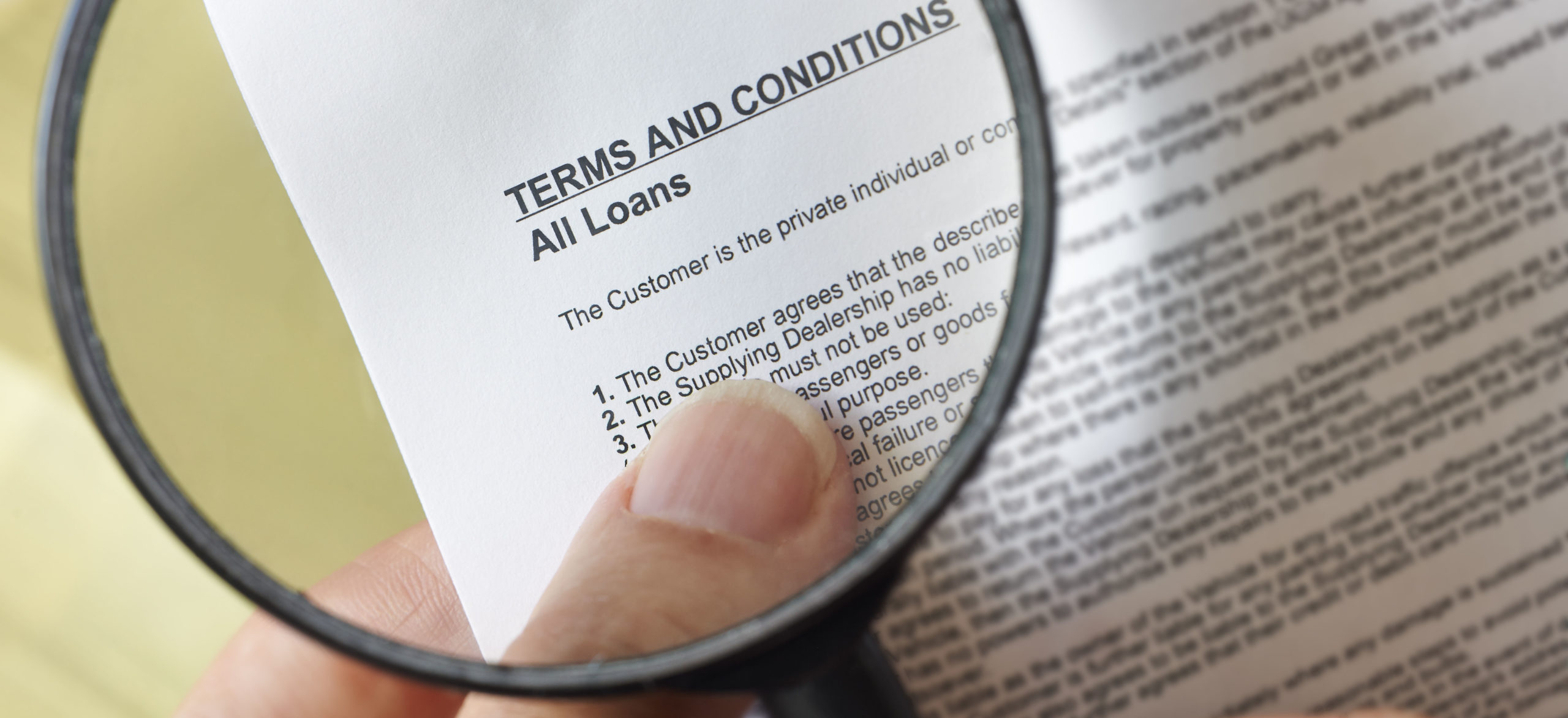

The ‘small print’ of any contractual relationship often goes unnoticed by the consumer when contracting a service or purchasing a product. Some companies take advantage of this fact to introduce clauses with abusive agreements. The law says that contracts have to be written in a clear and understandable way, but, even so, the traps of the ‘small print’ are repeated. Why? Jordi Coll, 11Onze agent, explains it to us.

If we talk about size, the ‘small print’ no longer exists, at least in reference to the contracting of services. Since 1 June of this year, the law obliges banks, insurance companies and any other service company to write the contracts they offer to consumers in characters with a minimum size of 2.5 millimetres.

The new regulation aims to avoid the damage caused to customers as a result of illegible contracts, which are impossible or more difficult to read because of the small print. The scandal of the ‘preferentes’ shares and subordinated debentures, which particularly affected the most vulnerable sectors of the population, such as the elderly, highlighted the urgent need to reform the regulations.

As Coll explains, “companies often use the small print with contracts that are not negotiable, and in order for them to go unnoticed by consumers”, and he continues, “they are even used to introduce clauses with abusive agreements”.

The small print, a gigantic deception

Size isn’t everything

Will this new regulation change anything? The previous law already set a minimum size for the small print, as well as calling for clarity and transparency in contracts. But despite the court rulings in favour of customers, condemning the companies involved, abuses were repeated. Why? Because it is good business. The percentage of affected customers who complain is negligible, so, bearing in mind that the profits are considerable, it pays to pay the fines, sanctions and lawsuits without changing anything.

Despite the fact that, as Coll points out, “current legislation allows consumers to request the non-application of these clauses when they have not been drafted with adequate clarity and transparency, or to declare them null and void when they are abusive”, bad practices have not been eliminated.

When asked to explain abusive credit card contracts or banking products such as preference shares, the excuse used by banks to justify themselves is to pass the buck to the customer, claiming that they should have read the contract. Does the size of the text characters really make a difference? Or is it the wording of the clauses and the ethical integrity of the institutions that should also be corrected?

11Onze is the community fintech of Catalonia. Open an account by downloading the super app El Canut for Android or iOS and join the revolution!

Leave a Reply

You must be logged in to post a comment.

Gràcies!!!!

👍

Moltes gràcies👍