Three basics of managing our money

Sembla obvi, però, per aprendre a administrar els nostres diners, és primordial, primer, que ens els hàgim guanyat. Aconseguir diversificar els nostres guanys és una estratègia que ens pot blindar enfront d’una possible recessió o d’un imprevist. A 11Onze recopilem tres consells bàsics per fer-ho.

En moments d’incertesa és clau saber respondre a: com estalviar, com fer créixer els estalvis i com controlar les despeses. Difícilment serem experts a trobar respostes per totes tres preguntes alhora, però, si entenem els conceptes que s’amaguen rere cadascuna d’elles, tenim moltes més possibilitats de gestionar els nostres diners adequadament. No només aprendrem a cobrir les necessitats bàsiques, sinó que sabrem gaudir-ne i tindrem molt clar quan hem de prescindir d’aquelles que no ho són tant com ens pensàvem.

Estalvi: almenys un 10% dels ingressos

Sovint es diu que l’estalvi és la base principal de l’èxit financer. Tenir diners estalviats és el que ens dona la capacitat de respondre a situacions imprevistes —bé sigui una incapacitat per malaltia o càrrecs inesperats—, començar un negoci o tornar a estudiar. Però és important no confondre l’estalvi amb la inversió: mentre que el primer ens dona tranquil·litat, fins i tot en moments de crisi econòmica global, la inversió pot fer que els nostres estalvis es multipliquin, però també pot ser una font de maldecaps i la causa que perdem la nostra liquiditat.

Un dilema que ens podem trobar és si liquidar el deute o estalviar. Tot dependrà del tipus d’interès que tingui aquest deute. En casos d’interessos alts, com poden ser els de les targetes de crèdit, és generalment preferible deixar aquest deute a zero abans de plantejar-se l’estalvi. Però, en casos en què l’interès del deute sigui baix, com pot passar amb una hipoteca o, fins i tot, un crèdit personal, és raonable estalviar i alhora liquidar el deute lentament.

Creixement lent, risc baix, i a la inversa

Un compte d’estalvi ha estat la manera més tradicional que creixin els nostres diners, sobretot per a la gent més conservadora i poc aficionada al risc. Però, amb interessos relativament baixos i una inflació que ens visita molt més sovint del que seria desitjable, altres formes d’inversió van guanyant terreny, especialment davant d’una clientela cada dia més erudita en temes financers i amb un poder adquisitiu relativament superior a les generacions precedents.

En aquest punt, l’oferta de productes d’inversió és extensa i variada, amb diferents nivells de risc. Cadascú ha de ser conscient dels seus coneixements financers i, sobretot, de la quantitat de diners que s’està disposat a arriscar i perdre, especialment si l’expectativa de creixement és elevada i a curt termini. Cal tenir en compte que un gestor d’inversió pot ser una molt bona opció a l’hora d’escollir un producte financer que millori la rendibilitat dels nostres estalvis d’una manera substancial.

Despeses: necessitat vs. desig

Evidentment, no estalviarem tot el que guanyem, però hem de distingir entre dos tipus de despeses:

- Despeses de primera necessitat. Aquí hi comptem les despeses en el que és bàsic que necessitem per viure, com poden ser el menjar, l’allotjament, els subministraments d’electricitat, l’aigua, el transport públic, entre d’altres.

- Desitjos i productes més superflus. Per eliminació, hi incloem tot el que no és estrictament necessari. Hi trobaríem les compres impulsives, articles de luxe, viatges de lleure, etc.

Fer aquesta distinció no implica que no puguem gastar diners en coses que desitgem, però que no necessàriament ens calen. El desig i les accions que no tenen una finalitat merament pràctica són part de la condició humana. Això és un fet. Per tant, també ens hem de permetre aquestes despeses, sempre que ens adherim a un pressupost preestablert, bé sigui setmanal o mensual.

11Onze és la fintech comunitària de Catalunya. Obre un compte descarregant l’app El Canut per Android o iOS. Uneix-te a la revolució!

Having a deposit in a Spanish bank nowadays means not only getting a low return on our savings, given the low-interest rates, but also being covered by the Deposit Guarantee Fund (FGD). Currently, the FGD has about 4.2 billion euros at its disposal, against the 958.9 billion euros that customers have on deposit.

In 2021, according to data provided by the Bank of Spain, the accumulated level of deposits reached 958.9 billion euros at the end of 2021, a new all-time high. Even so, it should be noted that the level of financial resources accumulated by the Deposit Guarantee Fund, and available in the deposit guarantee systems, amounted to 4,191 million euros in 2020, which represents 0.5% of guaranteed deposits to this date.

Clearly, therefore, the DGF is not in a position to cope with bank failures. The monstrous disproportion between money deposited and guarantee is pushing many savers to look for safer options. Even more so when the benefit obtained by having money in a Spanish bank is negligible, as we analyse in this article. Theoretically, the Deposit Guarantee Fund would have to guarantee up to 100,000 euros per individual or legal entity, but it is mathematically impossible for them to do so because the money reserves are exactly half of what they should be. For this reason, given the context of inflation that bites into savings and seeing the low profitability and security offered by traditional banks, it is necessary to look for safer options for our money.

Guaranteed Funds guarantee 100% of capital

Guaranteed investment funds can be a good option if we want to diversify our savings and, at the same time, ensure a certain return. As the name suggests, they guarantee all or part of the capital invested, as well as a predetermined return for a certain period of time. Normally, these are funds that have insurance that guarantees the totality of the money regardless of the amount.

Therefore, the question to ask yourself is: is there any fund that generates high returns and guarantees 100% of the investment and returns? If you want to find out about superior options for making your money profitable, go to Guaranteed Funds. From 11Onze Recommends we propose the best options.

11Onze is the fintech community of Catalonia. Open an account by downloading the super app El Canut on Android and Apple and join the revolution!

Despite a 10% reduction in the price of raw materials, the CPI for food in Catalonia rises to 4.7%. Experts point out that the sector in Europe is taking advantage of this to pass on part of the cost increases of recent years, and other parts of the chain could be expanding margins.

According to data from the Consumer Price Index for February, food is now 4.7% more expensive in Catalonia than it was a year ago. The statistics from the National Statistics Institute for Spain as a whole are even worse, with food prices rising by 5.3% in February compared to the same month last year.

According to INE, over the last twelve months, the foods that have experienced the biggest rises in Spain are olive oil (67%), fruit and vegetable juices (18.8%), potatoes (11.6%), pork (11%), confectionery (10.8%), chocolate (10%), fresh or chilled fruit (9.1%), salt, spices, and herbs (8.8%), sheep and goat meat (8.1%) and, finally, ice cream (7.9%).

Less supply?

The Spanish government blames part of this price rise on a temporary reduction in supply due to “unfavourable weather conditions” in many EU countries, which is reducing production. In fact, as we indicated in another article, Catalonia is suffering the most severe drought since 2008. And it is true that this winter greenhouses have been closed in several European countries because the price of gas is making them loss-making.

However, this argument is not very solid when it comes to justifying the high prices if we take into account that the data of the FAO (The Food and Agriculture Organization of the United Nations) food price index stood at 117.3 points in February 2024, 0.9 points (0.7%) below its revised January level, and 14 points below its February 2023 level of 131.

Impact of costs

Many analysts point out that the price rises have served to offset part of the increase in production costs suffered by the agri-food sector in recent years. These affect such important items as seeds, fertilisers, animal feed and energy.

Fertilisers tripled in price, although they subsequently became 40% cheaper from spring onwards, when they reached their highest price; it is estimated that feed has risen by more than 80% since 2019; and, as for energy, the price per megawatt-hour reached more than 300 euros and the price of a barrel of Brent oil reached 120 euros.

In any case, it is not clear that higher food prices always translate into higher incomes for producers. In this sense, there is much debate about which actors in the food chain are taking advantage of the situation to increase their margins. What is certain is that even the president of Mercadona, Juan Roig, has just admitted that his chain has raised prices “a huge amount”.

11Onze is the community fintech of Catalonia. Open an account by downloading the app El Canut for Android or iOS and join the revolution!

The gold market is one of the largest and most liquid in the world. Every day, billions of dollars are traded between London, New York, Zurich, Dubai, and Shanghai. It is an asset with more than five thousand years of history, present in central bank reserves and in the portfolios of institutional and retail investors. However, in 2020, one of the world’s largest banks, JPMorgan Chase, admitted to having manipulated precious metals markets for years.

How was it possible to manipulate a market of this magnitude? Are we facing a systemic conspiracy or a more subtle technical mechanism? Understanding the “how” is key to avoiding both naivety and sensationalism.

When we think about the price of gold, we imagine stacked bars inside a vault. But the global price is not primarily determined by the physical metal, but by the financial contracts traded around it.

The reference market is in London, coordinated by the London Bullion Market Association, which sets the “Good Delivery” standard and concentrates a large share of global OTC trading. In New York, the COMEX futures market allows trading contracts with future maturities and plays a key role in price formation through derivatives.

But the map does not end there. Zurich is one of the main global refining and custody centers, hosting some of the world’s largest refineries. Recently, Dubai has consolidated itself as a strategic hub between Africa and Asia, especially in the trade of Dore gold and OTC markets outside the traditional London circuit. In Asia, the Shanghai Gold Exchange has emerged as a key player in the internationalization of gold pricing in yuan, reinforcing China’s growing weight in the physical market.

The global gold price, therefore, is not the result of a single center, but of a dynamic balance between these financial hubs, where physical and derivative markets constantly interact.

The reality is that the volume of futures contracts far exceeds the volume of physical gold that changes hands each day. This phenomenon, often referred to as “paper gold,” means that the price is largely formed in derivative markets. And this is where vulnerability appears.

What is spoofing?

To understand how the gold market can be manipulated, we must first understand how a modern electronic market works. Today, prices are not decided in a crowded trading pit, but on digital platforms where thousands of buy and sell orders compete in fractions of a second.

Each order is recorded in what is called the order book. This book shows, in real time, how many contracts are willing to buy or sell at each price level. It reflects not only executed trades, but also intentions. In financial markets, the perception of intention can move prices just as much as actual supply. This is where spoofing appears.

The 2020 JPMorgan case

In September 2020, the U.S. Department of Justice and the U.S. Commodity Futures Trading Commission demonstrated how JPMorgan Chase and several traders, between 2008 and 2016, carried out systematic manipulation practices in gold, silver, platinum, and palladium futures markets through the technique known as spoofing on COMEX.

The mechanism consisted of placing large buy or sell orders with no real intention of executing them. These orders temporarily altered the visible balance of the order book and created the perception of strong imminent buying or selling pressure. When other participants — algorithms, funds, or traders — reacted to this apparent pressure, the price moved slightly. At that moment, the traders cancelled the false orders and executed real trades in the opposite direction, taking advantage of the generated movement. It was not about controlling the global price of gold, but about gaining an advantage from very brief and repeated distortions in market microstructure.

For these actions, JPMorgan Chase agreed to pay approximately 920 million dollars in penalties, while several involved traders were criminally convicted. It was not a suspicion or a speculative theory: it was a judicial resolution with economic and criminal consequences.

Manipulation is not control

The JPMorgan Chase case proves that manipulation is possible, but it also forces us to set boundaries to the narrative. Manipulating short-term movements through microstructure techniques is not the same as structurally controlling the global gold price.

The global gold market has a colossal scale. According to the World Gold Council, the total value of existing gold exceeds 12 trillion euros, and central banks hold more than 35,000 tons as reserves. No private entity can indefinitely sustain a massive distortion without being arbitraged by other actors. In deep and liquid markets, inefficiencies tend to correct themselves.

This does not mean the market is pure or perfect, but it does mean we must distinguish between temporary influence and systemic control. Power in financial markets exists, but it is not omnipotent, and confusing technical manipulation with absolute domination only distances us from rigorous analysis.

It is also true that influence is not always technical. Large banks publish forecast reports that can alter expectations and capital flows. This is part of the market game. The limit appears when conflicts of interest or opaque coordination between research and trading arise. But even here, we speak of influence, not permanent control — and the difference is crucial.

A lesson for the community

The gold market is not a stage of constant conspiratorial engineering. Nor is it a neutral space where all actors compete on equal footing. It is a complex ecosystem where global banks, central banks, refineries, funds, algorithms, and retail investors coexist.

The J.P. Morgan case leaves us with a clear lesson: concentration of financial power can generate distortions. But it also demonstrates that regulators, sanctions, and consequences exist. The manipulation was detected and penalized.

For the 11Onze community, the reflection is even more relevant. Investing in gold is not just buying a metal, but understanding where and how the price is formed. It is distinguishing between physical gold and derivatives. It is knowing that short-term movements may respond to complex financial dynamics, not necessarily to structural changes in real value. The best protection is not fear or viral narratives. It is knowledge.

In an environment where information circulates rapidly and extreme narratives gain audience, preserving wealth also requires preserving judgment. Gold has withstood centuries of monetary instability. But we must learn to withstand misinformation. Because understanding the system is the first step to moving freely within it.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Countries such as Ireland, Luxembourg, Malta, the Netherlands and Cyprus attract large numbers of multinational companies by offering tax advantages that allow them to reduce their tax liabilities significantly. These cross-border tax avoidance practices drain resources from other EU countries and create tensions between member states.

Tax avoidance and tax evasion are legal concepts that may seem synonymous but have a completely different legal nature. Tax avoidance is using legal practices to avoid paying certain taxes or to minimise a tax bill. Although this practice is not illegal, it often exploits loopholes in the law to obtain certain tax exemptions, deductions, and allowances. On the other hand, tax avoidance also seeks to avoid or reduce the payment of taxes, but in this case, using illegal practices, therefore, it is a criminal offence.

A good example of tax avoidance is what many Spanish multinationals do by having subsidiaries in low-tax countries to reduce the burden of their tax architecture. According to the latest ‘Country-by-Country’ report republished in April by the Tax Agency, the most productive workers of Spanish companies are to be found in their subsidiaries in Ireland, Luxembourg, Malta, and the Netherlands.

The productivity of these subsidiaries in EU tax shelters owned by the 123 largest multinationals in Spain ranged between 1.2 million and 1.9 million euros per employee, while in other European countries that do not offer the same tax advantages, this indicator was around 450,000 euros per employee.

This is no coincidence, nor does it mean that the employees of these subsidiaries are much more efficient than their counterparts in Spain. These delegations are not production centres, but small, low-staffed offices that manage a lot of money. And this is where the high productivity figures for these workers come from. With these practices, Spain loses more than 4.7 billion euros in taxes per year.

Advantages of tax havens

The case of Ferrovial, which, despite having received public aid, changed its headquarters from Spain to the Netherlands by merging with its subsidiary to pay less taxes, revived the debate on tax havens in the EU.

The Spanish multinational claimed that it had chosen the Netherlands as its headquarters because of the country’s triple A (AAA) credit rating and ‘stable’ legal framework, but it is no secret that a more favourable tax and regulatory climate was the main trigger for the move.

While it is true that corporate tax is around 25% in both countries, the first 395,000 euros of income is only taxed at 15% in the Netherlands. Moreover, the tax treatment of dividends is less aggressive and there is the possibility of redirecting part of their taxable income to the Netherlands Antilles with a more favourable tax treatment.

Similarly, Ireland has established itself as a Mecca for large technology, financial and pharmaceutical companies, attracting more than 1000 multinationals in these sectors, partly thanks to its benevolent corporate tax policy, but mainly because until 2015 it allowed the creation of two companies: one in a tax haven with intellectual property rights, and the other in Ireland that was used to sell to the rest of the world while paying for these rights to the first.

A similar case can be found in Luxembourg, Malta and Cyprus, where Spanish companies can pay less than 3% tax on their foreign business. These subsidiaries also stand out for having the lowest average number of employees. In Malta, the country with the second-lowest effective rate and where companies can be split in two, as in Ireland, there are 13 employees on average per subsidiary, while in Cyprus there are only 9.

Finally, there is the case of Belgium, where the General Court of the European Union found that tax exemptions granted to multinational companies constituted an illegal aid scheme, forcing the country to recover 700 million euros in unpaid taxes from at least 35 multinationals and to change its tax regime. An exceptional case in a European context favourable to tax havens that shows little sign of changing in the near future.

If you want to discover the best option to protect your savings, go to Preciosos 11Onze. We will help you buy at the best price the ultimate safe haven asset: physical gold.

Reuters reports that Swiss financial authorities and banks are considering new rules to prevent future bank runs such as the one that took place just before the bailout of Credit Suisse earlier this year.

It was the summer of 2022 when rumours began to circulate that Credit Suisse was facing imminent bankruptcy. The announcement by Saudi National Bank (SNB), its main shareholder, that it would not inject another round of capital, was the straw that broke the camel’s back, triggering a crisis of confidence on the part of shareholders, clients and investors who decided to withdraw some 111 billion euros in funds during the last quarter of the year.

In March 2023, the Swiss National Bank (SNB) approved emergency funding of up to 57 billion euros to bolster Credit Suisse’s liquidity amid the banking crisis. The Swiss Central Bank, together with the Financial Market Supervisory Authority (FINMA) and the Swiss government, wanted to buy time to negotiate the sale of Credit Suisse to domestic rival UBS.

A few days later, UBS absorbed its banking counterpart in a rescue operation designed to prevent its demise. Even so, the speed of the collapse of Switzerland’s second-largest bank, caused by a wave of customers taking back their money, surprised European analysts and banking regulators.

“The case of Credit Suisse has clearly shown that outflows of customer deposits can now be much faster and more extensive than assumed by the existing regulations,” said Swiss National Bank president Thomas Jordan at an event in Bern on 1 November.

A general overhaul of the country’s banking regulations

Since the failures of Silicon Valley Bank (SVB), Signature Bank and Credit Suisse, financial regulators around the world have been considering how to avoid a new uncontrollable bank run. In this context, it was only a matter of time before the Swiss authorities met with the relevant institutions to discuss how to implement new regulatory measures to reduce the risk of yet another massive withdrawal of deposits.

From the article published by Reuters, it appears that the talks between the Swiss authorities and the country’s major banks (including UBS) are part of a broader review of the country’s banking rules, and could primarily target the wealthy clients of Swiss banks. This is mainly due to their bank’s specialisation in wealth management, which means that they tend to have a higher concentration of deposits than some of their commercial banking competitors.

Negotiations are at an early stage, but according to sources consulted by the UK-based news agency, among the measures being discussed is the option of staggering a large part of deposit withdrawals over longer periods. The possibility of imposing fees on certain amounts of withdrawals is also under consideration. On the other hand, a higher interest rate is to be rewarded to customers who keep their savings for a longer period.

In any case, a representative for the Finance Ministry said that the issue of mass deposit withdrawals is part of an overall assessment of the regulatory framework for banks that are too big to fail in Switzerland and that the government plans to publish a report on the outcome of the talks in spring next year.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Banks have turned off the tap on lending because they fear a rise in non-performing loans. The difficulty in obtaining credit affects businesses and individuals, who have to cope with a rise in interest rates and a reduced supply of available credit.

Rising interest rates have pushed bank profits to record highs. The six main Spanish banks (Santander, BBVA, CaixaBank, Sabadell, Bankinter and Unicaja Banco) earned 19,761 million euros between January and September this year, 23.6% (3,747 million) more than in the previous period. In other words, in the first nine months of the year they have almost equalled the profits obtained during the whole of 2022, in which they made an all-time record of 20.8 billion in profits.

The profit figures are even more significant if we subtract the foreign activities of these banks, adding up to 9,000 million euros in profits, an increase of 55% over last year. This means that, if we add these profits to the data of the annual reports provided by Aebanca, the Spanish banking sector’s employers’ association, Spanish banks have accumulated net profits of more than 180 billion euros since the financial crisis of 2008 until 2023. And we should not forget that the cost borne by the state in injecting public money to rescue the financial sector exceeds 120 billion euros.

Despite these multi-billion euro profits, bankers continue to complain about the extraordinary tax on banks. According to Onur Genç, CEO of BBVA, “Spanish banks will not be able to compete in Spain”, while his counterpart at CaixaBank, Gonzalo Cortázar, stated last month that, “Taxing banks more is akin to shooting ourselves in the foot”, after he declared in May that, “It is not logical that we pay more than we earn”. On the government side, the Secretary of State for the Economy, Gonzalo García Andrés, does not understand the complaints about the tax on the sector after the latest profits declared: “I find it strange that we are still having this debate”.

Less remuneration for deposits and less access to credit

The Spanish banking sector has been one of the slowest in the European Union to reflect the European Central Bank’s interest rate hikes with a better return on savings. This has led to a flight of deposits by many families who have decided to diversify their savings by taking their money out of banks in favour of other products and investments that offer a higher return.

Moreover, according to the Bank of Spain’s Bank Lending Survey, Spanish banks have tightened the criteria and conditions applied to granting loans, due to the fear of default. Although the rate of non-performing loans rose slightly in August (3.56% compared to 3.5% in June and July), it closed the first half of 2023 at its lowest level in 15 years.

In this context, the Spanish government has called on financial institutions to “be extremely diligent” and speed up the granting of financial aid to families with variable-rate debt in difficulties, using the Code of Good Practices. Last week, the Bank of Spain reported that banks have yet to process 50% of the applications for adherence to the code for vulnerable mortgages.

The risk of cooling the economy and confidence in the banking sector

The restrictions in accessing credit mean that people with a higher risk, i.e. those who have more difficulties in paying their obligations, or who have no credit history, are unable to access financing. This difficulty in obtaining financing is experienced by both businesses and households. Even so, according to the Bank of Spain, during the last three months, the restrictions in the corporate financing segment have eased, while the conditions for household loans have tightened.

On the other hand, the higher cost of financing tends to cool the economy in general, as it dampens consumer spending and business investment. At the same time, as demand for goods and services falls, prices tend to moderate. In the business sector, the cost of capital needed to expand increases and the profitability of investments is reduced. In addition, some investors may reduce the money they have in the stock market and buy debt because of the higher returns.

While large companies have the option of ceasing to finance themselves through banks and can opt to go to the markets, SMEs and individuals are practically excluded from this alternative source of financing. If we add to this the precarious remuneration of savings, it is not surprising that the banking and financial services sectors are among those that generate the least confidence among consumers in Spain.

Fund lawsuits against banks. Do justice and get returns on your savings above inflation thanks to the compensation the banks will have to pay. All the information about Litigation Funding can be found at 11Onze Recommends.

‘Stock market psychosis’, “Wall Street goes mad”, “The market goes into depression”. How many times have we read in the press expressions comparing the economy to mental health disorders? Organisations such as Obertament believe that economic jargon stigmatises and needs to be remedied.

‘I have seen them in all colours. Even a professor of economics, in an opinion article, said ‘schizoid economics’, because, in his opinion, ‘the economy entered into a dissociation between two simultaneous and contradictory trends’’. He denounces it openly to Dani in Obertament‘s blog, where the organisation teaches about inclusive language with hundreds of first-person witnesses. The complaint is repeated over and over again.

It was precisely the habitual use of the words ‘psychosis’ and ‘schizophrenia’ as pejorative metaphors that set off all the alarm bells. Since then, Obertament has produced up to five reports with the help of Grup Barnils, with their corresponding campaigns and training sessions throughout the country to raise awareness of the stigma attached to mental health in the media and, specifically, in international, opinion, political and economic news. ‘The schizoid personality has nothing to do with economics – don’t mix apples and pears,’ says Dani.

Because, undoubtedly, the first offence is to use metaphors that consolidate the stigma without taking into account what it means to have a mental health disorder. According to the World Health Organisation (WHO), one in four people have it or will have it during their lifetime, and it can appear at any time, from childhood to old age. According to the latest Obertament report, for example, the WHO estimates that nearly 300 million people in the world have had depression, 4.4% of the global population.

And yet, these people often feel discriminated against in their family and work environment. In fact, according to a study published by the Autonomous University of Barcelona and Spora Sinergies, 80.1% of people with a mental health problem in Catalonia have suffered discrimination and stigma, and 54.9% have been discriminated against very often.

Disorders have nothing to do with violence

Therefore, when the media or economic and political professionals link mental health with conflicts, crises or difficult contexts, they further reinforce this discrimination. The second offence, in fact, is to link mental health disorders with violence. In this sense, the Audiovisual Council of Catalonia (CAC) warns in a guide that ‘the risk of aggression is exaggerated, fear and mistrust are encouraged and the gap of ignorance about mental health issues is widened’.

When we do so, we unwittingly reproduce a discourse that describes the economy as an aggressive environment, where competition without morals rules and suspicions pull the strings of the market. Is that really the image we have of how the economy works? The ACC also recalls that using terms such as ‘schizophrenic’, ‘bipolar’, ‘psychosis’, ‘depressive’ to describe chaotic, irrational, extravagant situations or to disqualify the opponent; using negative activation; or opting for alarming and morbid statements, ‘perpetuates false beliefs and stereotypes’.

Stereotypes that are almost insults

And, of course, the third offence is stereotyping, as Obertament denounces. We often use expressions that, because they are so normalised, we do not realise how derogatory they are. For example, current economic issues that are irreversible are frequently linked to mental health, which is wrongly associated with an incurable illness that prevents people from leading a normal life.

In this way, a mental disorder is regularly confused with a mental disability or dementia. The organisations also warn that, believing that we are being empathetic, we fall into ‘a paternalistic and compassionate tone’. This idea, moreover, is reinforced by illustrations that arouse rejection, sadness, or a dark and desperate inner abyss. Nothing could be further from the truth. In the end, as Obertament denounces, we end up turning mental health into ‘a catch-all’.

That is why, on the contrary, the organisations recommend using expressions such as ‘A person who has or has had…’, using adjectives and resources that do not refer to mental health, contextualising mental health disorders, listening to and respecting people with this diagnosis more, highlighting stories of overcoming mental health problems and avoiding sensationalism.

In the end, all this advice means that the focus is not on the person, but on the society that causes common disorders such as anxiety or depression. If we come to collectively change the economy and build a fairer, more honest and more ethical banking system, instead of reproducing prejudices, we might just turn it all around like a sock. Let’s start with the language.

11Onze is the community fintech of Catalonia. Open an account by downloading the app El Canut for Android or iOS and join the revolution!

According to data from the National Securities Market Commission (CNMV), banks have stakes in up to 174 companies in the energy sector. The percentage of shares held by these financial institutions ensures that they have decision-making powers on Boards of Directors and Shareholders’ Meetings.

Large banking institutions have stakes in many energy companies through shares or directorships in key management positions, which allows them to influence the management of these companies and the way in which the management of the energy transition takes shape.

CaixaBank is one of the most active banks in this sector, participating in companies such as Naturgy and TotalEnergies. In the case of Naturgy, CaixaBank was a majority shareholder of Repsol until 2019. The financial institution maintains its control over these companies through CriteriaCaixa and has directors in key positions in the energy companies.

For its part, Bankia also has members on the boards of Red Eléctrica de España, while Banco Santander has stakes in companies such as Endesa in Chile, Técnicas Reunidas and ENCE Energía & Celulosa. Banco Sabadell also has a significant presence in the energy sector, with board members in Repsol, ENCE Energía & Celulosa and Enagas.

The energy challenge

Conflict of interest

Bearing in mind that the energy crisis has sent the price of energy soaring and, therefore, the profits of these companies – big banks and the main energy companies have accumulated more than 64,000 in profits during the three years of pandemic and inflationary crisis – it is difficult to justify those who are allergic to public intervention in these economic sectors.

It is interesting that the same actors opposed to government intervention seem to have no problem in perpetuating and justifying the revolving doors. A profitable business, which, by signing former presidents and ministers onto the boards of banks and energy companies, has facilitated the electricity oligopoly in the Spanish energy market, preserving price manipulation at the expense of the consumer, and with extraordinary profits for these two sectors of the economy.

The solutions to the problems arising from the conflict of interests of the shareholders of these companies cannot be limited to one-off tax impositions on the financial and energy sectors after they have made extraordinary profits. If we want to eliminate the problem outright, perhaps we would do well to ask ourselves what is being paid for when a politician, with no relevant education or experience, is hired for a position in a bank or electricity company.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

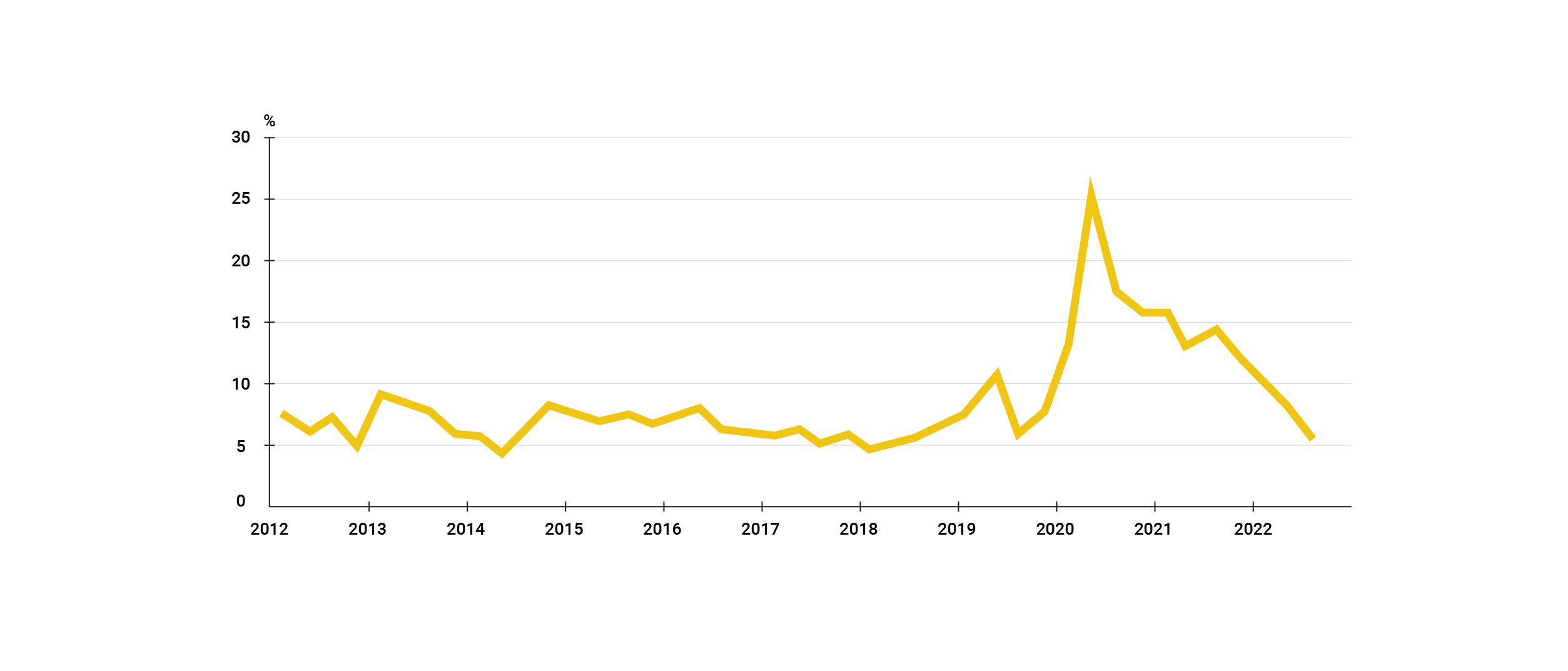

Households reduce savings accumulated during the pandemic to sustain spending in the face of sharp price rises. The fall in the savings rate is reflected in the decline in household financial wealth.

While rising prices have been strangling families for months, the rise in central bank interest rates to try to curb inflation is pushing up mortgage prices, adding up to a perfect storm, forcing households to use the savings accumulated during the sanitary crisis to maintain the same level of consumption at much higher prices.

Data collected by the Bank of Spain and the National Statistics Institute (INE) suggest that households saved some 269 billion euros during the peak phases of the pandemic. Even so, the gradual reopening of the economy and the rising cost of living has caused a large part of these accumulated savings to evaporate.

The INE report shows that in the third quarter of 2022, the household savings rate stood at 5.7% of disposable income, the lowest figure in four years. It should be borne in mind that this rate is calculated by eliminating seasonal and calendar effects, due to the fact that savings tend to fall in the first and third quarters and rise in the other two. If we disregard these seasonal adjustments, the data show a negative savings rate of -3.2% compared with 6.4% in the same quarter of the previous year.

SAVINGS RATE OF FAMILIES ON GROSS DISPOSABLE INCOME

Based on INE data

Less saving and less investment

Although the Bank of Spain has improved its GDP growth forecast by three-tenths of a percentage point to 1.6%, the forecast for private consumption falls by seven-tenths of a percentage point from 1.9% to 1.2%. On the one hand, the rise in the cost of living has ‘artificially’ increased consumption figures, but, on the other hand, the rise in interest rates and the reduction in the accumulated savings pool mean that the increase in household spending is expected to be weak. A slowdown in consumption could directly affect economic activity as it is a fundamental component of GDP.

Another consequence of the increase in spending and the reduction in savings capacity caused by inflation is reflected in a decrease in the household investment rate. The stock of household financial assets, whether in equity and investment fund (IF) holdings or a reduction in bank deposits, has been reduced by 53,431 million euros, or -2%, a fall not seen since the early 2020s.

In this context, the latest macroeconomic projections of the European Central Bank (ECB) indicate that although real household consumption is expected to recover gradually as the fall in real household income due to inflation and energy supply problems subside, the household saving rate will continue to fall this year to a level close to that recorded before the pandemic.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.