Bitvavo is registered with the Dutch Central Bank and guarantees €100,000 per account and customer in case of unauthorised access.

Here's how to create an account at Bitvavo

Registered with the Central Bank of the Netherlands and headquartered in Amsterdam, Bitvavo, which 11Onze recommends, is the leading European cryptocurrency exchange platform in terms of crypto trading volume in euros. We have prepared a tutorial explaining the easy steps you need to follow to open an account.

Since its market launch in 2018, Bitvavo has been driven by one of its founding pillars in making cryptocurrencies accessible to everyone. It was entering a sector dominated by US-based exchanges that were pioneers in facilitating the exchange of digital assets, but which were unintuitive for people inexperienced in trading cryptocurrencies and had some shortcomings in terms of the security they offered to their users.

With a very tight fee structure that allows them to be among the most competitive exchange platforms in Europe, success was not long in coming. Bitvavo, which 11Onze recommends, accumulated more than 26 billion euros in trading volume by 2023 and has climbed to first place among European platforms in crypto trading volume in euros.

Steps you need to follow to open an account

Oriol Blanch, Bitvavo’s affiliate manager, has prepared a tutorial so that members of the 11Onze community who have not yet registered on the platform can start buying or selling cryptocurrencies and add or withdraw money in any format in a very simple way.

As Blanch points out, ‘to get started, it is important to open an account through the 11Onze Recommends link, so you get €20 just for registering’. This link takes you directly to the Bitvavo website, where you can claim the €20 bonus and start the registration process.

Tutorial: how to create an account at Bitvavo

Firstly, you will have to select your country and enter your first and last name, as well as your email address and password. You will then receive an email to confirm your email address.

With this done, you will be able to log in to Bitvavo. After answering a few questions, you will need to verify your identity and the bank account you want to link to the platform. From here you can start using the application. In the tutorial, Blanch also explains the basic operations you need to know and some of the more technical terms related to cryptocurrency trading.

11Onze Recommends Bitvavo, cryptocurrency trading made easy, safe and at a good value.

El Banc d’Espanya (BdE) ha comunicat que dona el seu suport al projecte de l’euro digital, poc després que el Banc Central Europeu (BCE) anunciés els seus plans d’avançar cap a una nova fase en el desenvolupament dels nous diners electrònics.

L’euro digital és el que es coneix com una CBDC (Central Bank Digital Currency), és a dir, una divisa electrònica gestionada i supervisada per un banc central, en aquest cas pel Banc Central Europeu (BCE). Podrà ser utilitzada tant per particulars com per empreses i, almenys en principi, no hauria de substituir sinó complementar els diners en efectiu.

Tot i que l’emissió d’un euro digital no és una certesa, després de dos anys d’un estudi preliminar sobre la possible introducció de la nova moneda digital, el dimecres passat la institució europea donava la llum verda als seus funcionaris per avançar cap a la següent fase del projecte. Amb la publicació d’un informe sobre el disseny i la distribució de la CBDC europea, el BCE anunciava que volia “començar a establir les bases per a la possible emissió d’un euro digital” a partir de l’1 de novembre.

Està previst que aquesta segona fase duri aproximadament dos anys, fins al 2025. Durant aquest període de preparació del projecte es finalitzarà el codi normatiu i la selecció de proveïdors per a desenvolupar la plataforma i la infraestructura. Segons el BCE, aquesta fase també servirà per “aplanar el camí per a una possible decisió futura sobre l’emissió d’un euro digital”.

El Banc d’Espanya es posiciona a favor de l’euro digital

Després que el Banc Central Europeu (BCE) anunciés la segona fase del projecte, el Banc d’Espanya (BdE) emetia un comunicat destacant el que considera com els avantatges de la CBDC i donant el seu suport al BCE. Juan Ayuso, director general d’Operacions, Mercats i Sistemes de Pagament del Banc d’Espanya, afirmava que l’euro digital conserva els avantatges de la moneda física.

El banc afirma que el format d’efectiu físic “no permet aprofitar tots els avantatges que ofereix la creixent digitalització de l’economia i la societat”. Un punt contenciós entre els proponents i crítics de les CBDC, que argumenten que els les monedes digitals centralitzades no poden garantir l’anonimat que ofereixen les transaccions en efectiu. Com admetia Christine Lagarde, presidenta del Banc Central Europeu, “L’anonimat total —com el que ofereix els diners en efectiu— no sembla una opció viable”.

Christine Lagarde, presidenta del Banc Central Europeu

Per altra banda, Josep Borrell, vicepresident de la Comissió Europea, afirmava que no hem de patir per la nostra privacitat i protecció de dades que “les dades personals estarien totalment protegides. Els bancs, ni tan sols el BCE, no veurien ni podrien rastrejar les dades o detalls personals de la gent. Els pagaments sense connexió oferirien un nivell de privacitat similar al que ofereix avui els diners en efectiu”.

Per a tranquil·litzar a la població i a les associacions de consumidors, la Comissió Europea i el Banc Central Europeu van presentar el juny passat un paquet de propostes legislatives per convèncer al Parlament Europeu i al Consell de la UE de donar suport al llançament de l’euro digital. Les autoritats europees justifiquen la necessitat d’una CBDC perquè cada vegada hi ha més ciutadans —un 55% segons les seves enquestes— que prefereixen pagar a través de mètodes electrònics.

Tanmateix, Javier Rupérez, president de la plataforma Denaria que dona suport a l’ús dels diners en efectiu, reaccionava a l’anunci del BCE assenyalant que, tot i que creu que l’euro digital podria ser un mitjà de pagament gratuït que “conviurà amb els diners físics, encara no existeixen garanties fermes que assegurin aquesta coexistència”.

Queda per veure si les CBDC podran garantir els conceptes de privacitat, anonimat i llibertat que ara tenim amb els diners físics i les criptodivises, però el debat està servit i sembla que l’euro digital està cada vegada més a prop.

11Onze Recomana Bitvavo, les criptomonedes de manera fàcil, segura i a baix preu.

Com és possible que contamini una cosa que no existeix físicament? El cert és que les criptomonedes requereixen gran quantitat d’energia per a les granges de minat. De fet, si el bitcoin fos un país, se situaria entre els 30 principals consumidors d’electricitat del món, com explica l’agent d’11Onze Aitor Canudas.

Tan sols uns dies després de la primera transacció de bitcoins, que es va realitzar al gener de 2009, el pioner de la criptografia Hal Finney mostrava a Twitter la seva preocupació sobre les emissions de CO₂ que generaria aquesta criptomoneda. I no anava errat.

Un estudi de la Universitat de Cambridge calcula que la xarxa bitcoin consumeix més de 121 TWh d’energia anualment, la qual cosa vol dir que, si fos un país, se situaria “entre els 30 principals consumidors mundials d’electricitat”, segons Canudas. De fet, per a que ens fem una idea de la magnitud de les dades, l’agent d’11Onze indica que aquesta criptomoneda gairebé consumeix tanta electricitat com Suècia i genera més emissions de CO₂ que Las Vegas.

La raó és que els processos necessaris per a les operacions de les criptomonedes requereixen una gran quantitat d’equips informàtics, les “granges de minat” i, per tant, una enorme quantitat d’energia. “Aquest conjunt de processos informàtics necessaris per validar les transaccions i generar nous blocs representa un 0,2 % del consum mundial d’electricitat”, especifica Aitor Canudas.

El problema és especialment greu en el cas del bitcoin, ja que, com advertia recentment Bill Gates, aquesta criptomoneda és la que consumeix més electricitat per transacció. D’aquí que, segons estimacions del Massachusetts Institute of Technology (MIT), l’ús dels bitcoins generi una petjada de carboni cada any d’entre 22 i 22,9 megatones.

Les criptomonedes no són innòcues per al medi ambient.

L’origen brut d’una energia neta

Si bé normalment veiem l’electricitat com una energia neta, això depèn bàsicament del seu origen. Sobretot a Àsia, i especialment a la Xina, gran part de l’electricitat generada prové de la combustió de carbó, que resulta molt contaminant. Per això, el fet que un altíssim percentatge de les granges de minat se situïn en aquesta regió per aconseguir els preus de l’electricitat més assequibles multiplica la petjada de carboni.

De cara a preservar el medi ambient, Aitor Canudas assenyala la necessitat d’augmentar el percentatge d’energies renovables en l’electricitat que s’utilitza “per crear els nous blocs i fer les transaccions del bitcoin”. Una altra alternativa que apunta l’agent d’11Onze seria recórrer a criptomonedes alternatives, com el cardano, “que en teoria contaminen menys que el bitcoin”.

11Onze és la comunitat fintech de Catalunya. Obre un compte descarregant la super app El Canut per Android o iOS. Uneix-te a la revolució!

The rise of e-commerce has created new consumer habits, but it has also highlighted the risk of shopping online with traditional payment methods. Virtual cards are born from the need to make online purchases more secure, and at 11Onze we already have our list, ready for Black Friday shopping.

The main feature is the format of the card, where there is no magnetic stripe or chip. The format and design of virtual cards varies between entities, but they usually only exist in virtual form and, therefore, the card data can only be accessed from the banking platform or digital wallet.

Protecting our account

Virtual cards, far from leaving your account uncovered, do just the opposite: they provide more protection than conventional cards.

The 11Onze virtual card, with a one-off price of two euros, allows us to set a daily payment limit. A card that does not have direct access to the account and can be activated and deactivated whenever the customer wishes; therefore, protection is assured.

Virtual shopping, physical card?

Digital shopping is becoming increasingly popular. Online shops, video platforms such as Netflix or Filmen, or other subscription services such as Spotify have become so popular that it is common to have a card for these services. For security and spending control, it is advisable to have a specific card for these subscriptions that does not have unlimited access to the account. For this reason, the virtual card can be very useful for Black Friday on 25 November and Cyber Monday on 28 November. These are dates when online shopping increases, and we therefore enter our card details at various merchants.

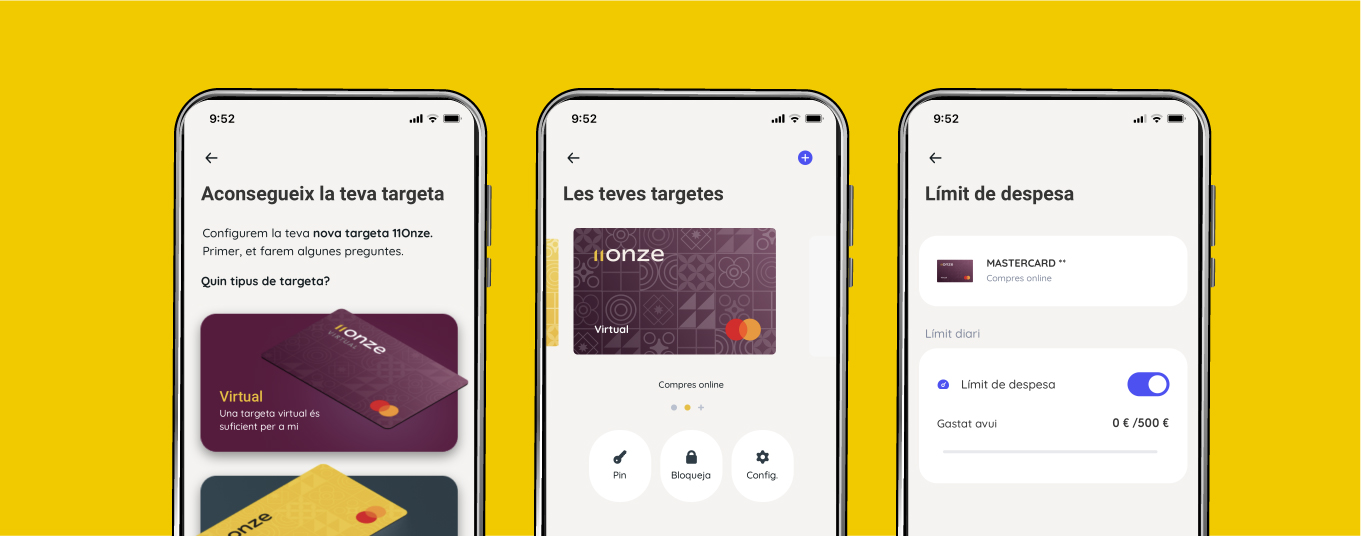

Request the 11Onze virtual card.

How to obtain the 11Onze virtual card

If you haven’t already done so, you have to download El Canut, 11Onze’s super app that comes to revolutionise traditional banking, a new generation wallet of wallets. Once registered, you can request a physical card, as well as a virtual card that will be automatically activated, and you will be able to use it to make online purchases.

The challenge for the coming years will be to bring this method of protection and agility provided by virtual cards to payments in other sectors, such as physical commerce or cash withdrawals.

Virtual Shopping? Virtual Card!

Les targetes virtuals són el principal mètode de pagament en línia. En un mercat on cada vegada es realitzen més transaccions virtuals, aquestes targetes ofereixen més protecció i agilitat en les compres.

Estan dissenyades específicament per a ser utilitzades com a mitjà de pagament virtual. L’objectiu és aportar seguretat al consumidor en les seves compres en línia, i protegir tant les transaccions com el compte corrent vinculat.

Disseny personalitzat per a compres digitals

La principal característica és el format de la targeta, on no trobem ni banda magnètica ni xip. El format i disseny de les targetes virtuals varia entre entitats, però és força comú trobar-nos que només existeixen de forma virtual i que, per tant, només s’accedeix a les dades de la targeta des de la plataforma bancària o la cartera digital.

La informació que tindrem d’aquesta targeta és la que ens demanaran en qualsevol transacció virtual: número de la targeta de setze xifres, codi de seguretat de tres xifres i data de caducitat. Aquesta és la informació més sensible de la targeta, i justament per això s’evita tenir-la en format físic, per a reduir les possibilitats de duplicar-la o suplantar la informació.

Protecció per als teus comptes

Les compres en línia han augmentat significativament, fins al punt que moltes empreses ja es creen sols en format digital. A Catalunya, la facturació dels comerços electrònics ja ha superat l’1,5 % del PIB. Però, tot i això, encara són molts els consumidors que es resisteixen a fer aquest canvi, la majoria motivats per la por que terceres persones tinguin accés als seus diners. I si bé és cert que aquesta és una problemàtica real, les entitats bancàries creen productes cada vegada més sofisticats per a evitar aquesta desprotecció.

Les targetes virtuals, lluny de pensar que deixaran el nostre compte al descobert, fan justament el contrari: aporten més protecció que les targetes convencionals. Podem trobar-nos amb targetes virtuals de prepagament, és a dir, que l’usuari les carrega amb l’import que necessita. Aquestes targetes no tenen accés directe al compte; per tant, la protecció està assegurada.

Altres targetes virtuals es poden activar i desactivar; per tant, només estarà operativa quan el client ho desitgi. Gràcies a peculiaritats com aquestes, disminueix encara més el risc d’operacions fraudulentes. Tot de mesures constantment en evolució que lluiten per acabar amb la ciberdelinqüència.

Més control per a tu, menys plàstic per al planeta

En termes pràctics, tot aquest sistema de protecció, que inclou la protecció de les dades de la targeta i la vinculació mínima amb el compte corrent, dificulten l’accés dels hackers als comptes personals. En cas de patir operacions fraudulentes, de fer reclamacions o de realitzar compres en altres països, les targetes virtuals faciliten significativament la resolució d’aquestes operacions i, el més important, permeten que qualsevol incidència que pugui sorgir afecti tan sols a aquesta targeta, sense implicar la resta de targetes o de comptes.

A més, no tenir format físic suposa una forma de pagament més sostenible que, en molts casos, implica menys costos de manteniment per al client.

Les targetes físiques, en procés de digitalització

Cada vegada és més comú tenir les targetes físiques, de dèbit o de crèdit, també en format virtual per pagar a través del mòbil. Solen estar lligades a les targetes físiques i al nostre compte corrent. A més de permetre fer pagaments sense necessitat de portar la targeta física, faciliten l’opció de bloquejar la targeta en cas d’incidència i ens permeten controlar les despeses en tot moment.

El repte dels pròxims anys serà apropar aquest mètode de protecció i agilitat que aporten les targetes virtuals en els pagaments de la resta d’àrees com ara el comerç físic o la retirada d’efectiu.

11Onze s’està convertint en un fenomen com a primera comunitat fintech de Catalunya. Ara, llança la primera versió d’El Canut, la super app d’11Onze, per a Android i Apple. Des d’El Canut es pot obrir el primer compte universal al territori català.

Credit cards were created in the 1950s, and with the arrival of smartphones, virtual cards became popular. Let’s review the history of cards and their possibilities.

Sixty years ago the first payment card was introduced and, since that day, the way we shop has changed to adapt to the era of e-commerce, bringing about a radical change in the way we pay. The way we consume is constantly changing, specially with the increase in e-commerce, following the start of the Covid-19 pandemic in 2020, as can be seen in the study carried out by Kantar, which states that 3 out of every 4 Spanish households have made purchases online in 2020, and that these households will continue to shop online in 2021. Households that now shop online account for 74.4%, which has increased e-commerce consumers by 8.4% since 2017. As detailed by Kantar in its study, the remaining 26.6% of consumers are older people who commute to buy products themselves, as they prefer a personalised service. And just as the consumption model has changed, so has the payment model. Welcome to the era of virtual cards.

Which card is best for me?

What are virtual cards?

Virtual cards are more secure cards, and unlike conventional payment cards, they are completely virtual. They are exclusively used for virtual purchases, but with the possibility to be used in physical establishments if you have the card linked to a wallet on your smartphone. The virtual card has a number, an expiry date, and a control number, as Rankia details. The financial website also states that the security controls of virtual cards are very varied. Some banks have a dynamic code that changes with each purchase, while others allow very few purchases to be made, and if there is money left on the card, this money is automatically returned to the account from which the card was recharged. Each customer is free to make a new virtual card whenever they need it, it’s as simple as that.

How was the virtual card born?

Since the world’s first payment card from Diners Club in 1950, the world of payment cards has come a long way, from the arrival of credit cards in Spain in the 1960s to virtual cards, according to Finanzas. A website specialising in finance reminds us that virtual cards were born with the arrival of mobile telephony, with the payment systems known as “wallets”.

How are they regulated?

The European regulation PSD2, the new European regulation on electronic payment services, came into force in September 2018, with the aim of reinforcing security for consumers with e-commerce payment systems. With this regulation, which has been in force for three years now, it can be said that something is changing in the way we make payments. In short, we can say that virtual cards are here to stay as another means of payment.

11Onze is the community fintech of Catalonia. Open an account by downloading the app El Canut for Android or iOS and join the revolution!

In a context where the use of cash is in decline and digital payments and cryptocurrencies are the order of the day, more than 130 countries are considering the introduction of central bank-issued digital currencies (CBDCs). What are the pros and cons of these new digital currencies?

The digitisation of the economy has brought the convenience of being able to make digital payments and has spurred the popularity of cryptocurrencies. This revolution in the financial system has led many central banks, initially reluctant to introduce them, to consider issuing their own digital currencies (CBDCs).

In this context, Europe does not want to be left behind and will create its own digital currency, as countries such as China, Sweden, and Uruguay have already done. Known as the digital euro, it is an electronic currency that will be managed and supervised by the European Central Bank (ECB), which can be used by both citizens and companies and which will not replace cash, but will complement it.

As for the Spanish state, the Banco de España (BdE) has positioned itself in favour of the introduction of the digital euro, issuing a statement highlighting what it considers to be the advantages of this CBDC and giving its support to the ECB. Juan Ayuso, Director General of Operations, Markets, and Payment Systems at the Banco de España, stated that the digital euro retains the advantages of the physical currency and pointed out that the physical cash format ‘does not allow all the advantages offered by the growing digitalisation of the economy and society to be exploited’.

Fintech Talks – The great economic reset

A complementary payment method

Financial inclusion. A centralised digital currency can contribute to financial inclusion, especially in areas where access to traditional banking services is limited. It would also be an alternative to cash in extreme situations, such as disasters, where cash cannot be used and where traditional means of payment, such as POS, do not work.

Security and financial resilience. One of the main promises of CBDCs is to improve the security and resilience of the financial system. Unlike decentralised cryptocurrencies, CBDCs are backed by central banks, which guarantees their value and makes them less susceptible to fluctuations in cryptocurrency markets. Therefore, the digital euro would just be another way of paying in euro, convertible at parity with physical money.

Reduced transaction costs. CBDCs eliminate the need for intermediaries such as payment processing institutions. Moreover, their digital implementation simplifies the transfer of cash, which benefits both individual users and businesses, especially in international transactions, where traditional costs are high. As for the digital euro, it is designed to be costless for individuals using it to make ordinary payments and can be used anywhere in the euro area.

Traceability and transparency. CBDCs allow detailed tracking of financial transactions, which can help governments combat money laundering, terrorist financing and tax evasion. However, the European banking regulator says that the digital euro would allow payments to be made without sharing data with third parties unless this is necessary to prevent illicit activities.

What are the potential risks?

Privacy and government control. One of the most important concerns about CBDCs is the potential loss of privacy for users. Unlike cash and cryptocurrencies, which allow anonymous transactions, CBDCs can have full traceability over most transactions. This would allow governments to know exactly how we spend our money and give them the ability to stop payments or confiscate them, as happened with the truckers’ protests against the Canadian government.

Cash and financial freedom. The increasing digitisation of money, driven by CBDCs, could mean the end of the use of cash, an important method of payment in many societies. This would not only affect the freedom to choose the means of payment but would also have implications for people with limited access to these technologies. In this respect, the ECB states that the digital euro would be a complement to cash, not a substitute, so banknotes and coins will remain in circulation.

Negative impact on commercial banks. The use of CBDC could negatively affect the financial intermediation now provided by commercial banks, as citizens may prefer to keep their money directly in digital accounts managed by the central bank, especially in times of crisis. This would reduce the role of commercial banks, affecting their ability to offer loans, credit, and financing.

11Onze Recommends Bitvavo, cryptocurrency trading made easy, safe and at a reasonable cost.

Technology companies are investing large amounts of money in creating new multimodal artificial intelligence models and algorithms that can learn, reason and make decisions autonomously after collecting and analysing data.

Data processing and machine learning are accelerating the development of artificial intelligence at an unrelenting pace. While early AI assistants, such as Siri or Alexa, were limited to simple interactions, with the entry of ChatGPT on the scene everyone started talking about the next generation of AI assistants that could perform more complex tasks.

The goal was to create a system capable of performing a wide range of tasks, like a human assistant. However, these assistants did not go beyond the processing of textual data, limiting their practical use. It is an approach far from how humans understand the world, using multiple sensory channels simultaneously.

Thus, the evolution of AI is focused on new algorithms that can process and integrate information from various modalities, including images, audio and video, to improve interaction. Many experts, including Sam Altman, CEO of Open AI, say that multimodal AI agents are the next big revolution that will make AI tools even more integrated into our daily lives than smartphones.

The future of multimodal agents

In practical terms, a multimodal AI agent can, for example, analyse a text while processing an image, spoken language, or an audio clip to give a more complete and accurate response, both through voice and text. This opens up new possibilities in various fields: from education and healthcare to e-commerce and customer service.

According to David Barber, director of the Centre for Artificial Intelligence at University College London, these agents could also streamline the processes of businesses and public bodies, so that an AI agent could function as a more complex customer service canister.

Unlike the current generation of linguistic model-based assistants that can only generate the next likely word in a sentence, an AI agent would have the ability to act autonomously on natural language commands and process customer service tasks without supervision, such as analysing customer complaint emails and, by accessing the management database, process them according to company policies.

Multimodal AI agents can also analyse consumers’ shopping behaviour, including their interaction with various media, to provide more personalised product recommendations. This is a practical application that would also be useful in educational environments, transforming the learning experience by providing personalised and interactive content.

Perhaps one of the most obvious uses of this latest evolution of AI is autonomous vehicles that can drive with limited human intervention. While it is true that we are still a long way from these vehicles being able to achieve fully autonomous operation, AI agents are already an integral part of their operation, sensing the car’s environment and making informed decisions.

In the medical field, it can not only improve patient care by integrating various types of data but can also help healthcare professionals diagnose diseases, identify patterns and suggest possible treatments by analysing medical images, vital data and the patient’s medical history. However, as with other potential applications that handle large amounts of personal data, privacy, security and ethical issues will need to be addressed to ensure public acceptance.

11Onze is the community fintech of Catalonia. Open an account by downloading the app El Canut for Android or iOS and join the revolution!

Bitvavo, the Amsterdam-based cryptocurrency exchange platform with 1.5 million users in Europe that 11Onze recommends, dethrones Binance as the leading European exchange in euro crypto trading volume.

Registered with the Central Bank of the Netherlands and headquartered in Amsterdam, Bitvavo is one of the leading exchanges in Europe and already has 1.5 million users on the continent. It launched in 2018 offering reasonable fees, security, and a simple and easy-to-use platform that has made it an ideal choice for beginners and experienced users alike.

Although some international cryptocurrency exchanges based in the US offer trading in euros without being officially based in the EU, there are several cryptocurrency exchanges based in Europe, such as Bitvavo, that specialise in trading services for European customers.

Since its founding, Bitvavo has climbed to the top spot among European platforms, overtaking Binance and amassing more than €26 billion in trading volume by 2023. In the cryptocurrency markets, the euro continues to gain ground on the dollar, doubling its market share to 17.2%.

Security as a badge

Bitvavo is registered with the Dutch Central Bank and guarantees €100,000 per account and customer in case of unauthorised access.

Bitvavo’s differentiating factors

Bitvavo is regulated by the Dutch Central Bank, which ensures compliance with European regulations, and its users have access to the Deposit Guarantee Fund, so that up to €100,000 could be recovered in the event of the exchange’s bankruptcy.

In addition, Bitvavo offers a ‘Recurring Buy’ option, which allows you to automatically buy and invest in cryptocurrencies without the need to constantly monitor the market. This way, you can minimise the impact of market fluctuations and gradually build up a stable cryptocurrency portfolio.

Oriol Blanch, Affiliate Marketer at Bitvavo, details the three key points that in his opinion make Bitvavo one of the preferred platforms among European users:

- Main cryptocurrency exchange in euros.

This allows you to buy directly in euros without going through any other currency. It is therefore ideal for EU residents. - Lowest and most transparent commissions on the market.

With Bitvavo you can buy at the best price. This is thanks to low trading fees. In addition, before you fulfil each transaction, you can see when you are paying commissions.

High liquidity within Bitvavo markets that offer a very low ‘Spread’ (price differential between buyer and seller). - Security. – Bitvavo offers security measures that make it the most secure exchange. Account guarantees, cold wallet safekeeping and anti-phishing measures.

Signing up to the platform is quite easy, you can do it via the 11Onze Recommends link.

Artificial intelligence (AI) is an increasingly ubiquitous technology in our daily lives and is already supplanting some human functions. Should we be concerned? Will it surpass human intelligence? We spoke to Dr Ricardo Baeza Yates, Director of Research at Northeastern University in Silicon Valley.

The coexistence between people and artificial intelligence has become normalised. The exponential increase in the processing power of computers, Big Data and advances in machine learning algorithms and neural networks have enabled artificial intelligence to advance by leaps and bounds.

Although AI is moving forward at a dizzying pace, it cannot yet replicate human emotions, creativity or intuition. It relies on specific learning and does not have the ability to understand the world as a human does. However, it is only a matter of time before it surpasses humans’ intelligence and abstract thinking capability.

The software engineers who developed ChatGPT warn that in ten years artificial intelligence systems will be able to surpass humans in most disciplines. Even so, Ricardo Baeza believes that it is possible that in the future “we will have a type of augmented humanity, rather than robots that dominate or exterminate us”, and adds, “we are always the ones in control and, if we are not in control, it is because of us, not because of artificial intelligence”.

The transformation of the labour market

One of the main concerns raised by the development of AI is the impact on the labour market. The automation of tasks threatens specific jobs, especially those that are routine or repetitive. But this has happened before, and it is important to remember that history has shown that technology also creates new job opportunities. “Artificial intelligence should complement people. Making the right use of it to increase their productivity,” says Baeza.

On the other hand, the massive use of personal data and machine learning raises questions about privacy, algorithmic discrimination and accountability in decisions made by AI-governed systems. It is crucial to establish sound ethical frameworks and the adoption of practices that ensure AI is used for the benefit of society at large.

11Onze Recommends Bitvavo, cryptocurrency trading made easy, safe and at a reasonable cost.