238 tonnes and marking the strongest first quarter since 2016, the World Gold Council (WGC) announced.

More liquidity than other markets

The gold market is large, global and highly liquid. The WGC estimates that investors’ and central banks’ holdings of physical gold amount to approximately 4.7 trillion euros, to which must be added 0.9 trillion euros in open interest through derivatives traded on exchanges or over-the-counter (OTC).

“The gold market is more liquid than virtually any other financial asset,” the WGC notes. This is demonstrated by the very high trading volumes of this asset, which according to WGC data in the last twelve months have exceeded 150,000 million per day, 139,000 million on average over the last five years.

Moreover, gold trading volumes have surpassed those of German bonds and US debt. Only the S&P 500 stock index accumulates a higher trading volume: 195 billion per day on average over the last five years. As well as the global foreign exchange market, which plays in a different league and exceeds 6 trillion euros per day.

This gold boom on the international markets, thanks to the growing demand from central banks, speculative investment and the interest of individuals who want to protect their savings in the current economic context, leads many analysts to believe that the gold rush still has a long way to go.

Preciosos 11Onze makes it easy to buy gold, at the best price and with total security. Give us a call and speak to one of our agents without any obligation to clarify any doubts you may have and protect yourself from economic crises with the ultimate safe-haven asset: gold. If you want your savings to keep or increase their value, Gold Patrimony.

Has managing the family finances become a nightmare? Do you not know how to share money with your partner? Does the anguish bite you when you realise that you haven’t saved anything? Perhaps your relationship with money is not healthy enough. When this happens you probably need some good financial therapy. Head of agents Lara de Castro, who is also a professional coach, gives us some clues in a new Territori 17 of La Xarxa.

“Financial therapy addresses the link we have with money, when it is not very aligned with what we want in life, when it has a negative impact on our reality,” De Castro summarises. There are many scenarios where financial therapy can be useful. The clearest example is that of all those people who have the habit of making impulsive purchases and, little by little, fall into compulsiveness. Financial therapy can help us to answer what is behind these compulsive purchases and how to deal with a possible lack of money due to debts we have incurred.

“Many decisions we make often go through unconscious circuits,” the head of agents warns. And its effects extend to many spheres of our private lives, including our relationships. “When we share a bank account, the income comes from two different sides. When we spend from that shared current account and we don’t tell our partner or we don’t comply with the agreed planning, the other can interpret it as financial infidelity,” Lara de Castro.

Want to go deeper into the reasons why you might need financial counselling? Who can you ask for help? Listen to the whole conversation below!

La Plaça – Territori 17: Financial infidelity

If you want to discover the best option to protect your savings, go to Preciosos 11Onze. We will help you buy at the best price the ultimate safe haven asset: physical gold.

Personal Income Tax (IRPF) is a personal and direct tax that plays an essential role in tax collection and the redistribution of wealth. It is a State tax partially ceded to Catalonia, but what are its origins?

We are in the middle of this year’s income tax return campaign, which runs from 11 April to 30 June and which more than 23 million taxpayers will have to complete. Almost everyone knows how to do it and understands the concept of this tax based on the balance of income and expenses we have had during the previous year. What some people may be unaware of, are the origins of this tax and its evolution throughout history.

The first general tax system

Although personal income tax (IRPF), as we know it today, is a relatively recent tax, approved in 1978, its origins date back to the 19th century.

The first income tax dates back to 1845, when the first general tax system was established as a consequence of a tax reform promoted by Alejandro Món and Ramón de Santillán, which simplified the existing tax system and brought about a broad tax unification throughout Spain.

The reasons behind this reform were to remove obstacles to economic growth in the context of industrialisation and a liberal revolution to replace the absolute monarchy of the Ancien Régime. Thus, classic taxes such as tithes and alcabalas were eliminated.

Tax reform during the Second Republic

One of the first modern attempts to impose a personal income tax in Spain took place during the Second Republic (1931-1939). During this period, under the government of Manuel Azaña, a new tax was introduced by the Minister of Finance, Jaume Carner.

The Carner Law, better known as the general income tax, was passed in 1932 and came into force at the beginning of 1933. Although its application was limited and was diluted after the Civil War with Franco’s dictatorship, it included a tax on individual income that set the precedent for what would later be known as IRPF.

The transition and the Moncloa Pacts

It was not until 1977, as a result of the agreements signed at the Moncloa Palace during the Spanish Transition, also known as the Moncloa Pacts, that the foundations of the contemporary tax system were established. Thus, in 1978, the first modern personal income tax was created with a broad political consensus.

This law established the basis for personal income taxation with a progressive tax system, where high incomes paid a higher percentage of tax. In this case, it had 28 brackets and its tax rates were as high as 65.5%. It was a tax that affected all persons with incomes over 300,000 pesetas.

Well into the 1980s, the way of filing a tax return stayed mostly the same, but with the development of new digital technologies, new access channels were added to carry out this tax activity, up to the current possibility of filing the tax return online. It also evolved significantly, incorporating several new features, such as the transfer of 50% of the tax to the autonomous communities.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Driven by geopolitical and economic uncertainty, global gold demand remains firm in the first quarter of the year, reaching its highest level in eight years on a year-on-year basis, according to the latest WGC report.

Global gold demand (including OTC purchases) during the first quarter of the year was up 3% year-on-year to 1,238 tonnes, marking the strongest first quarter since 2016, the World Gold Council (WGC) has announced in its latest Global Demand Trends report.

The strong performance in gold demand comes as persistent central bank buying on the back of geopolitical and economic uncertainty, investment in the OTC market, and increased demand from Asian buyers have driven the gold price in the first quarter to a record average of €1,934 an ounce.

As a reminder, there are two main ways to trade gold in the wholesale market: the over-the-counter (OTC) market and the exchange market. OTC markets are characterised by the fact that market participants trade directly with each other.

Excluding the OTC market, gold demand fell by 5% to 1,102 tonnes in the first quarter, as the jewellery market declined by 2% – although still resilient in the face of record prices – and physical gold-backed exchange-traded funds (ETFs) declined by 114 tonnes. In particular, Europe and North America recorded quarterly outflows, slightly offset by inflows into listed products in Asia.

Increased central bank purchases

Central banks continue to hoard gold at a frenetic pace. During the first quarter, they added 290 tonnes to their reserves, up 1% year-on-year and 69% more than the quarterly average of the last five years.

This is the strongest start to the year in the WGC’s historical series, which dates back to 2000. This increase in gold purchases is led by the central banks of China and India. The Asian giant generated most of the demand. Both Chinese consumers and their central bank are buying gold with renewed investor interest due to the weakening of the local currency and the poor performance of domestic equity markets.

Louise Street, Markets Analyst at the World Gold Council, noted, “We are witnessing shifting behaviour trends from Eastern and Western investors. Typically, investors in Eastern markets are more responsive to the price, waiting for a dip to buy, whereas Western investors have historically been attracted to a rising price, tending to buy into the rally. In Q1, we saw those roles reversed, with investment demand in markets such as China and India growing considerably as the gold price surged.”

However, the WGC expects central banks to slow their purchases slightly in 2024 compared to the previous year. Krishan Gopaul, senior analyst at the WGC, told Reuters, “While central bank buying momentum continues, we are taking a cautious view going forward, waiting to see if recent gold price growth prompts some central banks to slow purchases or some to sell some of their holdings.”

Preciosos 11Onze makes it easy to buy gold, at the best price and with total security. Give us a call and speak to one of our agents without any obligation to clarify any doubts you may have and protect yourself from economic crises with the ultimate safe-haven asset: gold. If you want your savings to keep or increase their value, Gold Patrimony.

Inflation, the low-interest rates offered by banks and the fear of a banking crisis continue to fuel a deposit flight towards safer and more profitable securities such as gold or Treasury Bills.

As we have been warning for months, the rise in ECB interest rates has not been reflected in a significant improvement in the remuneration of savings. During the first two months of the year, Spanish bank customers withdrew 18 billion in deposits from their savings accounts in search of a better return on their money.

The rising cost of living due to inflation has led to a loss of purchasing power for many families who have decided to diversify their savings by taking their money out of banks in favour of other products and investments that offer a better return on their money. A fact that largely explains why the demand for precious metals, especially gold, is still booming.

The case of Spain is not unique, the low profitability of bank deposits has been compounded by the fear of a new crisis caused by the bank collapses of recent months, which has led to a deposit flight in many parts of the world. Moreover, if this accelerates because of fears about the safety of deposits, the banks concerned will reduce the assets on their balance sheets, lending less and restricting credit to individuals and businesses.

A globalised deposit flight

The United States is one of the countries that has seen the greatest reduction in deposits, especially to higher-yielding investment funds. After the collapse of Silicon Valley Bank and Signature Bank, Federal Reserve data showed that between 1 and 15 March deposits worth 146 billion euros were withdrawn. A figure that rises to 574 billion euros if one looks at the evolution of the loss of bank deposits over the last year.

The picture is also worrying in the United Kingdom, where news of the collapse of US banks and Credit Suisse caused Britons to withdraw 5.5 billion euros from their bank accounts in March, the largest-ever drain of deposits.

The European Union’s largest economy was not spared from the outflow of deposits. Continuing with data from March, Germany is another country where banks have experienced a significant drain of deposits. Germans withdrew 18 billion euros from their banks, either because of fear of the banking crisis or because they were looking for higher returns in other financial institutions or investment products.

Concern about the safety of money in banks

Not surprisingly, in the midst of the turmoil in the US banking system, 48% of Americans are concerned about the safety of their money in banks. This sentiment, however, is not limited to the United States but is widespread throughout other Western countries whose economies are interconnected to the American giant.

The situation is so serious that the Japanese Finance Minister, Shunichi Suzuki, has announced that at this week’s meeting with the G7 group of nations, measures will be considered to try to stop the flight of bank deposits. In addition, the latest bank failures have called into question the degree of deposit protection. In this regard, the European Commission has adopted an emergency proposal to strengthen existing deposit insurance in the EU, with a particular focus on small and medium-sized banks.

Governments and regulators keep repeating that we do not have to worry about our money and the stability of the financial sector. Yet there seems to be no turning back, the lack of confidence in banks has been accentuated by the domino effect of the banking collapse, and the data shows that people have decided to look for other options in order to protect their savings.

Protect yourself from economic crises with the ultimate safe-haven asset: gold. If you want your savings to keep or increase their value, Preciosos 11Onze.

The 1980s on Wall Street was a decade of big personalities, big bonuses and a culture of excess that was accompanied by a meteoric rise in drug trafficking. The pressing need to launder large amounts of drug money led to collaboration between banks and criminal organisations.

To the banks and drug cartels, Bob Musella was a wealthy American businessman dressed in Armani who owned a chain of jewellery stores and ran an investment company from Miami. What they didn’t know was that he was Robert Mazur, an undercover DEA (Drug Enforcement Administration) agent who would eventually bring down drug lords and corrupt banks in one of the most successful anti-money laundering operations of all time.

“Miami is the crossroads of the international drug trade and this is where I did a lot of my business,” said Robert Mazur. With the help of two informants connected to a New York Mafia family and another based in Medellín, Colombia, Mazur mounted the most sophisticated undercover anti-money laundering operation ever conducted.

The evidence he gathered from this operation, known as C-Chase, was key for the US Senate Foreign Relations Subcommittee, led at the time by Senator John Kerry, to legitimise the closure of the Bank of Credit and Commerce International (BCCI), controlled by the Pakistani, Agha Hasan Abedi, which was dedicated to laundering money for the Medellín Cartel, led by Pablo Escobar.

The BCCI and the Medellín Cartel

To launder all this drug money, a series of companies were created with the help of some banking institutions, including BCCI. It was the seventh-largest private bank in the world, its reserves exceeded 20 billion dollars, and it had offices in 78 countries, including Spain.

According to US Customs documents, BCCI agents in Panama knew that the money came from drug trafficking by Colombian drug lords. They contacted Musella in December 1987 to suggest ways of laundering the money in several meetings in Miami, Paris, and London.

Law enforcement and investigative authorities nicknamed it the “International Bank of Thieves and Criminals” because of its penchant for serving customers who trafficked in guns, drugs and dirty money. Initially, the bank denied the charges, arguing it was a “malicious campaign” against the institution.

However, US and UK investigating authorities found that BCCI had been “deliberately set up to avoid centralised regulatory review, and operated extensively in secrecy jurisdictions”, adding that “its executives were sophisticated international bankers, the apparent aim of whom was to keep their affairs secret, commit large-scale fraud and avoid detection”. The entity was forced to cease all operations and shut down its business.

Fund lawsuits against banks. Get justice and returns on your savings above inflation thanks to the compensation the banks will have to pay. All the information about Litigation Funding can be found at 11Onze Recommends.

What is the SWIFT code and why is it so important in the financial world? What are the implications of expelling a country’s financial institutions from this banking messaging network? Iu Alemany, 11Onze’s Back Office and Customer Service Manager, reveals all the keys.

SWIFT stands for Society for World Interbank Financial Telecommunication, “a cooperative society based in Belgium that was founded in 1973”, as the 11Onze Back Office and Customer Service Director explains. Alemany points out that it is not a payment system, but a messaging system, which speeds up international transfers and “allows the parties involved to be identified in a standardised, secure and error-free manner”.

Some 12,000 institutions in more than 200 countries, both financial and non-financial, are connected through the SWIFT system, which facilitates “some 32 million messages on average” to be exchanged every day.

The SWIFT code normally consists of eleven characters, although sometimes it can be as few as eight. The first four letters identify the bank or institution. The next two letters indicate the country. The next two correspond to the location of the institution, for example, “BB would mean Barcelona”, as Alemany explains. And the last three digits identify the bank office or branch. In this case, “if three ‘Xs’ appear, it means that the branch carries out the settlement centrally”, explains the 11Onze’s Back Office and Customer Service Manager.

Iu Alemany talks to us about the SWIFT code.

A tool for political pressure

Seven Russian banks were excluded from the SWIFT system in March to put pressure on Russia with its conflict with Ukraine. As Alemany explains, cutting off communication between a country’s banks and the rest of the global financial system makes it impossible for that country to carry out “most of its financial transactions around the world, blocking exports and imports”. Ultimately, the aim is to hinder “its ability to operate globally”.

Iran was excluded from the SWIFT system in 2012 as part of sanctions over its nuclear programme. As a result, it lost almost half of its oil export revenues and 30 per cent of its exports. And Russia had already been threatened with this measure in 2014, when it annexed Crimea.

Iu Alemany warns that this measure could be detrimental in both ways, not only for the sanctioned country: “If we are thinking of applying this measure to a strong economy, highly interconnected to the rest of the world and which has a series of basic products for the rest of the world, we must be careful”.

As we explained in the article “SWIFT: use and abuse of an alphanumeric code”, the exclusion of some Russian banks from the SWIFT system will be an incentive for China, Russia and even the European Union to look for alternative systems that can shield their economies from this political pressure measure.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

Are you preparing your tax return? Have you taken into account all the deductions you can take advantage of? From 11Onze we detail eleven deductions that allow some type of saving when it comes to sorting your accounts with the Tax Agency.

In the income tax return we can take advantage of various tax deductions depending on the type of taxpayer we are, whether we are an individual or a legal entity. It should be borne in mind that, as well as state deductions, there are also regional deductions, depending on the autonomous community where you live and work. In the case of Catalonia, the Tax Agency provides the relevant information on its website.

It is important to bear in mind that deductions are limited by age, income, and other circumstances. Therefore, we cannot forget to read the small print. Having said that, here are the main state and regional deductions that are in force:

1. For large families or disabled dependents.

As detailed by the Tax Agency, among the state deductions for families, there is the specific one for large families, which is 1,200 euros for three children, 1,800 euros for four children, and 2,400 euros for five children. Even so, in some cases, a deduction of 1,200 euros can be applied for each of the descendants or ascendants with a disability or a spouse who is not legally separated and has a disability. These last deductions are only applicable if the annual income does not exceed 8,000 euros.

2. For maternity, birth, or adoption

Working mothers can apply a deduction of 1,200 euros per year for each child under the age of three, provided that they live with them. Childcare expenses can increase this amount by up to 1,000 euros. For residents in Catalonia, a deduction for birth or adoption of 300 euros is recognised in the case of a joint declaration by the parents, or 150 euros for each of the parents if this is done individually.

3. For donations to foundations and associations declared to be of public utility

Donations to NGOs, foundations, and public research bodies dependent on the General State Administration have deductions ranging from 10% to 80% of the amounts paid. At the regional level, deductions are also available for donations to organisations that promote the use of the Catalan or Occitan language, as well as for entities that promote Y+D+Y and environmental conservation.

4. For membership fees and contributions to political parties

A deduction of 20% is applied for membership fees and contributions to political parties, federations, coalitions, or groups of voters, with a maximum limit of 600 euros per year. It should be borne in mind that contributions made once you have ceased to be a member do not form part of the base on which the aforementioned deduction has to be calculated.

5. For investment in new or recently created companies

It is possible to deduct 30% of the amounts paid for the subscription of shares in new or recently created companies. The maximum deduction base will be 60,000 euros per year and will be formed by the acquisition value of the shares or holdings subscribed.

6. For building work to improve the energy efficiency of housing.

There are three types of possible deductions:

- Deduction of 20%, with a maximum of 5,000 euros, for reforms to improve the energy efficiency of a property that reduces energy consumption by at least 7%.

- Deduction of 40%, with a maximum of 7,500 euros, for improvement works that reduce the consumption of non-renewable primary energy by 30%.

- Deduction of up to 60%, with a maximum of 15,000 euros, for home improvements that reduce the primary energy consumption of a residential building by at least 30%.

7. For renting the main residence

These are deductions under a transitional regime and are to be abolished, which only apply if you are the holder of a rental contract dated prior to 1 January 2015. We can deduct 10.05% of the amounts paid in the tax period, provided that the taxable base is less than 24,107.20 euros.

8. For investment in the main residence

As in the previous case, this is a deduction that was abolished in 2013, but which is maintained on a transitional basis for taxpayers who acquired or paid amounts for the construction of their main residence before 1 January 2013. We have to bear in mind that the maximum deduction base for investments in the acquisition, rehabilitation, or extension of the main residence is 9,040 euros per year.

9. For investment by a ‘business angel’ for the acquisition of shares or stock holdings

- Deduction of 30%, up to a maximum of 6,000 euros, on amounts invested during the year in the acquisition of shares or holdings in companies as a result of agreements for the incorporation of companies or capital increases in commercial companies.

- Deduction of 50%, up to a limit of 12,000 euros, in companies created or owned by universities or research centres.

10. For taxpayers who were widowed in 2020, 2021 or 2022

A general reduction of 150 euros can be obtained, and of 300 euros if the person who becomes a widow or widower has one or more descendants who qualify for the application of the minimum for descendants.

11. For income obtained in Ceuta and Melilla

Taxpayers can deduct 60% of the state and regional tax liability corresponding to income obtained in Ceuta and Melilla. This deduction is also applicable for periods of residence in these cities of no less than three years for income obtained outside Ceuta and Melilla if at least one-third of the net assets are located in the aforementioned cities.

If you want to know more about superior options to make your money profitable, go to Guaranteed Funds. From 11Onze Recomana we propose you the best options in the market.