Will gold prices reach $3,000 an ounce in 2024?

Some market analysts predict that the price of gold could rise to $3,000 by the end of the year after hitting its third record high so far in 2024. Geopolitical tensions, strong central bank buying and growing demand from China are driving up the price of the golden metal.

Following gold’s strong March, thanks to the fact that futures investors and US gold ETFs helped push prices to new all-time highs, April is shaping up to be even stronger and all indications are that the price will remain elevated throughout the year.

Furthermore, the price of an ounce of gold has broken new records this week. The maximum of 2,384.35 dollars (2,196.18 euros) reached this Tuesday leaves behind the record set on Monday, according to market data consulted by Europa Press, although it has contained its advance and has been losing strength throughout the day to 2,358.30 dollars (2,172.19 euros) at the closing time in Europe.

Geopolitical tensions, armed conflicts and tighter monetary policy sent gold prices soaring in 2023, and we have started this year with an unprecedented gold rush. Investors are turning to gold for its historical value as a safe-haven asset and as a hedge against economic instability.

Likewise, the sanctions imposed on Russia have boosted the demand for gold by some central banks, following the trend seen in recent years. According to IMF data, central banks’ global gold reserves increased by 39 tonnes in January.

This represents more than double December’s net purchases and the eighth consecutive month of net purchases. This is the case of China’s central bank, which expanded its holdings in March for the 17th consecutive month. Moreover, central banks have purchased more than 1,000 net tonnes of gold for two consecutive years, according to the World Gold Council.

Will it reach $3,000 an ounce by the end of the year?

Gold’s meteoric rise could also be boosted by the US presidential election in November, which Donald Trump has a good chance of winning and which presents a very favourable backdrop for gold prices to reach $3,000 an ounce much sooner than expected.

On the other hand, the US Federal Reserve has indicated that there could be three interest rate cuts during 2024, which could push gold prices even higher. Investors were concerned that the Fed might make fewer than three rate cuts this year, as economic reports in recent months have shown that inflation remains high and the labour market strong.

There are growing signs that this is a special moment for the precious metal or, as the analysts at GSC Commodity Intelligence call it, “the beginning of a new historic super-cycle for gold”. Interestingly, real-time data obtained by GSC reveals a strong correlation between increased searches for “stock market bubble” and inflows of “gold capital”. This reinforces gold’s reputation as the best hedge for diversifying an investment portfolio.

Similarly, Aakash Doshi, head of commodities research at Citi, forecasts that the gold price could soar 50% to 3,000 per ounce in the next 12 to 18 months: “The most likely wildcard path to $3,000 per ounce gold is a rapid acceleration of an existing, but slow-moving trend: de-dollarisation in emerging market central banks, which in turn leads to a crisis of confidence in the US dollar”.

Preciosos 11Onze makes it easy to buy gold, at the best price and with total security. Protect yourself from economic crises with the ultimate safe-haven asset: gold. If you want your savings to keep or increase their value, Gold Patrimony.

Although reducing the weight of packaged products to mask a price increase is not new, persistent inflation has led many brands to use this practice to subtly make their products more expensive. In this episode of La Plaça, Gemma Vallet, director of 11Onze District, and Carolina Rafales, Product Manager, talk about the current economic situation and explain what downsizing is.

When applied to products sold in supermarkets, the term downsizing refers to offering less quantity of product for the same price, subtly reducing the amount of product to mislead consumers. This practice is also known as shrinkflation, a term credited to the British economist Pippa Malmgren.

As Gemma Vallet explains, In a situation where the CPI or inflation is getting out of hand, brands ‘use strategies to make you pay more for products’. Although, in this case, this is not an illegal marketing practice, consumer organisations warn that it is questionable and unethical because it is done with the intention of raising prices without the consumer realising it.

A drop in inflation that is not noticeable in food prices

Luis Planas, the Spanish Minister of Agriculture, Fisheries and Food, says he is “absolutely convinced” that food prices will go down, but asks consumers for “patience”, as the reduction in inflation will still take time to be reflected in the prices of supermarket products.

Given the rising cost of the shopping basket, the measures to limit the impact of inflation on consumers’ pockets have proved to be totally insufficient. The VAT reduction on foodstuffs seems to have served more to increase the commercial margins of distribution chains than to alleviate the precariousness of many families. “The situation is worrying, but despite the measures that have been taken, the market is the market, and it is difficult to foresee its impact in the short term”, stresses Carolina Rafales.

11Onze is the community fintech of Catalonia. Open an account by downloading the app El Canut for Android or iOS and join the revolution!

When we inherit, we are often concerned about the legal and tax consequences. Sometimes, once all the legacies have been distributed, the main heir is left with a remainder so low that it does not even reach the minimum that the law recognises. That is why, in Catalonia, the heir can claim the fourth falcidia or minimum inheritance quota. Agent 11Onze Jordi Coll summarises what this consists of.

Coll explains that the fourth falcidia, also known as the minimum inheritance quota, is regulated by article 427.40 of the Inheritance Code of Catalonia. It is a legal figure whose purpose is to guarantee the heir a minimum share of the inheritance, at least a quarter of the estate, when this is disproportionately encumbered by legacies or by rights in rem, such as mortgages or other assets.

Imagine, for example, that there are many beneficiaries in an estate and the main heir, with so many legacies to be distributed, realises that he or she will have almost nothing left. In this case, the heir is entitled to the fourth falcidia, i.e. he or she has the right to secure a quarter of the inheritance, even if this means reducing the inheritance of the other beneficiaries a little. The fourth falcidia is, therefore, a guarantee offered by Catalan law.

“If the heir sees that what has been left to him or her in inheritance does not cover 25% of the 75% of the inherited assets, he or she can claim the fourth falcidia. The other 25% is for the corresponding legitimacy rights of the persons to be inherited, whether or not they are the same heir or heirs,” the agent explains. Thus, the fourth falcidia acts as a limiter of the testator’s powers. This protects the principal heir and prevents him from having to renounce the inheritance for a small bequest.

Even so, it must be borne in mind that, if he or she accepts it, he or she will not only have to assume the responsibility for the payment of the bequests or legitimate, among other burdens, but, in the event that there is any debt of the testator, he or she will also have to take care of it. Therefore, before accepting an inheritance laden with legacies and obligations, it is necessary for a legal expert to carry out a study to assess whether it is really worth it. In this sense, the fourth estate provides some certainty that the heir will be able to pay all these expenses.

Do you want to know what requirements have to be met to be able to claim the fourth falcidia and how it is calculated? Just watch the video below!

The fourth falcidia

The Court of Justice of the European Union has overturned the rule that obliges you to declare your wealth abroad to the Treasury, because it considers it to be “disproportionate.” The Spanish government will now have to amend the law. But in the meantime, what exactly does Royal Decree 1065/2007 require? At 11Onze we summarise the regulations.

In fact, according to Royal Decree 1065/2007, at present, assets abroad that do not exceed 50,000 euros do not have to be declared. This is specified in article 42 bis, point 4, when it announces that “there is no obligation to report any account when the balances […] do not exceed, together, 50,000 euros.” Even so, in the event of exceeding this amount, all accounts must be reported to the Tax Agency through Form 720.

This model 720 was introduced in 2012 when the then finance minister of the Popular Party, Cristóbal Montoro, decided to pursue foreign assets in order to increase the Spanish state’s revenue during the worst years of the financial crisis. Montoro defended the measure as a “necessary tax regulation.”

It is precisely this Model 720 that the Court of Justice of the European Union (CJEU) considers “illegal,” because it imposes a system of penalties that is too high. The European Court’s ruling is devastating. It argues that Spain is pursuing the free movement of capital recognised by the European Union with a “disproportionate restriction.”

For this reason, the current PSOE finance minister, María Jesús Montero, who until now has ignored the legal process while awaiting the CJEU’s decision, has stated that Spain will reform the law. If it fails to do so, Spain could be fined by Brussels. The ruling, which is not explicit in these terms, also opens the door to claims from all those who have been forced to pay the penalties set out in the regulation.

But what exactly does Royal Decree 1065/2007 say? Here are the three most frequently asked questions. At the same time, especially now that the regulation has been appealed, we recommend resolving any doubts with the advice of a legal expert.

- What information is required to be submitted to the tax authorities? At present, the name of the financial or credit institution and its address must be provided. The complete identification of the accounts must also be submitted, with the date of opening and cancellation or the details of the granting and revocation of a credit authorisation. In addition, the account balances as at 31 December and the average balance for the last quarter of the year must be submitted, as required by Article 4 of Law 10/2010 on the prevention of money laundering and terrorist financing.

- When does Form 720 have to be filed? According to Article 42 bis, point 5, the form must be filed between 1 January and 31 March of the year following the year to which the information to be provided refers. This information must be submitted each year if, as stated in the regulations, “any of the joint balances […] has experienced an increase of more than 20,000 euros with respect to those determined in the submission of the last return.”

- Can I be penalised if I don’t do it? Yes, and in a “disproportionate” way, according to the CJEU. For this reason, you should ask your legal advisor for help, who will analyse whether you may incur a penalty, according to Law 58/2003, of 17 December.

In order to manage your assets properly and clarify any doubts, we always recommend that you seek specialist legal advice. In any case, whether you exceed 50,000 euros, you must continue to file your tax return in the country where you are resident for tax purposes.

11Onze is the fintech community of Catalonia. Open an account by downloading the super app El Canut on Android and Apple and join the revolution!

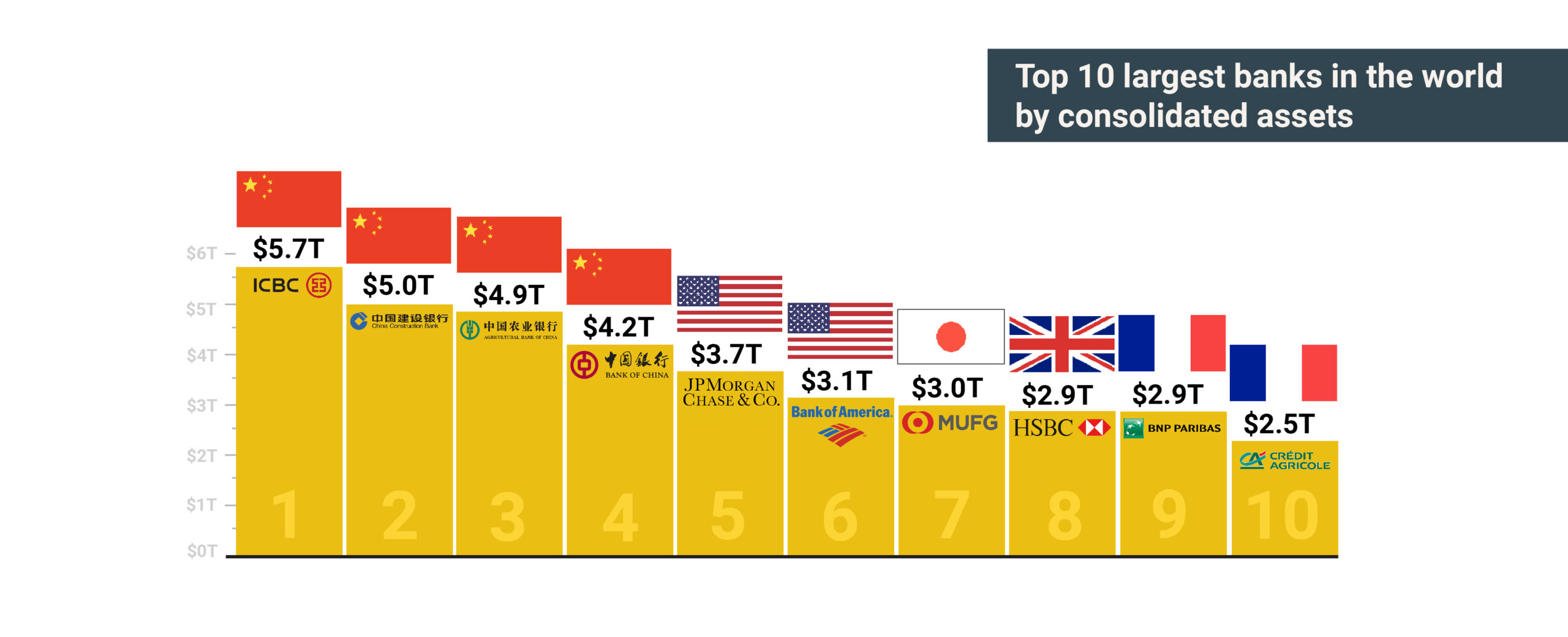

For yet another year, Chinese banks top the global ranking of the world’s most valuable banks, extending their dominance over their Western counterparts amid rising interest rates and slowing global economic growth.

The world’s major banks play a crucial role in the global economy, facilitating international trade, lending to businesses and providing financial services to millions of customers around the world.

This is particularly relevant in the current economic climate where many countries are trying to revive their economies while improving their fiscal balance sheets remains a challenge for their banking systems, given declining business volumes and lower demand for credit.

The combined value of the world’s 500 most valuable banking brands reached a record $1.44 trillion in 2023, almost double what it was a decade ago, according to a report by Brand Finance, the world’s leading brand valuation consultancy.

As every year, the main economic analysis and research entities compile data to publish the ranking of the best-positioned financial institutions according to their market share, turnover or consolidated assets.

Source: S&P Global Market Intelligence

The dominance of Chinese banks

Beyond brand value, the ranking of the world’s largest banks varies according to the parameters we take into account. Even so, the dominance of Chinese banks extends not only to the value of their assets, but they are also leaders in other parameters of banking activity such as deposits, loans, and the number of customers and employees.

Thus, the Industrial and Commercial Bank of China (ICBC), China Construction Bank, Agricultural Bank of China and Bank of China once again top the list compiled in a report by S&P Global Market Intelligence.

According to S&P, these four Chinese banks increased their assets by 4.1% in 2022, to a combined total of 19.8 trillion dollars. Moreover, Chinese banks already account for more than a third of the assets of the world’s largest banks.

Two US banks, JPMorgan Chase & Co and Bank of America, are next in the ranking, with the top six US banks accounting for $13.7 trillion in assets. They are followed by Japanese and European banks. In Spain, Banco Santander is in 17th position and BBVA in 46th.

If you want to discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy at the best price the safe-haven asset par excellence: physical gold.

Cash payments, less susceptible to being controlled by the government than digital payments, are being completely replaced by card payments, transfers or other electronic means. Should we be concerned? What options are there on the market? We talk about it with Iu Alemany, Head of Customer Service at 11Onze, in a new episode of La Plaça, Territori 17’s radio show.

Advances in technology, the rise of online shopping and the digitisation of finance have led to the popularity of electronic means of payment. Many countries have already started a transition process with the aim of phasing out cash payments to the point of their possible total disappearance in the not-too-distant future.

On the one hand, the new generations of digital natives are more used to paying via mobile phone or smartwatch than with cash. On the other hand, governments see a good opportunity to fight the black economy and tax fraud by restricting cash payments that are more difficult to trace.

Thus, more and more limits are being imposed on cash payments, such as the European Union limiting cash purchases to 10,000 euros, or the Spanish state going much further by banning cash transactions of more than 1,000 euros in cases where one of the parties is acting in a professional capacity.

An economy subordinated to the banking system

The elimination of cash payments facilitates the bankarization of the economy, i.e. the State’s control over the transactions carried out by individuals and companies through the information provided by the financial system. Cryptocurrencies and blockchain technology have positioned themselves as an alternative to this centralisation of finances, but states have also increased scrutiny and limited the use of such transactions.

In this context, several countries around the world have begun to explore the possibility of issuing central bank-issued digital currencies (CBDCs) – the European Central Bank has for some years now been working on the creation of the digital euro – which would give them unprecedented control over citizens’ money.

Increasing citizens’ dependence on the banking system will reduce the shadow economy, but it may also put our freedoms at risk and affect those most at risk of social exclusion. As Iu Alemany points out, “behind all this, there is a desire to have more control over the economy and the population and, if necessary, at any given moment to open or close the tap”.

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

Grifols shares have come to lose more than half their value since the vulture fund Gotham City Research published a report on 9 January questioning the Catalan pharmaceutical company’s accounting practices. Are we facing a case of market manipulation?

On 26 January, the multinational pharmaceutical company Grifols filed a lawsuit in the Southern District Court of New York, in the United States, against the entire Gotham City Research network for “publishing and distributing” a report “containing falsehoods about the accounting, communications, finances and integrity” of the pharmaceutical group.

In a statement to the Spanish Securities and Exchange Commission (CNMV), Grifols explained that its complaint alleges that Gotham City Research, in addition to publishing and distributing the report containing falsehoods about the company’s accounting practices, obtained “a substantial short position against Grifols”.

In the report published by Gotham on 9 January, the hedge fund accuses Grifols of falsifying its accounts and criticises the relationships that exist between management directors, family members and the various companies involved: “We are particularly concerned that these management executives and the parties involved are listed at different times as shareholders, directors, creditors, debtors or advisors of Grifols, all at the same time”.

Specifically, the US fund argues that the Catalan multinational “manipulates debt and EBITDA to artificially reduce debt by six times, when, in reality, it is between ten and thirteen times EBITDA”, which is why it argues that its shares are worthless. In addition, he also questions the debt of Scranton Enterprises – one of the companies through which the Grifols family controls the pharmaceutical company – pointing out that it has a leverage of 27 times its EBITDA.

What is Gotham City Research, and how does it operate?

Gotham City Research is a consulting and research firm founded by Dan Yu, a Wall Street analyst who also acts as a hedge fund. Ten years ago it became famous for causing the collapse of Gowex, a Spanish company specialising in the creation of free Wi-Fi networks.

These hedge funds, also known as vulture funds, have a business model, a priori lawful from a legal point of view, based on making profits from the stock market collapse of the companies they are targeting. In other words, they take bearish positions using short selling or derivatives to profit when shares or the market falls.

Their modus operandi involves choosing a company they consider to be overvalued and potentially vulnerable. They then borrow shares in this company – which they have to pay back within an agreed period – and sell them on the market. When these shares lose value on the stock market, they buy them back and then return them to the entity that lent them to them, keeping the difference.

Therefore, the more the share price has fallen, the more profit these funds make. The possible conflict of interest or market manipulation can occur because some of these funds, as in the case of Gotham City Research, are the ones who directly cause the collapse of the company in which they have taken a short position. They do so by publishing reports in which they question the financial state of these companies.

Grifols shares plunge and lose half their value

Since Gotham published its first report, it has not ceased its attacks on the pharmaceutical multinational, to the point that Grifols’ share price could not get back on its feet and has lost more than 50% of its market capitalisation, to the tune of more than 4.5 billion euros.

When it rains, it pours, so early last week, the credit rating agency Moody’s put Grifols’ debt rating under review, with the risk of a possible downgrade justified by the company’s lower cash generation and the delay in publishing its audited accounts.

This scenario did not change until last Friday, when its shares soared by up to 20% after the pharmaceutical company published its audited accounts, greenlighted “without exceptions” by KPMG, as reported by the company to the CNMV.

There is no denying that Grifols has debt problems, which have led it to make a series of changes at the core of its internal power that have resulted in a whole series of executives leaving the company over the last two years. The pharmaceutical company has senior managers dedicated to managing this debt. But beyond these well-known problems, it remains to be seen whether the information published by Gotham is true or false.

Investigation of possible criminal conduct

The CNMV is analysing whether Gotham complied with the requirements of the regulations on the dissemination of misleading information, at the same time as it is studying the information published by Grifols. Rodrigo Buenaventura, chairman of the supervisory body, said on Tuesday that they had requested further clarifications and additional information from the Catalan company, needing more time to conclude their investigation. “We just received them a few days ago and still need a few more weeks”.

If the allegations in Gotham’s report are ultimately confirmed, Grifols’ conduct could amount to a corporate crime of false accounting and misrepresentation to investors. On the other hand, if the information in the report is false, the hedge fund could be charged with market manipulation.

It would not be the first or the last time that a company has falsified its accounts, and it is certainly true that consultancy and analysis firms play an important role in complementing financial and market supervisory bodies. However, when these analyses come from hedge funds specialised in short-selling, there is a risk that the cure will be worse than the disease.

11Onze Recommends Bitvavo, cryptocurrency trading made easy, safe and at a good value.

Poor US economic data and expectations of interest rate cuts by the Federal Reserve and the European Central Bank push gold prices to a new all-time high of $2,140.6/oz.

The price of gold reached an all-time high as it looks ahead to the expected rate cuts by the Federal Reserve (Fed) and the European Central Bank (ECB) in June. On Tuesday the 5th, it reached a new record high of 2,140.6 dollars an ounce, surpassing the previous record set on 4 December, when the price rose to 2,135.40 dollars.

Given that according to the analysis made by Julius Baer, gold prices rise by 15.5% on average over the 12 months following a rate cut if it is followed by a recession, the expectation of a further cut increases investor demand. That said, if no recession exists, prices fall by 7% on average. In any case, it is a move that would affect US bond yields and the dollar and could lead investors to bet on gold as a safe-haven asset.

We should not forget that the European Union and the Eurozone avoided closing 2023 in recession by the narrowest of margins, mainly because the German economy, Europe’s largest, spiralled downwards thanks to the economic sanctions imposed on Russia. The Teutonic country’s industrial production contracted for the first time since the start of the pandemic.

In this context, some financial analysts warn that a possible rate cut by the ECB is unlikely to have a positive economic impact that will be felt before 2025. Jack Allen-Reynolds, an economist at Capital Economics, expects the eurozone economy to “flatline” in the first half of 2024 “as the effects of past monetary tightening continue to take hold and fiscal policy becomes tighter”.

Consumer confidence on the decline

Gold’s strong performance has also been spurred by recently released US economic data, which missed expected targets: the US manufacturing ISM fell to 47.8 in February from 49.5 expected and 49.1 in the previous month. The continued decline in the sector’s performance comes after 28 months of growth.

Meanwhile, according to a survey by the University of Michigan, consumer confidence in February also fell to 76.9 from an estimated 79.6. “Consumer confidence moved sideways this month, falling only two points below January and maintaining the gains in confidence seen over the past three months,” explained Joanne Hsu, the survey’s director.

This loss of consumer confidence reflects “lingering uncertainty about the US economy,” said Dana Peterson, Chief Economist at The Conference Board. This downward sentiment is mirrored among the G7 countries, which recorded significant declines – Britain (-3.2 points), Canada (-2.1 points) and Germany (-2.0 points) – in contrast to Asian countries, where consumer confidence is on the rise across the board.

To discover the best option to protect your savings, enter Preciosos 11Onze. We will help you buy the safe-haven asset par excellence, physical gold, at the best price.

El sector de les fintech ha crescut significativament en els últims anys. Això ha creat noves oportunitats per als consumidors i les empreses, que ara tenen accés a una gran varietat de productes i serveis financers innovadors. Xavi Viñolas, redactor d’11Onze, detalla algunes de les noves tecnologies relacionades amb les fintech.

Préstecs peer-to-peer

Els préstecs peer-to-peer (P2P), són una innovació financera que ha crescut en popularitat en els últims anys. El terme P2P lending fa referència als préstecs entre iguals. És a dir, a través de les plataformes de préstecs P2P com el crowdfunding els inversors poden prestar diners a altres persones o empreses sense la necessitat d’un intermediari financer tradicional, com un banc.

Productes bancaris Fintech

Criptomonedes

Les criptomonedes són monedes digitals que utilitzen la criptografia per assegurar les transaccions i controlar la creació de noves unitats. Es tracta d’uns actius digitals que segueixen guanyant protagonisme en el món financer, amb el Bitcoin com a exemple més conegut. Ofereixen avantatges com la seguretat, la privacitat i la descentralització, però també presenten riscos, com la volatilitat del seu valor.

Blockchain

La tecnologia blockchain, o de cadena de blocs, va ser popularitzada amb la creació del Bitcoin. És una tecnologia que permet fer transaccions entre dues o més persones sense la necessitat d’intermediaris. Ve a ser un llibre de comptabilitat digital on s’emmagatzemen totes les operacions distribuïdes en ordinadors interconnectats a través d’una xarxa P2P, sense necessitat d’un servidor central. Aquesta tecnologia s’ha mostrat clau per les fintech, ja que redueix costos, accelera els processos i millora la seguretat a l’hora de fer pagaments internacionals, verificar la identitat digital dels usuaris o facilitar el micromecenatge.

API

Les API, sigles en anglès d’Application Programming Interfaces, són un conjunt de protocols, mecanismes i eines que permeten la comunicació entre diferents aplicacions informàtiques. En el sector fintech, les API són una eina clau per connectar diferents plataformes i sistemes, permetent la transferència de dades de forma segura i eficient. Per exemple, una fintech que ofereix serveis de pagament podria utilitzar una API per connectar-se amb una plataforma de banca en línia perquè els seus clients puguin transferir diners directament des del seu compte bancari.

11Onze és la fintech comunitària de Catalunya. Obre un compte descarregant la super app El Canut per Android o iOS. Uneix-te a la revolució!

The expansion of the fintech sector and the increasing integration of financial services into mobile apps and e-commerce are revolutionising the way we interact with our money outside traditional banking. But what exactly is embedded finance and why is it becoming so important?

Embedded finance is a model whereby non-banking companies integrate banking services and products directly into their virtual channels through mobile applications or e-commerce platforms. The aim is to allow customers to access financial products and services without having to leave the platform or application they are using, carrying out transactions where the contracting or purchasing process is easy and fast.

This is possible thanks to the use of technologies such as APIs (Application Programming Interfaces), a set of definitions and protocols that enable communication between two software applications and facilitate interconnection between financial services platforms and other sectors through mobile phones in an immediate and intuitive way. This saves time and money when setting up a business, without the need to create an application and all its services from scratch.

A typical case of the use of this technology is online payment, which has become an indispensable tool for consumers. For example, a fintech offering payment services could use an API to connect to an online banking platform so that its customers can transfer money directly from their bank account.

Similarly, e-commerce companies offer payments integrated into their platforms, so that customers do not need to leave the website to make a transaction. This is not only convenient for customers but also offers merchants the possibility to customise their services and improve their efficiency.

The fintech revolution

This technology is especially useful for fintechs that do not have the resources to develop their own banking products or that want to offer more accessible and personalised financial services to their customers, providing an alternative to the traditional banking model. Previously, customers had to visit a bank branch or cash point to access financial services, but now they have access through the platforms and apps they already use, reducing the need for travel, paperwork and waiting.

In addition, embedded finance has also enabled the creation of new business models. For example, e-commerce platforms can offer financing to their customers for their purchases, eliminating the need to use a traditional financial institution. This can help companies improve customer loyalty and increase sales

Embedded finance can also help improve financial inclusion. Many people do not have a bank account or are unable to access financial services for various reasons, such as poverty or lack of access to the banking system. Through embedded finance, these people can access basic financial services from a simple mobile device.

In short, the symbiosis between banks, technology providers and distributors of financial products has created an ecosystem that is transforming the sector, broadening the range of services on offer, fostering competitiveness and improving the customer experience with greater accessibility, convenience, and flexibility.

11Onze is the community fintech of Catalonia. Open an account by downloading the app El Canut for Android or iOS and join the revolution!