Are our assets and liberties at risk?

The draft bill for the reform of the Spanish national security law foresees that, in the event of a serious crisis, citizens of legal age may be obliged to provide “personal services” to the state, which may also intervene, or provisionally requisition goods and capital that it deems necessary.

This is what is established in the draft bill published by the newspaper El País, which modifies the Law 36/2015 on National Security. These measures were already, in part, contemplated by the Law 17/2015 on the National Civil Protection System for cases of emergency, but are now extended to the field of national security.

Seizing assets and capital

One of the most controversial points that has generated the most criticism from the opposition, consternation on social media, and debate among legal experts, is the possibility, in extreme conditions, of the state having the power to seize or requisition our assets and capital. Nonetheless, with the right to be compensated for economic damages in the business activity, but without compensation for any obligation to make a personal service.

It should be noted that this is a draft that has not yet been approved and has to go through the Cortes. However, the ambiguity and lack of specificity give rise to different legal interpretations that create mistrust.

As Arcadi Sala-Planell, head of the Legal Department at 11Onze, explains, the draft bill is not very precise. “It is designed in such a way that the government can act with total freedom and discretion, thanks to the imprecision of the articles, which allows for a legal interpretation that is too broad”.

Former Constitutional Court lawyer Joaquín Urías believes that “the law must include mechanisms to prevent anyone from using it in the future for disproportionate or illegitimate purposes” and insists that the reform “must be as detailed as possible” and should include “a list of catastrophes or emergencies for which it could be applied, which authorities are qualified to guarantee compliance and even the development of a system of sanctions”.

Securing critical resources

It is clear that lessons learned during the Covid-19 pandemic and the subsequent declaration of a state of alarm have influenced the wording of this draft bill. Speculation as a result of excess demand and shortages of certain medical supplies such as masks or PPE led to extravagant price rises and dramatic scenes of medical staff working without adequate protective equipment.

In a context of extreme crisis, governments want to ensure that they have sufficient legal tools to guarantee critical resources. A concept that is not new and for which other countries, such as the US, already have similar laws that they have used during the pandemic to urge companies to collaborate with state authorities in overcoming the crisis.

That said, we are talking about an ordinary law, but one which, as jurists have pointed out, may affect our fundamental rights, and which will possibly be processed as an organic law in order to avoid legal issues and have all the legal guarantees. This procedure will have to be accompanied by more precise and detailed articles to guarantee that there can be no abuse of authority by the representatives of the executive branch of the State.

Do you want to be the first to receive the latest news about 11Onze? Click here to subscribe to our Telegram channel

Right now, having money in your current account has become a problem: a problem for banks and a problem for bank users. The level of bank fees imposed on money kept in current accounts is disproportionate. They are charging us for having the money deposited and the only way to avoid paying this commission is to invest in one of their financial products: an investment fund, a retirement product… This is happening at most banks across Europe. Will we go back to hiding the money under a tile or the mattress?

Why do banks charge for deposits?

The answer is because negative interest rates are hurting the banks’ income statement. Therefore, having customers deposit their money in the bank generates a cost and no benefit.

Suppose we deposit €10,000 into our current account at the bank. The bank has to keep this money and have it available for you at all times. If there are 100 people who all deposit €10,000, the bank will have €1,000,000 in its hands. With this amount of money, the bank can do two things: either lend it, or keep it in cash. Lending it carries a risk, and keeping it in cash entails a number of costs, either due to the need for high-security storage, or the option of making a deposit with the European Central Bank.

Agent David López analyses the pros and cons of saving and investing

Why do ECB deposits have a cost?

The deposit at the European Central Bank has a cost of -0.50% for banks. This means that, in order to deposit the million euros of the example, the financial institution would have to pay approximately €5,000 in cost.

The aim of the European Central Bank for maintaining negative interest rates is to push financial institutions to increase lending to businesses and consumers, and thus reactivate the consumer economy. The European Central Bank has also chosen to penalise savings with the aim of moving, investing, and spending money. The idea is to boost the economy and alleviate the continent’s meagre macroeconomic outlook.

However, due to the incidence of COVID-19, household savings have increased and, therefore, there has been an increase in liquidity, and the value of deposits has been increasing. Thus, due to negative interest rates, banks have had to pay large sums of money to deposit all this liquidity in the European Central Bank.

As banks get negative returns on liquidity, they no longer want to raise more money, and have stopped offering fixed-term deposits and remuneration in their accounts. Far from our reach is the financial memory of 2008, when the EURIBOR was above 5% and there were deposits that gave you 10% or 11% APR a month. Or others, which gave 7.5% APR in three months; or 5-6% deposits in the medium and long term. If one day we have such deposits again, it will be because the EURIBOR will have risen again.

Are the tile or the mattress back?

However, the solution is not to keep money inside the mattress or under the tile, as the loss of the value of money, due to inflation, also reduces our purchasing power. Right now, the solution to all this mess is a pretty complicated equation about what I want to do with the money saved, how long I want to keep it off, and so on. These and other questions can guide us on what we can do about it. But that’s a horse of a different colour.

11Onze is the fintech community of Catalonia. Open an account by downloading the super app El Canut on Android and Apple and join the revolution!

From 10 April 2021, grants from the MOVES III Plan (or Moves Plan 2021) are available, which will run until 2023. This plan to help purchase electrified vehicles has an initial budget of €400 million, expandable up to €800 million, if the demand justifies it.

The budget for grants will be divided by autonomous communities, depending on their population. With this in mind, Andalusia would be the most benefited with €71.35 million, followed by Catalonia, with €65.79 million, the Community of Madrid, with €57.15 million, and the Valencian Community, with €42.63 million. Of course; it is not possible to submit applications until the Autonomous Communities have activated their plans.

There are two types of grants:

- For the purchase of plug-in electric and hybrid vehicles.

- For the installation and development of recharging points throughout the territory — depending on the population, up to 80% of the total cost of the installation can be obtained.

In addition to cars, support is also provided for the purchase of vans, motorcycles, and quadricycles. Unlike the previous plan, MOVES II, trucks, buses, gas cars, and electric bicycles are excluded from this current plan.

Grants for individuals

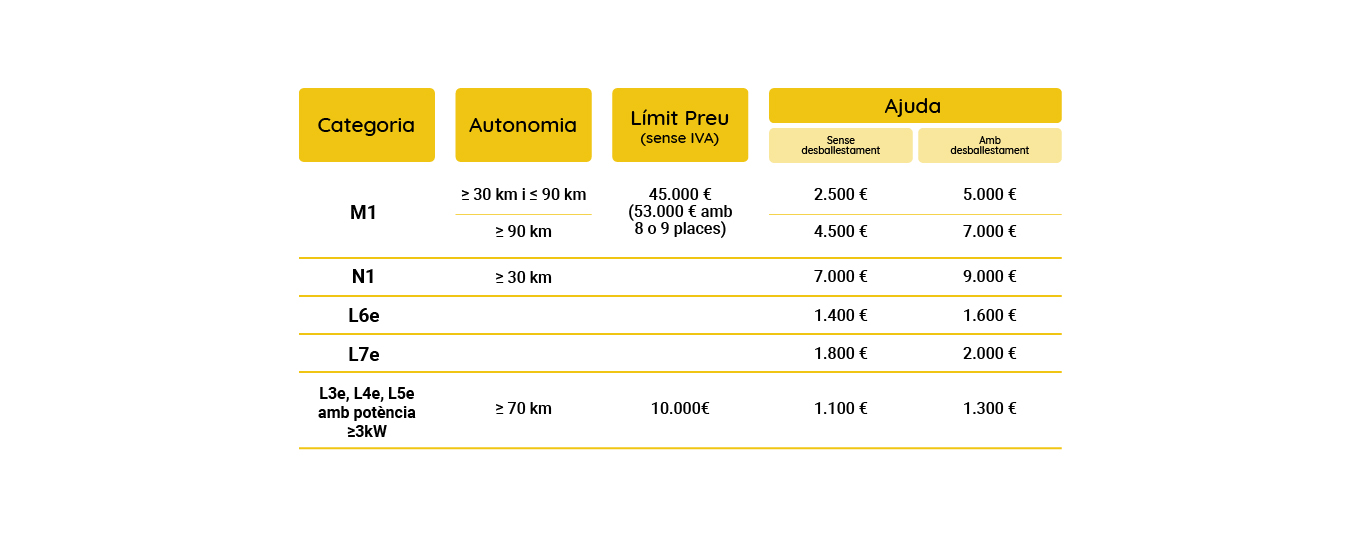

For cars, grants can reach up to €7,000, as long as a car older than seven years is delivered for scrapping in return.

The types of vehicles that can benefit from the Plan are:

- 100% electric cars (EV or BEV) with an electric autonomy greater than 90 kilometres. For these, the maximum amount can reach €7,000. The requirements are:

- Delivering a car over seven years old to be scrapped. Otherwise, the amount is reduced to €4,500.

- The amount (excluding VAT) of the purchase of the new electric car cannot exceed €45,000, or €53,000 if it has 8 or 9 seats.

- These same conditions apply to plug-in hybrids (PHEV) with more than 90 kilometres of approved autonomy (very few achieve this).

- Plug-in hybrid cars (PHEV) with an electric autonomy of between 30 and 90 kilometres.

- Cars with fuel cell technology (FCV or FCHV). The requirements are:

- The maximum subsidy is €5,000, in exchange for a car older than seven years to be scrapped. Otherwise, the subsidy will be half, €2,500.

- The purchase price cannot exceed €45,000 (excluding VAT).

Synthesis of the Plan for individuals, self-employed workers, and public administrations

Cars and SUVs are in the M1 category. N1 includes goods vehicles weighing less than 3.5 tons. L6e and L7e include quadricycles, and L3e, L4e, and L5e are motorcycles and tricycles.

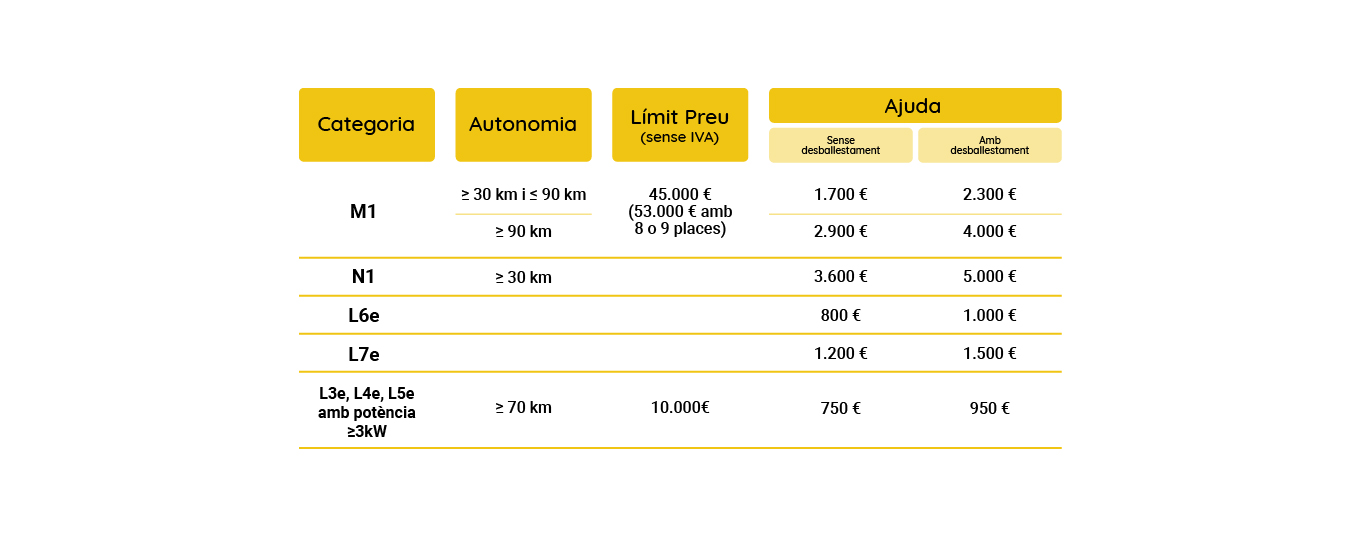

Synthesis of the Plan for SMEs

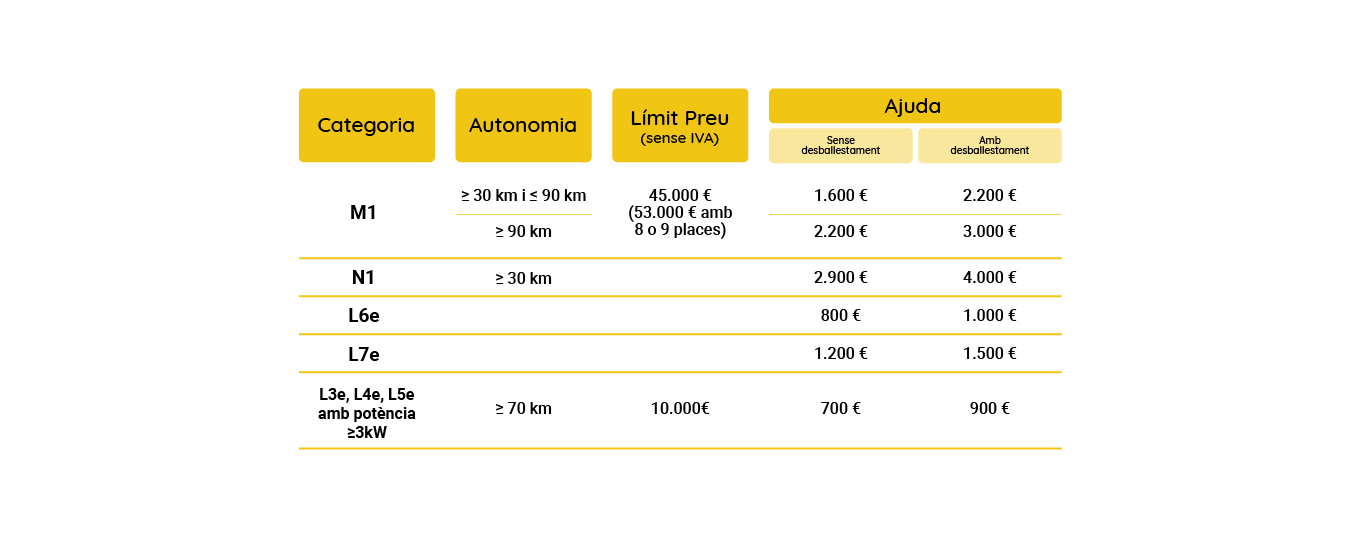

Synthesis of the Plan for large companies

In order to prevent cities from concentrating most grants, the Spanish government is offering greater subsidies to municipalities with less than 5,000 inhabitants and their citizens. In these cases, it is 10% more of what is indicated in the tables above. However, the registration in this same municipality must be maintained for some years.

An increase of 10% is also granted to VTC services, taxis, and owners with disabilities.

The Spanish government expects that, with these grants, by 2023 there will be at least 250,000 electric vehicles in circulation. Also, a minimum of 100,000 recharging points (both public and private).

In the economic section, the government’s calculations predict that the Moves III Plan will involve an extra contribution of €2.9 billion to the Spanish GDP that will generate nearly 40,000 jobs along the entire value chain.

Do you want to be the first to receive the latest news about 11Onze? Click here to subscribe to our Telegram channel

Every year, there are millions of people around the world who suffer the effects of online scams. Digitalisation has accelerated this increasingly common type of digital crime, but how can we prevent and avoid the serious effects that result from it?

Scams have always been present in the daily lives of all of us. Who hasn’t felt cheated in discovering that a product wasn’t what they expected? Who hasn’t seen the need to keep a close eye on their belongings while watching a street show in crowded places like the Rambles in Barcelona? Online scams are these events, but focused on the digital realm, which involves the theft of our identity or our money through various shenanigans, just like in real life.

The fundamental reason why they are booming is that, in the face-to-face world, we have much more experience in avoiding them. We have been doing it all our lives, while online fraud is a new event for most of us, and they are much more difficult to avoid, especially for those who are not yet fully accustomed to the digital realm. How can we protect ourselves?

Montserrat Massana tells us about fraud

Information is power

The key word is prevention. As the saying goes: no use crying over spilt milk. A phrase that, in the digital world, is a perfect fit. Unlike what happens in many physical scams, in online fraud it is very difficult to identify the author, so it is complicated to prosecute them and get them to return what they have stolen. Therefore, the best option is to take enough precautions so that it does not happen.

One of the most important is controlling the information we give about ourselves on the Net. And it is worth remembering that many virtual scammers take advantage of information that people may have left accessible in the cloud to try to make them fall into a trap: for example, receiving a message from a supposed messaging company the day you wait for a package can be the perfect setting to open a fake message and fall into the trap.

The best thing we can do, then, is to make things difficult for them and avoid sharing details on the internet that we don’t want strangers to know. That may mean changing privacy settings on our social networks, for example, by setting the profile as private, or restricting the information that people that you have not added as contacts can see.

In addition, we should also be vigilant with the information we give to third parties. If in an email, message, or call they ask you for personal information or a password, check that the sender of the message is actually who they claim to be, for example, by comparing the sender of the email with the information on the sender’s official website.

Protect your account to protect yourself

The other aspect that we must not neglect is the level of protection of our accounts, whether those of our social networks, our e-mail, or the bank’s application. It is advisable to have a strong password, if possible, one that includes numbers, letters (both uppercase and lowercase), and some special characters, such as a question mark or quotation marks.

Likewise, it is also recommended activating two-factor or two-step authentication on the pages where we can activate it. It is a security feature that activates two different user identification processes instead of one, so an outside person would need to have stolen much more personal information in order to access the account.

Protect yourself without becoming obsessed

More and more crimes are being committed online, but that doesn’t mean we have to become obsessed with security measures. As in real life, no matter how much care you take, sometimes you may be robbed, and the same goes for the digital realm: you may have protected yourself at a high level but, in every little detail, the possibility of a third person seeing it and taking advantage of it.

All in all, enjoying social media and surfing the internet safely is possible, and following these tips will serve as a precautionary measure. Of course, we must always remember that the risk exists, and therefore it is not worth making us paranoid in this regard, as the results can be counterproductive. Common sense, the avoidance of all those practices that we believe are not convenient for us, and controlling our privacy will be key in this fight against online fraud.

Do you want to be the first to receive the latest news about 11Onze? Click here to subscribe to our Telegram channel

The new electricity tariffs come into force from 1 June. Changes will be applied to the hourly consumption brackets and the possibility of contracting two different power supply levels for the same day will be introduced.

This new bill “will promote energy saving, efficiency, self-consumption and the deployment of electric vehicles”. Or so we are told by the Ministerio para la Transición Ecológica y lo Reto Demográfico.

It is designed to modify our consumption habits and will apply different prices based on three time slots and depending on whether it is a working day, weekend or public holiday. However, it will only affect domestic consumers and small businesses in the regulated market, the so-called Precio Voluntario para el Pequeño Consumidor (PVPC), and which have a contracted power of less than 15 kW.

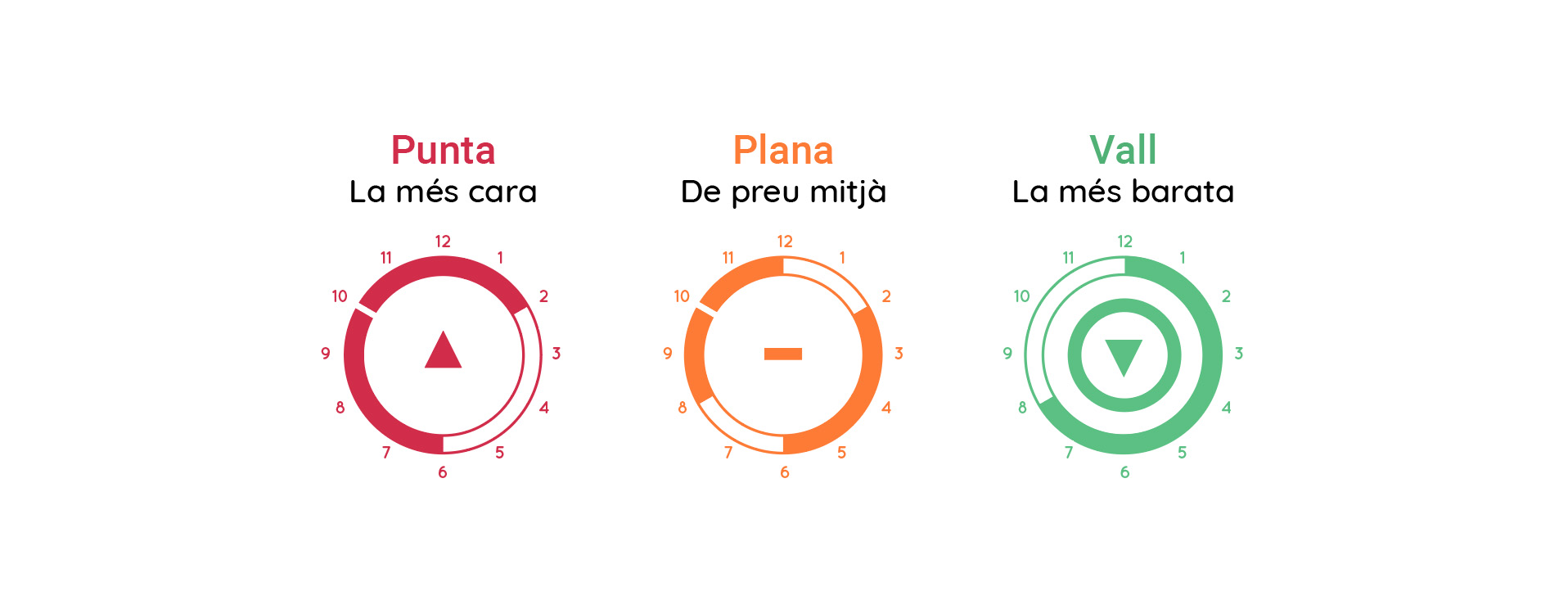

Three time bands

Three time bands are established with different tolls and charges. The cost of electricity in the Valle time band will be up to 95% cheaper than in the Punta time band, which is why it is recommended that you try to concentrate most of your electricity consumption in this time band between midnight and 8:00 in the morning.

- Punta, the most expensive. Weekdays from 10 am to 2 pm and from 6 pm to 10 pm.

- Plana, the medium price. Weekdays from 8 a.m. to 10 a.m., from 2 p.m. to 6 p.m. and from 10 p.m. to midnight.

- Valle, the cheapest. Weekdays from midnight to 8.00 a.m. and also all weekends and public holidays.

Two different power ratings

Until now, we could only contract one power rating, but with the new tariff we can contract two different ratings, although if we do not specify otherwise they will be of the same rating.

This is an interesting change for consumers who have an electric car with a charging point at home, and who will be able to contract the highest power in the cheapest time slot and thus take advantage of the opportunity to charge the batteries at an almost symbolic cost of €1.42 per kW contracted (OCU). Similarly, consumers who have storage heaters will benefit from the possibility of charging the heat reserves in the highest power period at the lowest tariff.

Does this mean that I will pay more, or less?

Well, it will depend on each household and the distribution of consumption. If we already had an hourly discrimination contract that included morning hours, we will have to adapt to the new time slots if we do not want our electricity bill to increase, since a good part of these hours, which until now had the cheapest tariff, will now have the most expensive one.

On the other hand, if we adjust the contracted power and get into the habit of using washing machines and dryers at the weekend or at night, we will be compensated with lower annual bills.

So, don’t these changes affect free market consumers?

Indirectly, possibly yes, since regardless of the contract we have signed, it is common for marketers to reserve the right to pass on to customers any legislative changes in reference to tolls or charges, and therefore we must be alert to any letter we receive from our electricity supplier indicating changes in the contract.

A more simplified bill, or not

Although it will be shorter, only two pages, it will have more information, such as the two new power ratings and the three energy bands. And it will also include a QR code with which we will be able to access a comparison of available offers from the Comisión Nacional de los Mercados y la Competencia (CNMC).

Obviously, none of these changes affect the oligopoly that the large electricity companies still have in our national market, despite the relative fragmentation of alternative suppliers, and which ensures that a significant drop in electricity prices remains, unfortunately, a utopia. But in any case, we already have our homework to do, at the very least, to prevent our electricity bills from rising.

Do you want to be the first to receive the latest news about 11Onze? Click here to subscribe to our Telegram channel

Silvia talks about Home renewable energy installation

We are in the middle of the 2020 income tax campaign, in a year that will be marked by the ERTEs that have had an impact on taxpayers’ finances. In order to have everything ready, we offer you a quick guide on how to do your income tax return.

On the other hand, the Tax Agency offers the “We’ll call you” plan, for those people who cannot do the online procedure or who cannot or do not want to go to a tax office branch. As the pandemic is still raging, the Tax Agency has reinforced its telephone service for all those taxpayers who do not wish to file their income tax returns in person. An appointment is made, and a member of staff will contact the taxpayer to make the tax return. Appointments can be made by telephone by calling 901 22 33 44 or 91 553 00 71 from Monday to Friday from 9am to 7pm before 29 June.

As in every tax year, the self-employed are a special case. Agent Oriol Garcia Farré analyses the most common obstacles for the self-employed and how to avoid them.

Do you want to be the first to receive the latest news about 11Onze? Click here to subscribe to our Telegram channel

Agent Oriol Garcia Farré explains it us

A neobank is a financial technology-based bank that operates only digitally or through a mobile app, and can offer most of the products and services of a conventional bank, minus the physical subdivisions. These are relatively young companies, with the neobank designation dating back to 2017.

Banking structures, as well as the needs of the population, have changed exponentially over the last few years. While it used to be commonplace to go to the bank in person to make transactions, we can now carry out the same operations from the sofa at home. In response to the new technological context, traditional banks, those that have been around forever, set to work to make a digital banking model available to the public that would allow a considerable number of banking operations to be carried out from any location.

Thanks to this adaptation, digital banks emerged, ready to address society’s new concerns. However, despite streamlining certain banking procedures, digital banks act as subsidiaries of larger banks that already have a specific track record. It is precisely in this context that neobanks were born; a banking structure that starts from scratch and that, moreover, has as a fundamental pillar the use of Fintech technology to serve its customers.

Over the last few years in Europe we have already started to work with neobanks, taking advantage of the technology in the market. But what exactly do neobanks offer, and what are the differences between traditional banking and a neobank?

Streamlined products and services

We all know what operations a traditional bank can carry out and what procedures can be carried out. The great challenge for them, in fact, was to try to transfer to the virtual world all the procedures that are usually carried out in branches, and they partially succeeded. There are still operations that require a visit to the bank because they cannot be carried out from a tablet or mobile phone. Opening a new account is one of them.

Neobanks, on the other hand, have a much more simplified structure compared to traditional banking. This means that they do not offer all the products or possibilities of the more veteran entities, but they have managed to bring together a good number of services with simpler procedures. In other words, they offer a smaller but at the same time more decisive range of products. Opening a current account, transferring money, managing cards or applying for credit are just some of the procedures that customers can access at any time. For this reason, neobanks are gaining more and more followers among small and medium-sized businesses and young people; they prefer effectiveness and speed in their operations over quantity.

Zero or almost zero fees

Surely more than once you have heard someone complaining about the commissions that banks ask for in order to manage procedures. These expenses are present on the part of traditional banks because they need to put a cost on the management of their agents, maintaining their branches and the bank itself. It is precisely here where we find one of the most relevant differential features. Unlike these, neobanks can afford a considerable reduction in commissions, since the use of technology means the elimination of the costs that large banking institutions have to face.

As a result, traditional banks have also tried to reduce their costs in order to be able to offer more competitive prices, but they have not managed to match the zero transaction costs or decrease their high savings rates. This is why the neobank model is currently gaining popularity.

Autonomous customers

This is undoubtedly one of the most differentiating factors between traditional banking and neobanks. While the former are characterised by little autonomy and, consequently, work every day to improve their digital services and thus gain more independence, neobanks offer absolute freedom from the outset through highly advanced technological tools that help customers control their money.

But the downside of this is that neobanks often do not have an interpersonal communication service between the customer and the bank itself. Interactions are limited and very much focused on customer services, behind which there may be machines. In this sense, traditional banks do have the capacity to build stronger relationships between customers and agents. As for their digital subsidiaries, despite not having a physical person, they have customer service time slots to be able to solve any doubt or problem in a personalised way.

11Onze has been training its first 50 agents since 15 March 2021 to provide a personalised service to future customers, offering all the advantages of a neobank with a person-to-person service.

Here we go again. The pandemic resulting from Covid-19 has generated an economic crisis (still germinating) that they claim will be worse than the one we suffered in 2008. But perhaps there is still time to lessen this impact and demand that those who lead us come up with other solutions. We need to be even more involved in what affects us, even if we don’t like it

When we look at the media, and they explain possible ways out of the crisis, one comes to the conclusion that a large majority of the messages are about cuts and the need for austerity. Emphasis is placed on the excesses we have all made, on the debt we have generated, which is seen to have been disproportionate, as if hell had been placed on earth, and we had all participated in the bacchanal.

Then, immersed in an excessive guilt, we all believe that we are punished to pay for the party and purge ourselves of so much debauchery. To a certain extent, it is true that a certain degree of restraint, a review of spending and saving when there are no lean times, seems quite rational and common sense. However, staying here alone and thinking that nothing more can be done makes me think of another fundamental issue: it reassures us in the short term to believe in unilateral solutions instead of trying to question them and find others.

Big problems, joint solutions

If I tell someone that there is only one way to make a bow on a gift package, they will probably accuse me of being uncreative and point out that there are many, many ways to do it. She will tell me that we have to innovate and that the art of making beautiful packages has evolved. That now, apart from ribbons, they make knots with string, they put them inside recycled paper bags, and we will discuss the many options of modern parcels.

But let’s go back to the current situation, and the same austerity loop, cut them and unwrap the crisis’ package. Then we look at the unemployment figures and they seem to be rising relentlessly. We look at the closure of businesses in Catalonia in the first quarter of 2012 and already more than 10,000 have closed their doors. We see that the middle class is losing purchasing power, and many families already have more than one member out of work. Fortunately, they can look back, nostalgically, to the bacchanal they may have celebrated one day.

Perhaps there have been excesses, but the question is, from everyone? Perhaps we do need to look at spending and bring it into line with the reality of ordinary income in the first stage. But do we have to go on like this forever? I think we should be more critical of those things that affect us and question the proposed solutions that we receive as inevitable. Wanting to know the reality is key in the process of leadership. And it is even more so when it comes to making decisions that are not pleasant for the decision-maker. But we must also be very clear that our knowledge of what is happening is always based on perceptions that must be improved through acceptance of the facts, practising humility. We never have complete knowledge of what is happening, and therefore it is always necessary to listen to opinions that differ from our own in order to have a more realistic picture.

What if we look for new solutions?

The recipes are not always simple or immediate, especially in times of crisis and difficulties. But wanting to know the reality, wanting to talk to people who do not have the same opinion as us, looking for a mix of enthusiasm and pragmatism, will surely lead us to assess the situation in a much more realistic way, and therefore to find solutions that do not meet our expectations, but will certainly help us to learn how to manage better in the future.

Perhaps alternative solutions should be discussed in depth. Experts in economics and business are already beginning to talk about other options. Professor Vicenç Navarro said that the problem is not GDP, but that the State must find efficient ways to collect the revenues that correspond to it in a proportional manner from the large fortunes, preventing them from fleeing to other countries (a similar problem that Greece also faces). Other experts warn that if we do not start facilitating access to credit for companies, the crisis will worsen. At least someone is trying to look for more creative alternatives to all the cutbacks that we have to listen to lately as a heavy mantra.

The key message is that people need to develop our judgement to decide whether what our rulers say makes sense or not, and we need to start asking for alternatives to the all too simple solution of cutting back. The heavy mantra of retrenchment must be replaced by a chorus of mantras that will stop us sinking into the current despair.

11Onze is the community fintech of Catalonia. Open an account by downloading the app El Canut for Android or iOS and join the revolution!

Nerves, worry, headache or muscle strain. These are just some of the symptoms generated by financial anxiety, that is, the constant worry about financial matters. A real problem that conditions people’s lives, but that we can reduce with patience and personal management.

Have you ever avoided going into your bank account for fear of seeing the amount of money you have? Have you ever felt guilty when you have spent money on a service or material object that was not strictly necessary? Do you feel anxious when you receive a letter from the bank? If you have answered “yes” to any of these situations, you have indeed suffered from the popular financial anxiety. A problem that has further impacted the health of society because of the pandemic and that also manifests itself physically through insomnia, muscle contractions and stress, among others. The bad news is that this anxiety will not disappear from one day to the next; the good news is that we can learn to control it in order to try to live with it.

- Detect the origin of the fear and start working to solve it.

Everything has an origin and surely there is a specific problem or concern that generates most of your discomfort. Although it is difficult, it is important to detect what it is in order to manage it. To do this, we can write down on a piece of paper what is going through our heads until we find out what it is that is upsetting us. For example, job instability is one of the most recurrent; the fear of being out of work. In this case and to start managing it, we can start actively looking for a job or make a monthly budget of the money we can spend until the end of the month. The goal is to be able to take small steps like these to help us reduce the worry at source and thus know that we are already doing something to solve it.

- Understand your own finances better

It’s not uncommon to receive a letter from the bank full of initials and words about economics that knocks us off our game. No, you are not less intelligent than the rest, it is completely normal not to master this kind of vocabulary. Knowing and researching a little more about economics can also help us to know what is happening with our income and what kind of products we are contracting and, therefore, more peace of mind. Reading from time to time the economic press or internet portals where they clearly explain terms or clauses in which you are involved is one of the resources that can help us in this aspect. Ten minutes a day is enough.

- Stay positive!

We know it’s easy to say and very difficult to do, but a positive mindset will help us combat our anxiety. Instead of going over and over the same concern thinking that it will not be solved, try to understand that the flow of money goes up and down and that, many times, it is not only up to you. The economic situation can always improve and with it, job opportunities. In the meantime, and to keep anxiety at bay, we can carry out activities that help us relax and release endorphins that keep us positive. Physical exercise, yoga or hobbies that require manual labour can help us to concentrate and minimize our daily problems.

In summary, the keys to managing stress caused by financial anxiety are basic yet essential. There is no magic formula, with patience and small steps you will be able to keep the anxiety that stops you from enjoying the little things, at bay.

There are applications on the market that allow you to pay, by instalment, online purchases and purchases in shops, without commissions for purchasers

In recent times, we have seen that large companies allow financing everything, that is, they allow the customer to buy low-price products (shoes, suits, and consoles, amongst others) and to pay them comfortably, by instalment. As a result of the pandemic, online sales have grown in all sectors and consumers have also been finding new ways of saving. This has increased the specialised fintech on credit payment systems, known as Buy Now, Pay Later (BNPL).

A few years ago, some retail shops introduced the concept of Buy Now, Pay Later, which is not new. In fact, this system allowed the products to be tested before they were paid, so if customers were not satisfied, they could return them. Therefore, customers only paid for products they actually kept.

New Payment Methods

Times change and so do the ways we buy and pay. One of the main benefits of traditional banks is the payment of charges at the time of a card purchase, whether in a shop or online. This is one of the markets which, in view of the few interests that can be paid by providing loans and mortgages, because of the low interest rates, enables banks to generate income. However, this market has recently got complicated, as new forms of payment directly applicable to vendors have appeared, and they incorporate the solution of “Buy Now, Pay Later” applications.

The two best known and most widely used applications in the world are that of the Swedish company Klarna and the Australian Afterpay.

The way these applications work is very simple. The user, after choosing a product, when they have already decided to buy it and check out, instead of pulling their card or wallet, pull their mobile phone. The shopkeeper sends a payment request via an email that the customer must confirm or the operation is confirmed by a QR reader. Once the operation is accepted, the acquired article can be kept.

So far, everything is very similar to a purchase made and paid with the mobile payment service of the purchaser’s bank. The difference is that with the system of the Buy Now, Pay Later (BNPL) system, the purchaser can, if they want, choose not to charge the bank account immediately for the purchase amount. This decision does not represent any cost to the user of the BNPL system.

When a credit card payment is made, if the purchaser finds there is no money on the account, the operation is automatically cancelled by the bank and they will have to leave the store without the product. On the other hand, traditional banks charge a fee to the store for the use of their online payment service and also, if the payment is on credit, in some cases, the bank will charge interest to the customer, as well as a card maintenance commission.

Another difference is that the Buy Now, Pay Later apps allow you to fragment purchase payments. The shop receives the total amount of the purchase at the time it is made, but the purchaser can choose different payment options by instalment (one or more payment fees, within a time limit allowed by the application), which will not impose any additional financial burden, that is, no interest or commission. Their cost will therefore be zero.

For the time being, in order to enjoy this payment system, it is necessary to have an account in a bank, as applications do not yet have a bank licence to operate customer accounts.

Competitive Advantage

And how do these applications earn their living if they do not charge commissions or interest to purchasers? Well, they charge a commission to shops, as traditional banks do. The difference is that this fee is less costly than the traditional fee.

Thus, fintech such as BNPL can survive only on this income because it has no major infrastructure costs, no maintenance, no advertising, and few employees, unlike traditional banking, which has very high costs in all these respects. In general, these payment application companies have low costs because they are based on technology. This gives them a competitive advantage over the traditional banking sector, as it allows them to offer services to the establishments in exchange for smaller commissions and, in turn, they do not charge customers any interest for choosing to pay for purchases by instalment.

BNPL applications have revolutionized the small shop industry and the way of shopping. Millennials are regular users of shopping applications and they value the chance of saving and the convenience at the time of making purchases, such as not paying fees or interests, as well as being able to pay in comfortable quotas. It is proven that, at the time of making a purchase, the price is decisive and, in online purchases, the final decision of keeping a product is taken at the time of confirming the purchase. The purchase is not completed because the purchaser considers the price to be a high-cost blow to their pocket. The possibility of paying for the purchase through BNPL (Buy Now, Pay Later), encourages the consumer to complete the purchase, increases customer loyalty, and provides a better shopping experience.

Buy Now, Pay Later apps are very popular in Australia and the United States and, in the last year, have broken through Europe in full strength.